Question: Define credit default swaps. For a credit default swap (CDS) with the following terms (see exhibit 1 below), calculate the quarterly premium payment. Explain your

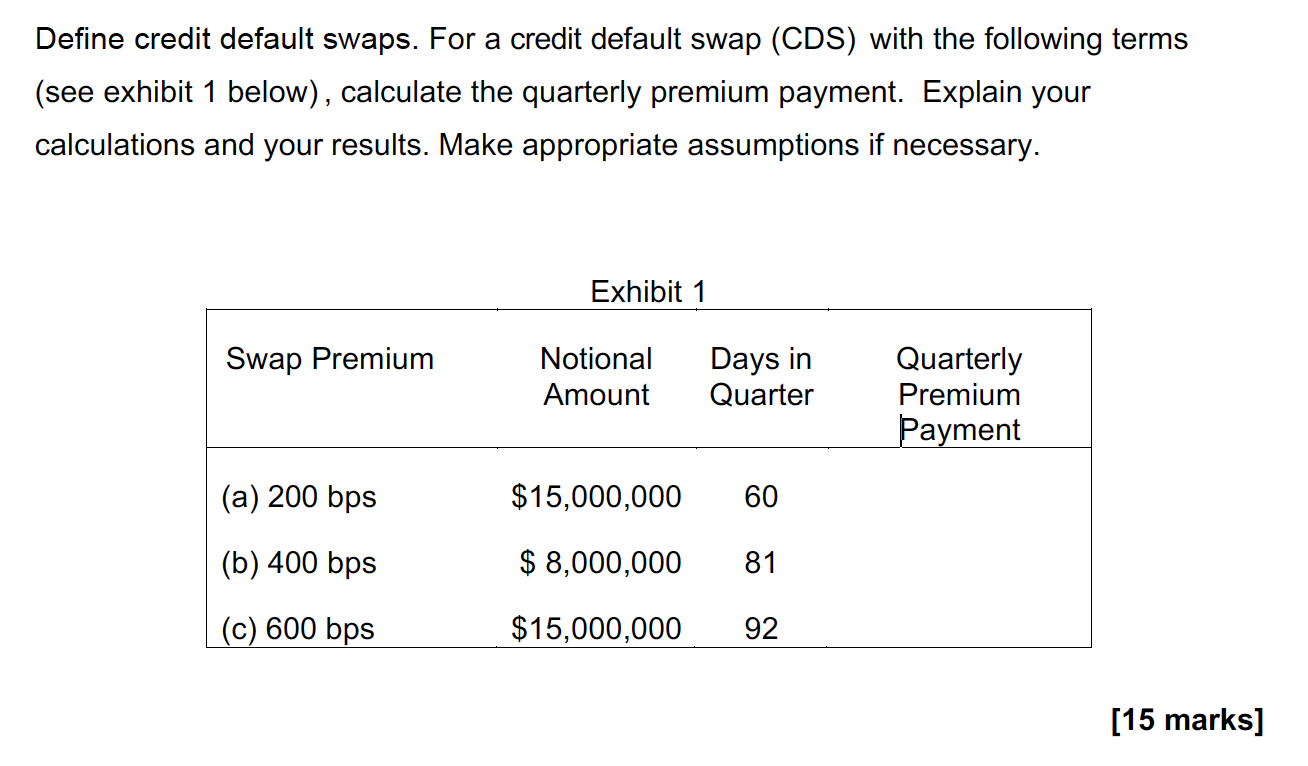

Define credit default swaps. For a credit default swap (CDS) with the following terms (see exhibit 1 below), calculate the quarterly premium payment. Explain your calculations and your results. Make appropriate assumptions if necessary. Exhibit 1 Swap Premium Notional Amount Days in Quarter Quarterly Premium Payment (a) 200 bps $15,000,000 60 (b) 400 bps $ 8,000,000 81 (c) 600 bps $15,000,000 92 [15 marks] Define credit default swaps. For a credit default swap (CDS) with the following terms (see exhibit 1 below), calculate the quarterly premium payment. Explain your calculations and your results. Make appropriate assumptions if necessary. Exhibit 1 Swap Premium Notional Amount Days in Quarter Quarterly Premium Payment (a) 200 bps $15,000,000 60 (b) 400 bps $ 8,000,000 81 (c) 600 bps $15,000,000 92 [15 marks]

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts