Question: Debt versus Equity Financing Look Before You Leverage Why do things have to be so complicated? said Mark to Clive, as he sat at his

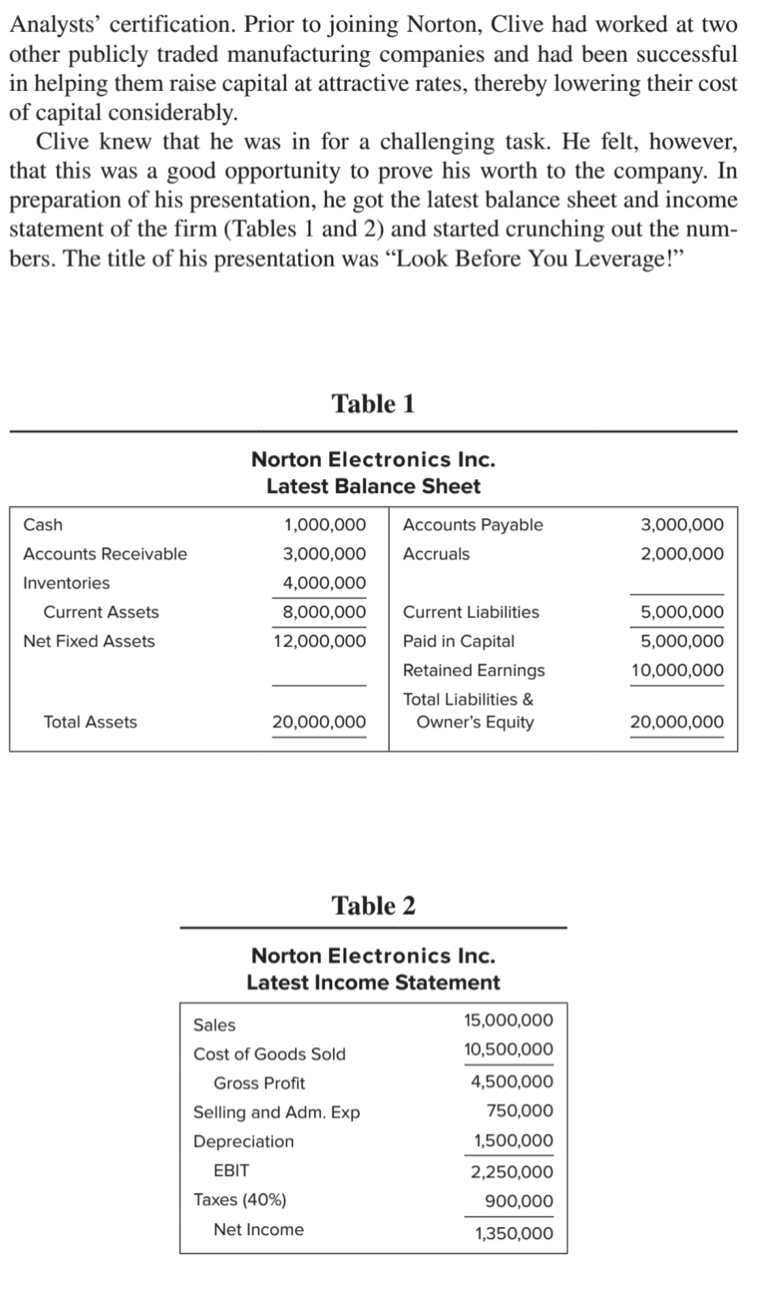

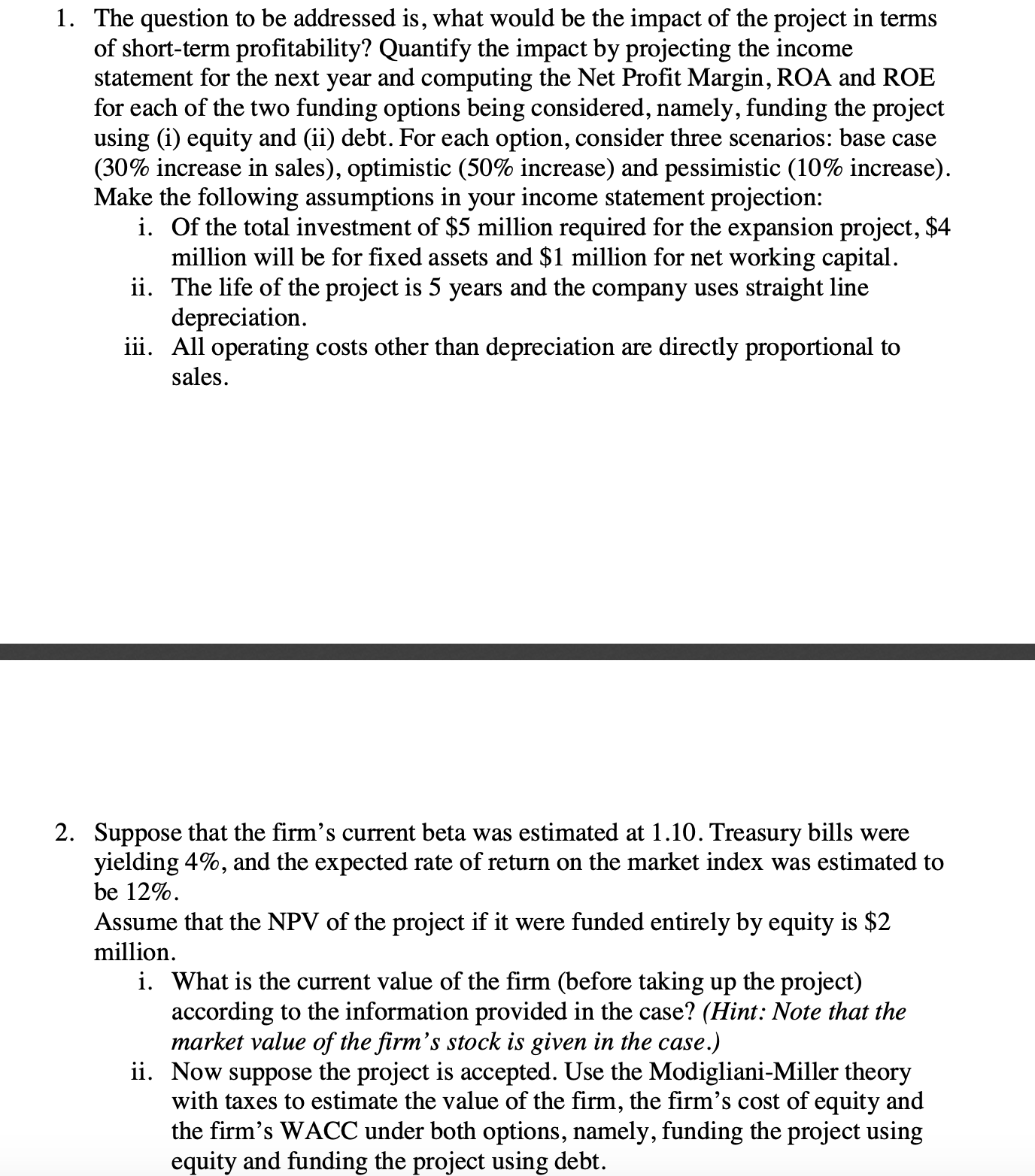

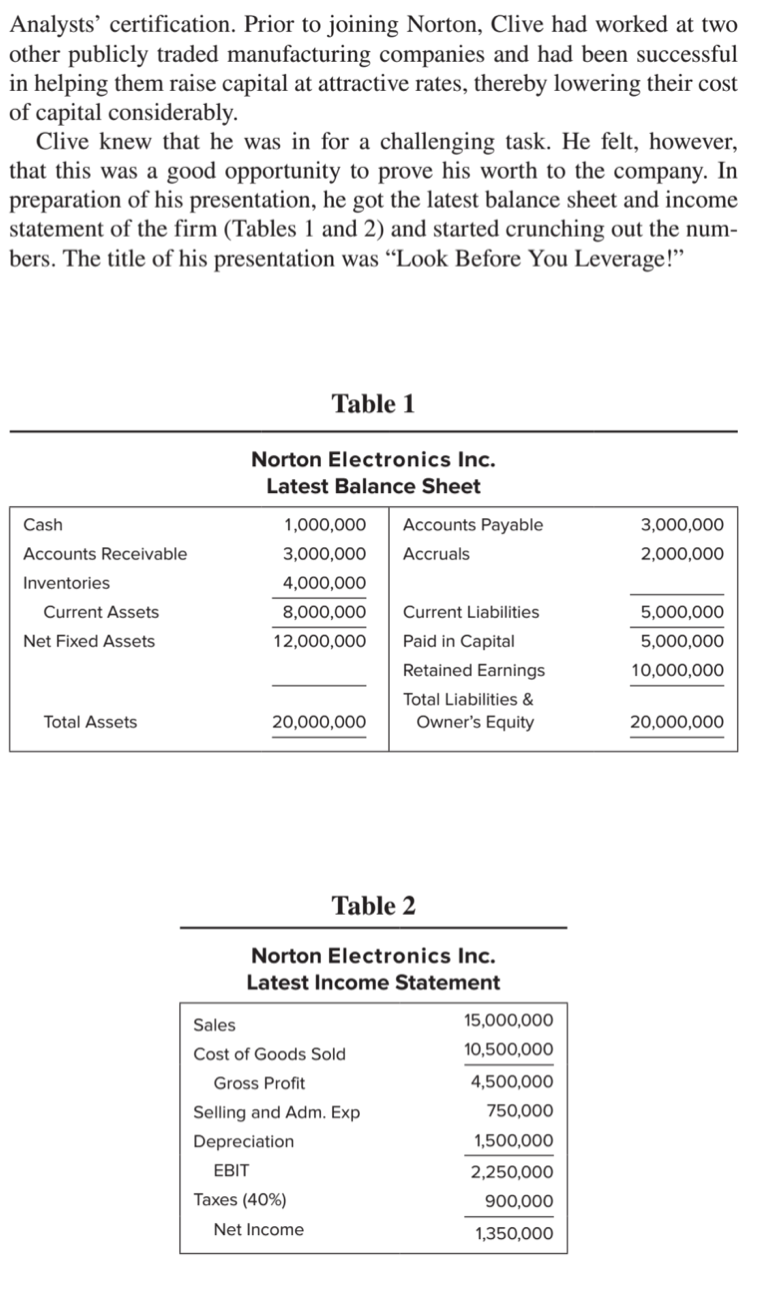

Debt versus Equity Financing Look Before You Leverage \"Why do things have to be so complicated?\" said Mark to Clive, as he sat at his desk shuffling papers around. \"I need you to come up with a con- vincing argument.\" Mark's company, Norton Electronics, had embarked upon an expansion project that had the potential of increasing sales by about 30% per year over the next ve years. The additional capital needed to nance the project had been estimated at $5,000,000. What Mark was wondering about was whether he should burden the rm with xed rate debt or issue common stock to raise the needed funds. Having had no luck with getting the board of directors to vote on a decision, Mark decided to call on Clive Jones, his chief nancial ofcer, to shed some light on the matter. Mark Norton, the chief executive ofcer of Norton Electronics, estab- lished his company about 10 years ago in his hometown of Cleveland, Ohio. After taking early retirement at age 55, Mark felt that he could really capitalize on his engineering knowledge and contacts within the industry. Mark remembered vividly how easily he had managed to get the company up and running by using $3,000,000 of his own savings and a ve-year bank note worth $2,000,000. He recollected how uneasy he had felt about that debt burden and the 14% per year rate of interest that the bank had been charging him. He remembered distinctly how relieved he had been after paying off the loan one year earlier than its ve-year term, and the surprised look on the bank manager's face. Business had been good over the years, and sales had doubled about every four years. As sales began to escalate with the booming economy and thriving stock market, the rm had needed additional capital. Initially, Mark had managed to grow the business by using internal equity and spontaneous nancing sources. However, about five years ago, when the need for nancing was overwhelming, Mark decided to take the company public via an initial public offering (IPO) in the over-the-counter market. The issue was very successful and oversubscribed, mainly due to the superb publicity and marketing efforts of the investment underwriting company that Mark had hired. The company sold 1 million shares at $5 per share. The stock price had grown steadily over time and was currently trading at its book value of $15 per share. When the expansion proposal was presented at last week's board meeting. the directors were unanimous about the decision to accept the proposal. Based upon the estimates provided by the marketing department, the project had the potential of increasing revenues by between 10% (worst case) and 50% (best case) per year. The internal rate of return was expected to far outperform the company's hurdle rate. Ordinarily, the project would have been started using internal and spontaneous funds. However, at this juncture, the rm had already invested all its internal equity into the business. Thus, Mark and his col- leagues were hard pressed to make a decision as to whether long-term debt or equity should be the chosen method of financing this time around. Upon contacting their investment bankers, Mark learned that they could issue five-year notes. at par. at a rate of 10% per year. Conversely, the company could issue common stock at its current price of $15 per share. Being unclear about what decision to make, Mark put the question to a vote by the directors. Unfortunately, the directors were equally divided in their opinion of which financing route should be chosen. Some direc- tors felt that the tax shelter offered by debt would help reduce the firm's overall cost of capital and prevent the rm's earnings per share from be- ing diluted. However, others had heard about \"homemade leverage\" and would not be convinced. They were of the opinion that it would be better for the rm to let investors leverage their investments themselves. They felt that equity was the way to go because the future looked rather uncer- tain and, being rather conservative, they were not interested in burdening the rm with interest charges. Besides, they felt that the firm should take advantage of the booming stock market. Feeling rather frustrated and confused, Mark decided to call upon his chief financial ofcer, Clive Jones, to resolve this dilemma. Clive had joined the company about two years ago. He held an MBA from a pres tigious university and had recently completed his Chartered Financial Analysts' certication. Prior to joining Norton, Clive had worked at two other publicly traded manufacturing companies and had been successful in helping them raise capital at attractive rates, thereby lowering their cost of capital considerably. Clive knew that he was in for a challenging task. He felt, however, that this was a good opportunity to prove his worth to the company. In preparation of his presentation, he got the latest balance sheet and income statement of the rm (Tables I and 2) and started crunching out the num- bers. The title of his presentation was \"Look Before You Leverage!" Table 1 Norton Electronics Inc. Latest Balance Sheet Cash 1,000,000 Accounts Payable 3.000.000 Accounts Receivable 3,000,000 Accruals 2,000,000 Inventories 4,000,000 Current Assets 3,000,000 Current Liabilities 5,000,000 Net Fixed Asseis 12,000,000 Paid in Capital 5,000,000 Retained Earnings 10,000,000 Total Liabilities 8: Total Assets 20,000,000 Owner's Equity 20,000,000 Table 2 Norton Electronics Inc. Latest Income Statement Sales 15,000,000 Cost of Goods Sold 10.500000 Gross Prot 4,500,000 Selling and Adm. Exp 750,000 Depreciation 1,500,000 EBIT 2,250,000 Taxes (40%) 900.000 Net Income m 1. The question to be addressed is, what would be the impact of the project in terms of short-term protability? Quantify the impact by projecting the income statement for the next year and computing the Net Prot Margin, RCA and ROE for each of the two funding options being considered, namely, funding the project using (i) equity and (ii) debt. For each option, consider three scenarios: base case (30% increase in sales), optimistic (50% increase) and pessimistic (10% increase). Make the following assumptions in your income statement projection: i. Of the total investment of $5 million required for the expansion project, $4 million will be for xed assets and $1 million for net working capital. ii. The life of the project is 5 years and the company uses straight line depreciation. iii. All operating costs other than depreciation are directly proportional to sales. 2. Suppose that the rm's current beta was estimated at 1.10. Treasury bills were yielding 4%, and the expected rate of return on the market index was estimated to be 12%. Assume that the NPV of the project if it were funded entirely by equity is $2 million. i. What is the current value of the rm (before taking up the project) according to the information provided in the case? (Hint: Note that the market value of the rm '3 stock is given in the case.) ii. Now suppose the project is accepted. Use the Modigliani-Miller theory with taxes to estimate the value of the rm, the rm's cost of equity and the firm's WACC under both options, namely, funding the project using equity and funding the project using debt. 3. What are some issues to be concerned about when increasing leverage? Is it reasonable to assume that if using debt were to increase profitability, the stock price would denitely increase? Explain. C. If you were Clive Jones, what would you recommend to the board, and why? Base your recommendation on your answers to questions 1, 2 and 3. Justify your recommendation by highlighting the key results of your analysis. Also, include any limitations of the analysis

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts