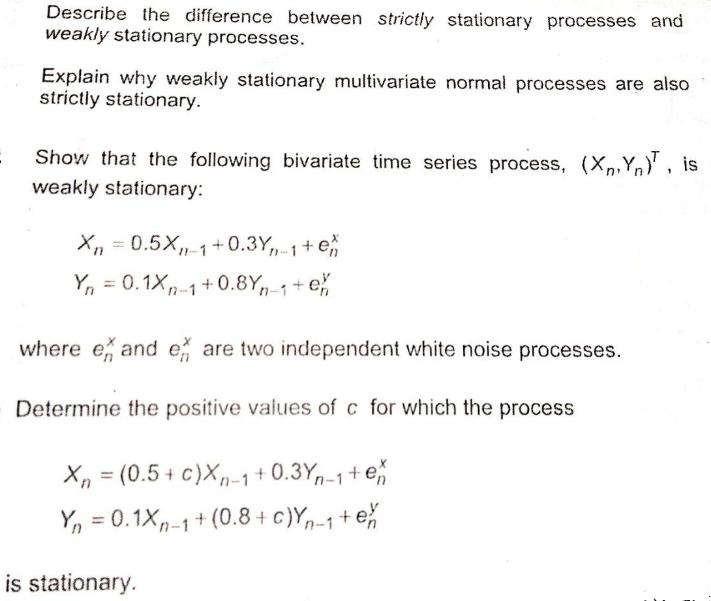

Question: Describe the difference between strictly stationary processes and weakly stationary processes. Explain why weakly stationary multivariate normal processes are also strictly stationary. Show that

Describe the difference between strictly stationary processes and weakly stationary processes. Explain why weakly stationary multivariate normal processes are also strictly stationary. Show that the following bivariate time series process, (X,Y), is weakly stationary: 1 Xn=0.5X, 1+0.3Y,, 1+e Yn = 0.1Xn-1+0.8Yn 1+e where e and e are two independent white noise processes. Determine the positive values of c for which the process X = (0.5+ c)Xn-1 +0.3Yn-1+en Yn = 0.1Xn-1+ (0.8+ c)Y-1+ex is stationary.

Step by Step Solution

★★★★★

3.30 Rating (147 Votes )

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock