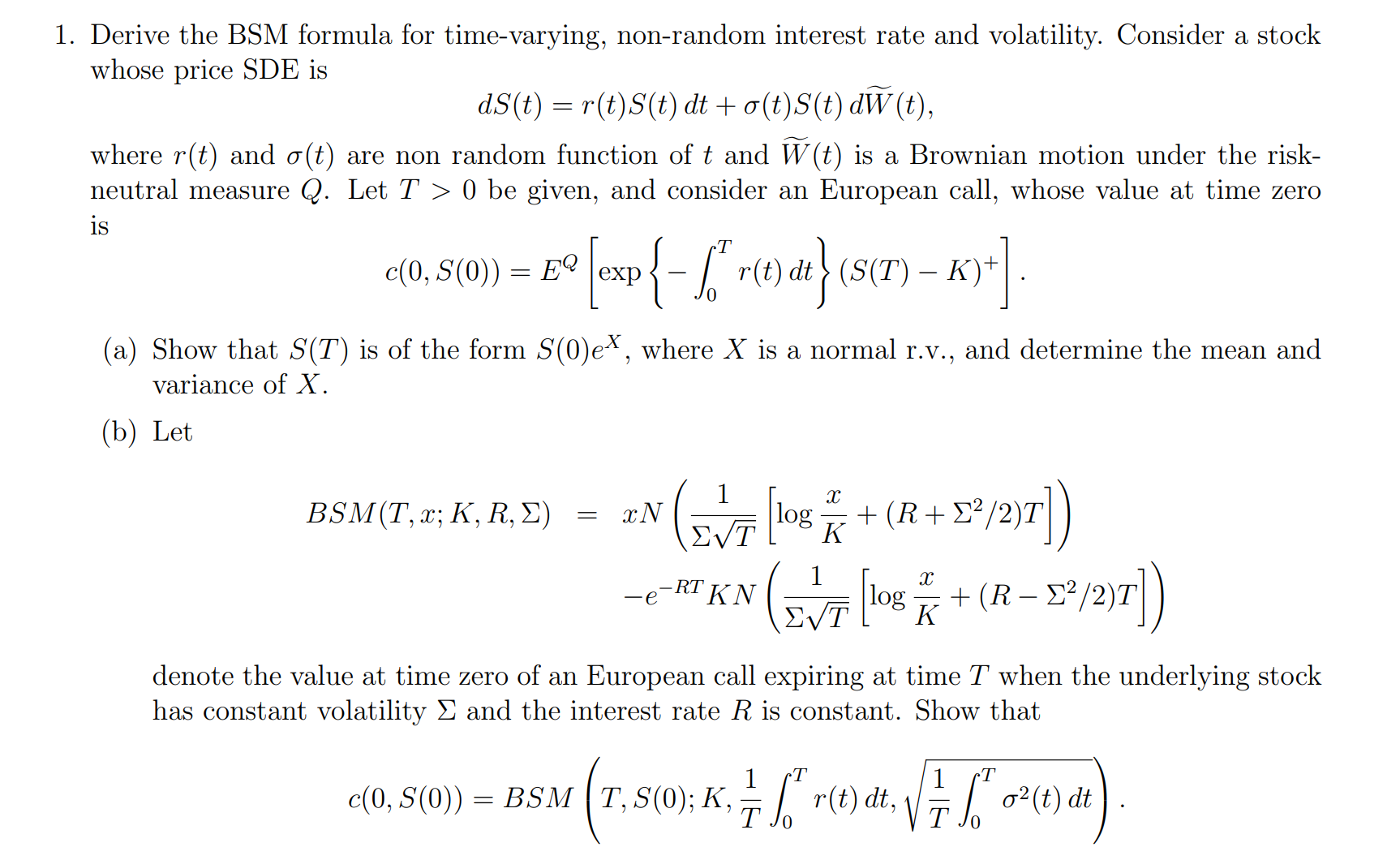

Question: Derive the BSM formula for time - varying, non - random interest rate and volatility. Consider a stock whose price SDE is d S (

Derive the BSM formula for timevarying, nonrandom interest rate and volatility. Consider a stock

whose price SDE is

where and are non random function of and widetilde is a Brownian motion under the risk

neutral measure Let be given, and consider an European call, whose value at time zero

is

a Show that is of the form where is a normal rv and determine the mean and

variance of

b Let

;

denote the value at time zero of an European call expiring at time when the underlying stock

has constant volatility and the interest rate is constant. Show that

;

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock