Question: Dear tutor, Grateful for your help solving end of chapter questions as in the attached files. Q8 - You are managing a portfolio of $1

Dear tutor,

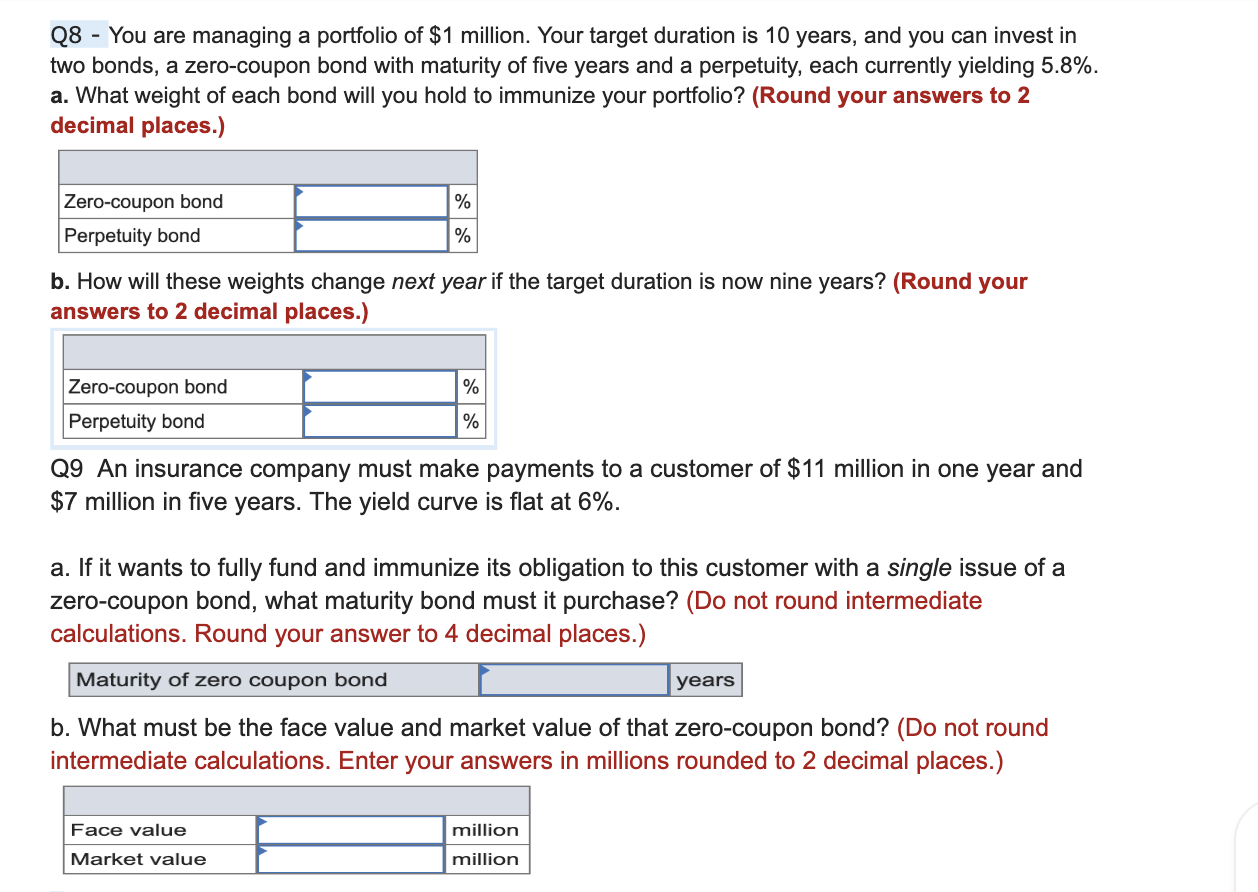

Grateful for your help solving end of chapter questions as in the attached files.

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock