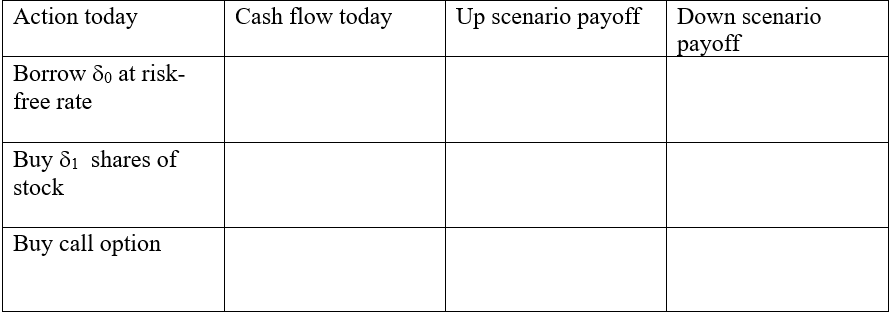

Demonstrate how a one-year European call option can be replicated when K = $50, S(0) = $50

Fantastic news! We've Found the answer you've been seeking!

Question:

Demonstrate how a one-year European call option can be replicated when K = $50, S(0) = $50 and the stock price in a year can take the value of either $65 or $40. Assume the risk-free interest rate equals 5% on an annualized basis. Find values for d0 and d1. Show all steps and calculations. Also, complete the following table and find the price for the call option.

Expert Answer:

Related Book For

Principles of Corporate Finance

ISBN: 978-0077404895

10th Edition

Authors: Richard A. Brealey, Stewart C. Myers, Franklin Allen

Posted Date: