Question: - Derivatives (Finance), discrete-time model; Exercise 1 Consider a one-period economy (Topic 1 slides 5-31) with four risky assets and four possible states of the

- Derivatives (Finance), discrete-time model;

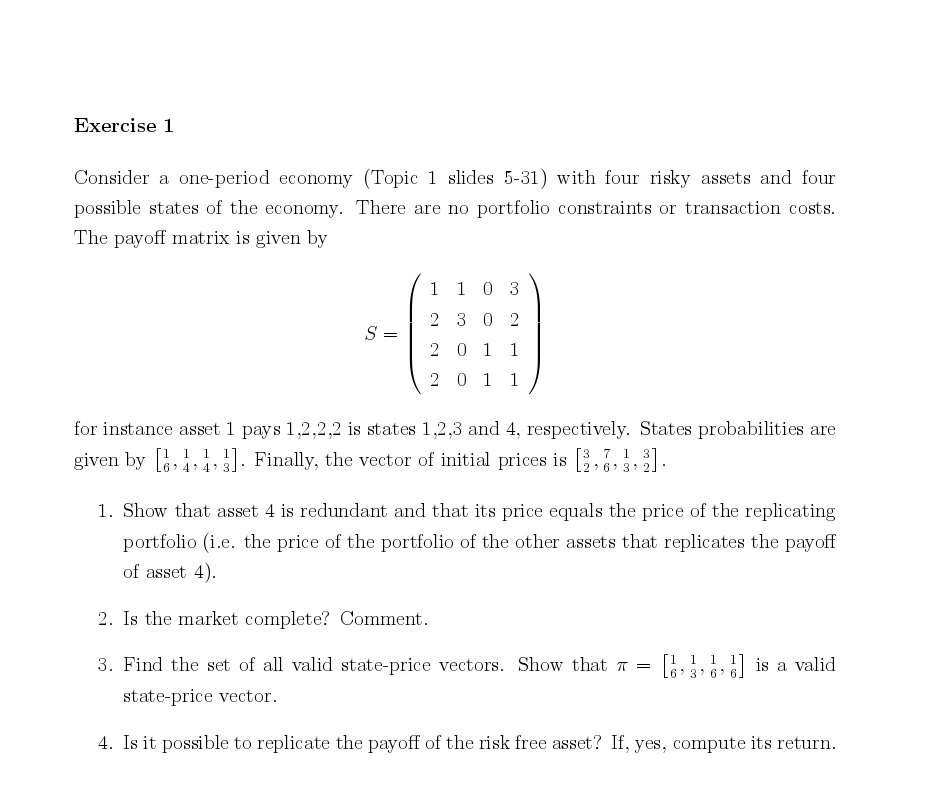

Exercise 1 Consider a one-period economy (Topic 1 slides 5-31) with four risky assets and four possible states of the economy. There are no portfolio constraints or transaction costs. The payoff matrix is given by 1 1 0 3 2 3 0 2 S= 2 0 1 1 1 2 0 1 for instance asset 1 pays 1,2,2,2 is states 1,2,3 and 4, respectively. States probabilities are given by [68: 4,3]. Finally, the vector of initial prices is [2:6,5,2]. 1 1 1. Show that asset 4 is redundant and that its price equals the price of the replicating portfolio (i.e. the price of the portfolio of the other assets that replicates the payoff of asset 4). 2. Is the market complete? Comment. 1 1 1 1 -6 3 6' 6. is a valid 3. Find the set of all valid state-price vectors. Show that a = state-price vector. 4. Is it possible to replicate the payoff of the risk free asset? If, yes, compute its return. Exercise 1 Consider a one-period economy (Topic 1 slides 5-31) with four risky assets and four possible states of the economy. There are no portfolio constraints or transaction costs. The payoff matrix is given by 1 1 0 3 2 3 0 2 S= 2 0 1 1 1 2 0 1 for instance asset 1 pays 1,2,2,2 is states 1,2,3 and 4, respectively. States probabilities are given by [68: 4,3]. Finally, the vector of initial prices is [2:6,5,2]. 1 1 1. Show that asset 4 is redundant and that its price equals the price of the replicating portfolio (i.e. the price of the portfolio of the other assets that replicates the payoff of asset 4). 2. Is the market complete? Comment. 1 1 1 1 -6 3 6' 6. is a valid 3. Find the set of all valid state-price vectors. Show that a = state-price vector. 4. Is it possible to replicate the payoff of the risk free asset? If, yes, compute its return

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts