Question: Description Instructions This is Section A of Tutorial Assignment 2 It comprises 15 multi-choice questions. Please select the BEST answer to each question. Your best

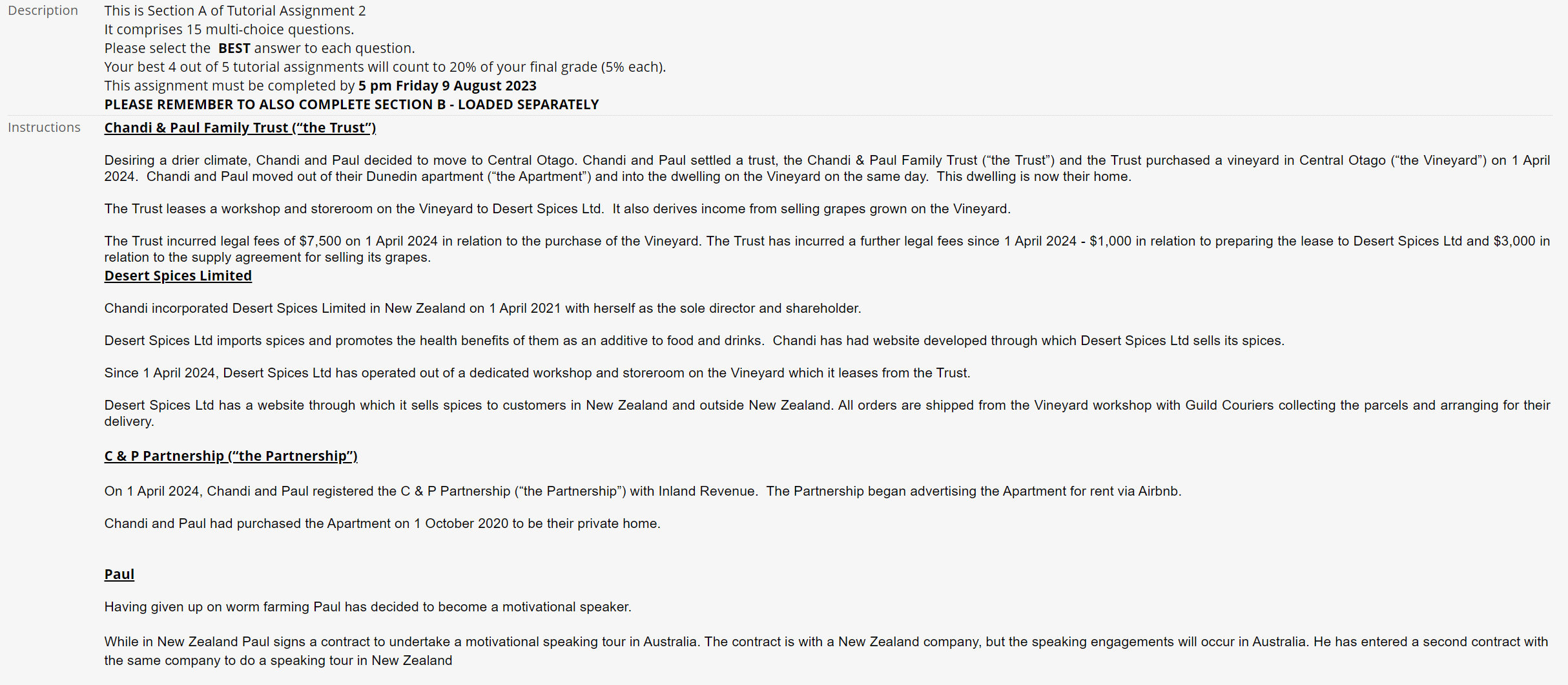

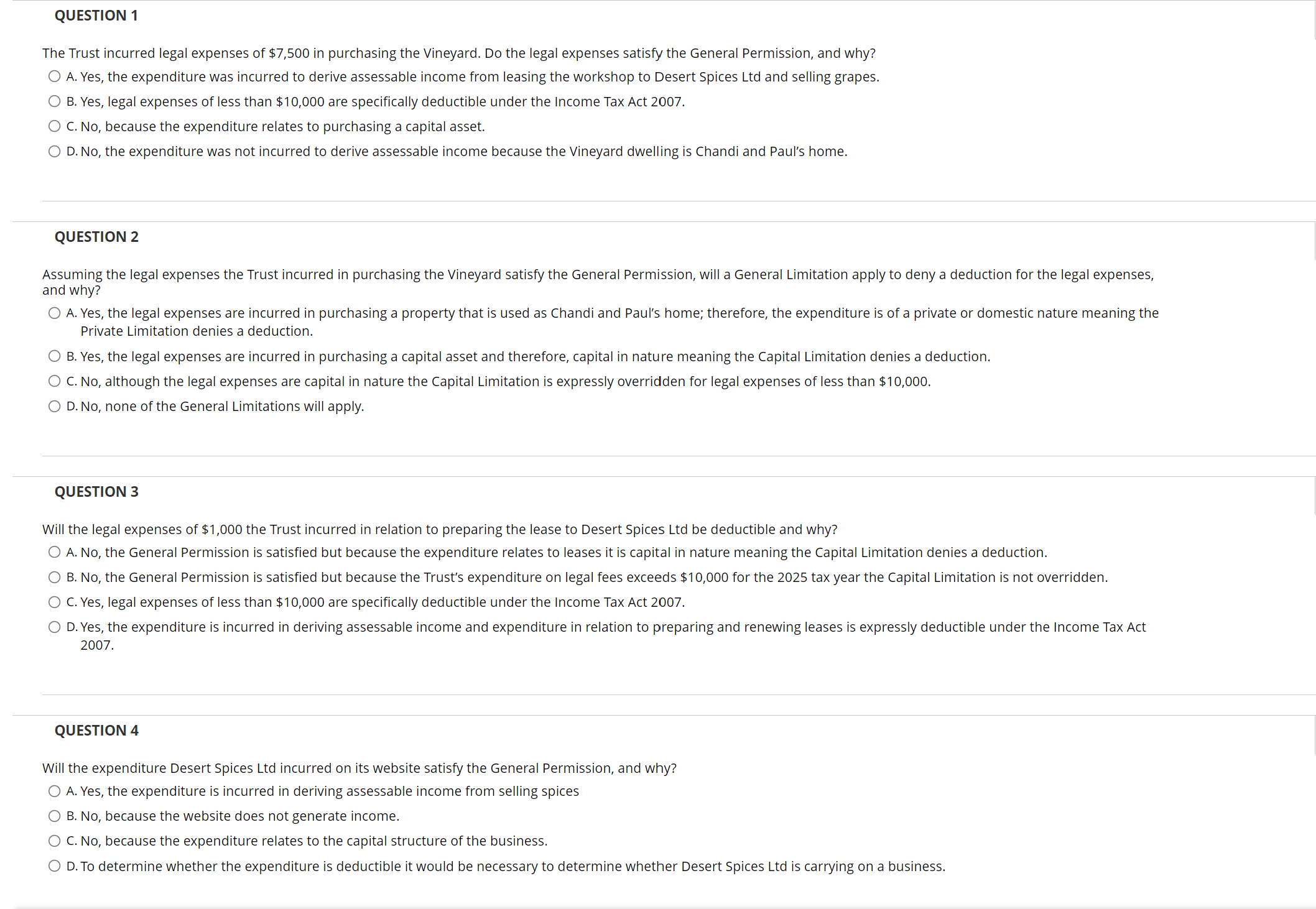

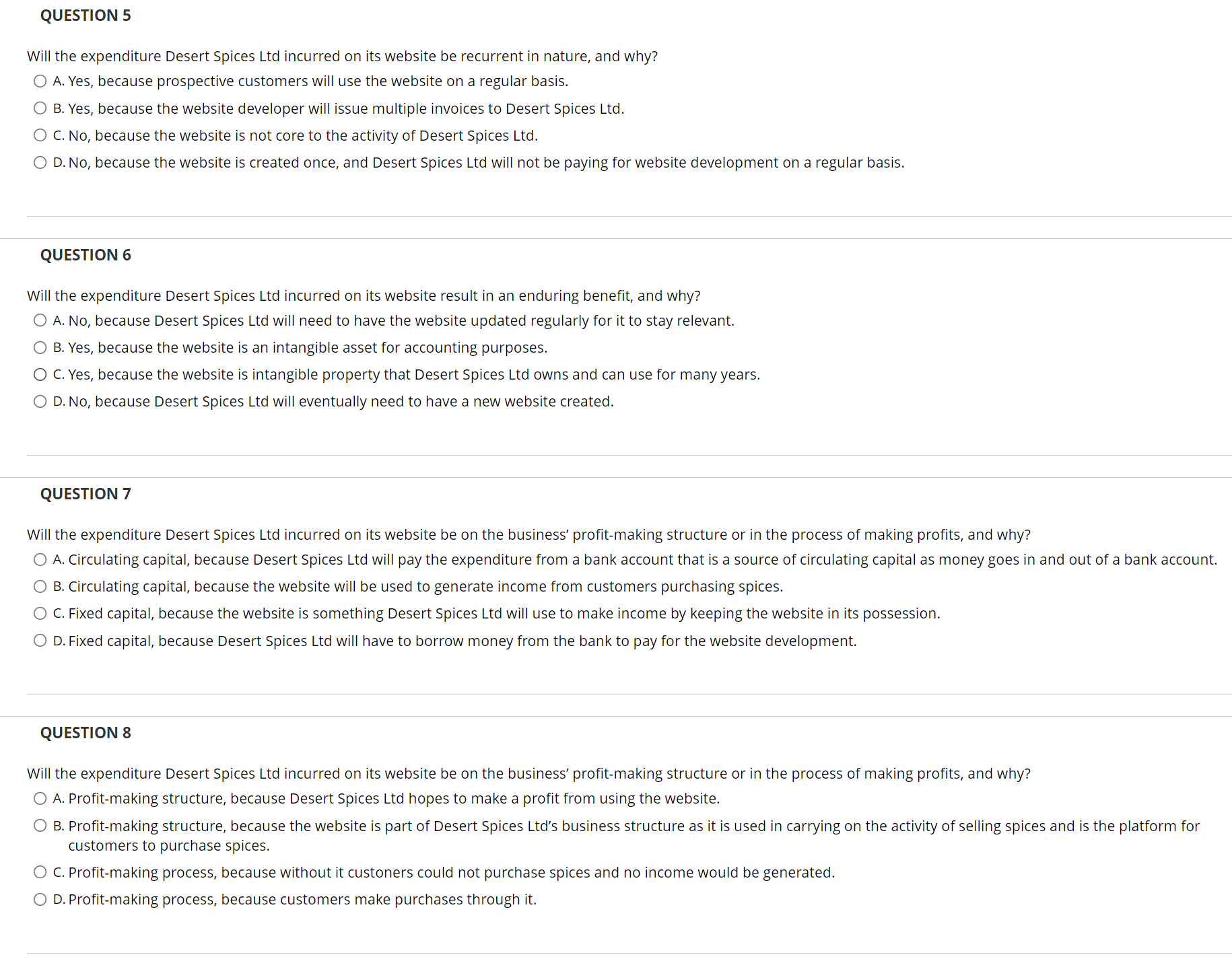

Description Instructions This is Section A of Tutorial Assignment 2 It comprises 15 multi-choice questions. Please select the BEST answer to each question. Your best 4 out of 5 tutorial assignments will count to 20% of your final grade (5% each). This assignment must be completed by 5 pm Friday 9 August 2023 PLEASE REMEMBER TO ALSO COMPLETE SECTION B - LOADED SEPARATELY Chandi & Paul Family Trust (\"the Trust\") Desiring a drier climate, Chandi and Paul decided to move to Central Otago. Chandi and Paul settled a trust, the Chandi & Paul Family Trust (\"the Trust\") and the Trust purchased a vineyard in Central Otago (\"the Vineyard\") on 1 April 2024. Chandi and Paul moved out of their Dunedin apartment (\"the Apartment\") and into the dwelling on the Vineyard on the same day. This dwelling is now their home. The Trust leases a workshop and storeroom on the Vineyard to Desert Spices Ltd. It also derives income from selling grapes grown on the Vineyard. The Trust incurred legal fees of $7,500 on 1 April 2024 in relation to the purchase of the Vineyard. The Trust has incurred a further legal fees since 1 April 2024 - $1,000 in relation to preparing the lease to Desert Spices Ltd and $3,000 in relation to the supply agreement for selling its grapes. Desert Spices Limited Chandi incorporated Desert Spices Limited in New Zealand on 1 April 2021 with herself as the sole director and shareholder. Desert Spices Ltd imports spices and promotes the health benefits of them as an additive to food and drinks. Chandi has had website developed through which Desert Spices Ltd sells its spices. Since 1 April 2024, Desert Spices Ltd has operated out of a dedicated workshop and storeroom on the Vineyard which it leases from the Trust. Desert Spices Ltd has a website through which it sells spices to customers in New Zealand and outside New Zealand. All orders are shipped from the Vineyard workshop with Guild Couriers collecting the parcels and arranging for their delivery. On 1 April 2024, Chandi and Paul registered the C & P Partnership (\"the Partnership\") with Inland Revenue. The Partnership began advertising the Apartment for rent via Airbnb. Chandi and Paul had purchased the Apartment on 1 October 2020 to be their private home. Paul Having given up on worm farming Paul has decided to become a motivational speaker. While in New Zealand Paul signs a contract to undertake a motivational speaking tour in Australia. The contract is with a New Zealand company, but the speaking engagements will occur in Australia. He has entered a second contract with the same company to do a speaking tour in New Zealand QUESTION 1 The Trust incurred legal expenses of $7,500 in purchasing the Vineyard. Do the legal expenses satisfy the General Permission, and why? O A.Yes, the expenditure was incurred to derive assessable income from leasing the workshop to Desert Spices Ltd and selling grapes. O B. Yes, legal expenses of less than $10,000 are specifically deductible under the Income Tax Act 2007. O C.No, because the expenditure relates to purchasing a capital asset. O D.No, the expenditure was not incurred to derive assessable income because the Vineyard dwelling is Chandi and Paul's home. QUESTION 2 Assuming the legal expenses the Trust incurred in purchasing the Vineyard satisfy the General Permission, will a General Limitation apply to deny a deduction for the legal expenses, and why? O A.Yes, the legal expenses are incurred in purchasing a property that is used as Chandi and Paul's home; therefore, the expenditure is of a private or domestic nature meaning the Private Limitation denies a deduction. O B. Yes, the legal expenses are incurred in purchasing a capital asset and therefore, capital in nature meaning the Capital Limitation denies a deduction. O C.No, although the legal expenses are capital in nature the Capital Limitation is expressly overridden for legal expenses of less than $10,000. O D.No, none of the General Limitations will apply. QUESTION 3 Will the legal expenses of $1,000 the Trust incurred in relation to preparing the lease to Desert Spices Ltd be deductible and why? O A.No, the General Permission is satisfied but because the expenditure relates to leases it is capital in nature meaning the Capital Limitation denies a deduction. O B. No, the General Permission is satisfied but because the Trust's expenditure on legal fees exceeds $10,000 for the 2025 tax year the Capital Limitation is not overridden. O C.Yes, legal expenses of less than $10,000 are specifically deductible under the Income Tax Act 2007. O D.Yes, the expenditure is incurred in deriving assessable income and expenditure in relation to preparing and renewing leases is expressly deductible under the Income Tax Act 2007. QUESTION 4 Will the expenditure Desert Spices Ltd incurred on its website satisfy the General Permission, and why? O A.Yes, the expenditure is incurred in deriving assessable income from selling spices O B.No, because the website does not generate income. O C.No, because the expenditure relates to the capital structure of the business. O D.To determine whether the expenditure is deductible it would be necessary to determine whether Desert Spices Ltd is carrying on a business. QUESTION 5 Will the expenditure Desert Spices Ltd incurred on its website be recurrent in nature, and why? O A. Yes, because prospective customers will use the website on a regular basis. O B. Yes, because the website developer will issue multiple invoices to Desert Spices Ltd. (O C.No, because the website is not core to the activity of Desert Spices Ltd. O D.No, because the website is created once, and Desert Spices Ltd will not be paying for website development on a regular basis. QUESTION 6 Will the expenditure Desert Spices Ltd incurred on its website result in an enduring benefit, and why? O A.No, because Desert Spices Ltd will need to have the website updated regularly for it to stay relevant. O B. Yes, because the website is an intangible asset for accounting purposes. QO C.Yes, because the website is intangible property that Desert Spices Ltd owns and can use for many years. O D.No, because Desert Spices Ltd will eventually need to have a new website created. QUESTION 7 Will the expenditure Desert Spices Ltd incurred on its website be on the business' profit-making structure or in the process of making profits, and why? O A. Circulating capital, because Desert Spices Ltd will pay the expenditure from a bank account that is a source of circulating capital as money goes in and out of a bank account. O B. Circulating capital, because the website will be used to generate income from customers purchasing spices. O C.Fixed capital, because the website is something Desert Spices Ltd will use to make income by keeping the website in its possession. O D.Fixed capital, because Desert Spices Ltd will have to borrow money from the bank to pay for the website development. QUESTION 8 Will the expenditure Desert Spices Ltd incurred on its website be on the business' profit-making structure or in the process of making profits, and why? O A. Profit-making structure, because Desert Spices Ltd hopes to make a profit from using the website. O B. Profit-making structure, because the website is part of Desert Spices Ltd's business structure as it is used in carrying on the activity of selling spices and is the platform for customers to purchase spices. O c. Profit-making process, because without it custoners could not purchase spices and no income would be generated. O D.Profit-making process, because customers make purchases through it. QUESTION 9 Will the expenditure Desert Spices Ltd incurred on its website produce an identifiable asset, and why? O A.No, because a website only exists in an online format. O B. Yes, because many people recognise a website as a valuable item. O C.No, because a website is not a real thing. O D.Yes, because a website is a capital asset that can be identified. QUESTION 10 How will the expenditure Desert Spices Ltd incurred on its website be treated for accounting purposes? O A It would be expensed. O B. It would give rise to a liability. O C. It would be capitalised as a fixed asset. O D.It would be treated as a capital loss. QUESTION 11 Will the expenditure Desert Spices Ltdincurs on its website be allowed as a deduction and why? O A.No, because although the expenditure satisfies the General Permission it is capital in nature and the Capital Limitation denies a deduction. O B. Yes, because the expenditure satisfies the General Permission. O C.Yes, because the expenditure satisfies the General Permission, and no General Limitation applies. O D.No, because the expenditure does not satisfy the General Permission. QUESTION 12 Assuming Paul is self-employed (not an employee) Paul has decided to drive from place-to-place on his motivational speaking tour of New Zealand. He will do so in his motor vehicle, which he also uses privately. Will Paul be entitled to a deduction for expenditure he incurs in relation to the running costs of the motor vehicle, including depreciation, and why? O A. No, because the motor vehicle is a capital asset which means the expenditure is capital in nature and the Capital Limitation will deny a deduction for the expenditure. O B. Yes, because the expenditure is incurred in carrying on an activity to derive assessable income, but the Private Limitation will limit the deduction available and require an apportionment between income-earning and private use. O C.Yes, because the expenditure is incurred in carrying on an activity to derive assessable income. O D.No, because the motor vehicle is a private vehicle, therefore the Private Limitation will deny a deduction for the expenditure. QUESTION 13 Desert Spice Ltd sold some of its products to an Auckland restaurant in December 2023 with payment due by 20 January 2024. When the invoice made went unpaid, Chandi made inquiries in late February 2024 and discovered the restaurant had gone into liquidation. She was advised by the liquidator that Desert Spices Ltd was unlikely to have its invoice paid. Although Desert Spices Ltd has a Xero subscription, Chandi is not confident using it. She maintains paper records of invoices Desert Spice Ltd issues and makes notes on them when they are paid. In February 2024, she writes on the invoice to the Auckland restaurant \"Not recoverable - bad debt\" and crosses out the amount due. She then removed the invoice from the bundle of unpaid invoices and put with the paid invoices. In June 2024, she provides Desert Spices Ltd's accountant with the bundle of invoices to assist with compilation of its financial statements for the year ended 31 March 2024. In June 2024, the accountant updates Desert Spices Ltd's Xero and records the invoice to the Auckland restaurant as a bad debt. In what tax year can Desert Spices Ltd claim a bad debt deduction and why? O A.Year ended 31 March 2024, because the debt became bad when it was not paid by the due date of 20 January 2024. O B.Year ended 31 March 2025, because although Chandi had grounds for believing the debt was bad in the year ended 31 March 2024 the debt was not recorded as bad in Xero until June 2025. O C.Year ended 31 March 2024, because the debt became bad when the liquidator notified Chandi it was unlikely to be paid. O D.Year ended 31 March 2024, because the liquidator had advised the invoice was unlikely to be paid and Chandi had written off the debt as bad in Desert Spices Ltd records. QUESTION 14 Desert Spices Ltd paid for Chandi to attend a conference in Auckland on marketing and selling online. The Conference was all-day Thursday and Friday. Desert Spices Ltd paid for her meals while she was attending the Conference. Will Desert Spices Ltd be able to claim a deduction for the expenditure on Chandi's meals, and why? O A Yes, the expenditure is incurred in carrying on Desert Spices Ltd's business meaning the General Permission is satisfied, no General Limitation applies, and the Entertainment Limitation does not apply to the expenditure on meals paid for as part of business-related travel or conferences. O B. No, the expenditure on meals is referrable to living as an individual member of society and a deduction is denied by the Private Limitation. O C. Yes, the expenditure is incurred in carrying on Desert Spices Ltd's business meaning the General Permission is satisfied, no General Limitation applies but the expenditure is only 50% deductible due to the Entertainment Limitation. O D.No, the expenditure on meals does not result in Desert Spice Ltd deriving assessable income meaning the General Permission is not satisfied. QUESTION 15 Desert Spice Ltd made a net loss of $20,000 in its first year of trading, the year ended 31 March 2022. What can Desert Spicer Ltd do with the net loss for the 2022 tax year? [ A. The net loss becomes a tax loss, which it can carry forward to the next tax year and/or offset against the net income of another company for the 2022 tax year. [ B. The net loss becomes a tax loss, which it can carry forward to the next tax year. [J C.The net loss becomes a tax loss, which it can carry forward to the next tax year and/or transfer to another person to offset against their net income for the 2022 tax year. [0 D.The net loss becomes a tax loss, which it can transfer to another person to offset against their net income for the 2022 tax year

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock

Students Have Also Explored These Related Accounting Questions!