Question: Detailed Instructions: Given the inputs c r , F V , T , r , you are going to evaluate a bond with annual coupon

Detailed Instructions:

Given the inputs r you are going to evaluate a bond with annual coupon payment

Calculate the bond price.

Note that the interest rate given array is NOT a flat yield

curve, so you cannot discount back everything using one same rate

Calculate the bond price

Find out the implicit yield to maturity

Calculate the Duration of this bond

Suppose the YTM changed, newytm what are the

percentage changes sensitivities in the bond price,

specifically you need to produce an array of using your established duration level

Use matplotlib to plot the rates curve given as

Hint:

IMPORTANT Make sure you use PRINT function to check necessary intermediery outputs

To calculate the bond price, you can do it by compute the pv of fv and coupon separtately

think about how to take the summation for array elements?

To calculate the duration, be careful about the weights!!!

To compute the YTM use numpyfinancial You can use other approches as

well, go find them.

To gauge the sensitivities of price to YTM you need to figure out the array in the first place

PricechangedeltaytmDuration

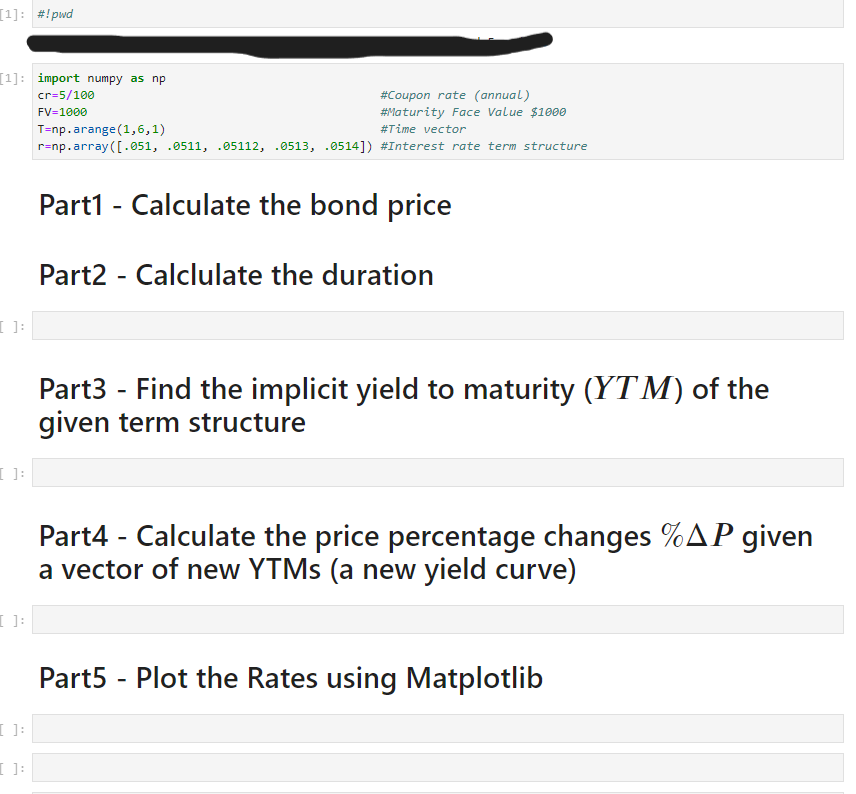

Part Calculate the bond price

Part Calclulate the duration

Part Find the implicit yield to maturity YTM of the

given term structure

Part Calculate the price percentage changes given

a vector of new YTMs a new yield curve

Part Plot the Rates using Matplotlib

All done in Python pls

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock