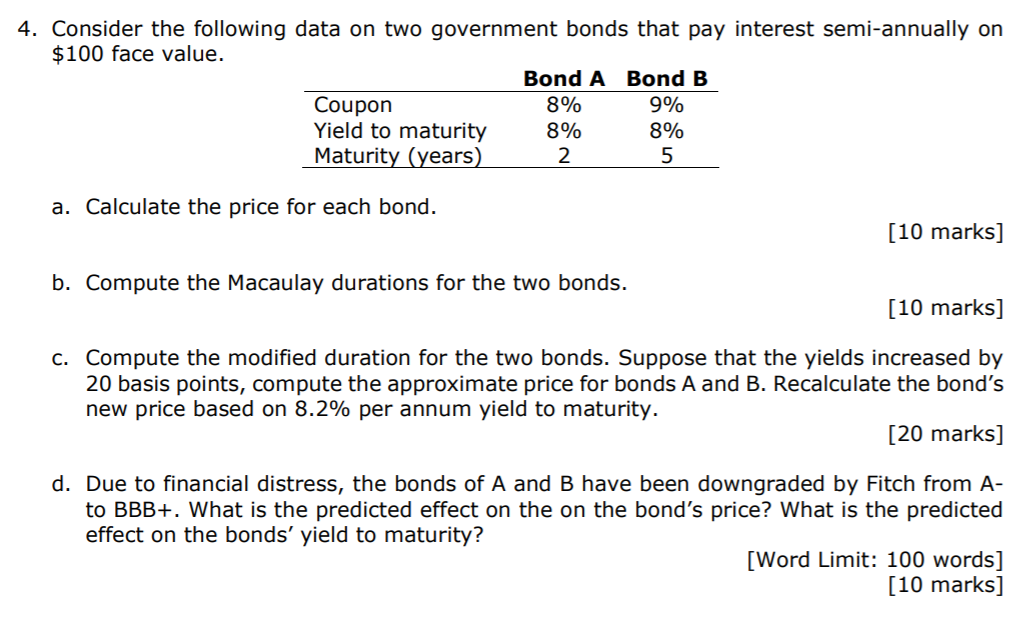

Question: Demonstrate every calculation 4. Consider the following data on two government bonds that pay interest semi-annually on $100 face value. Bond A Bond B Coupon

Demonstrate every calculation

Demonstrate every calculation

4. Consider the following data on two government bonds that pay interest semi-annually on $100 face value. Bond A Bond B Coupon 8% 9% Yield to maturity 8% 8% Maturity (years) 2 5 a. Calculate the price for each bond. (10 marks] b. Compute the Macaulay durations for the two bonds. [10 marks] C. Compute the modified duration for the two bonds. Suppose that the yields increased by 20 basis points, compute the approximate price for bonds A and B. Recalculate the bond's new price based on 8.2% per annum yield to maturity. [20 marks] d. Due to financial distress, the bonds of A and B have been downgraded by Fitch from A- to BBB+. What is the predicted effect on the on the bond's price? What is the predicted effect on the bonds' yield to maturity? [Word Limit: 100 words] [10 marks]

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts