Determine the extent of involvement, if any, of 5 consultants, specialists, or internal auditors. a NA...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

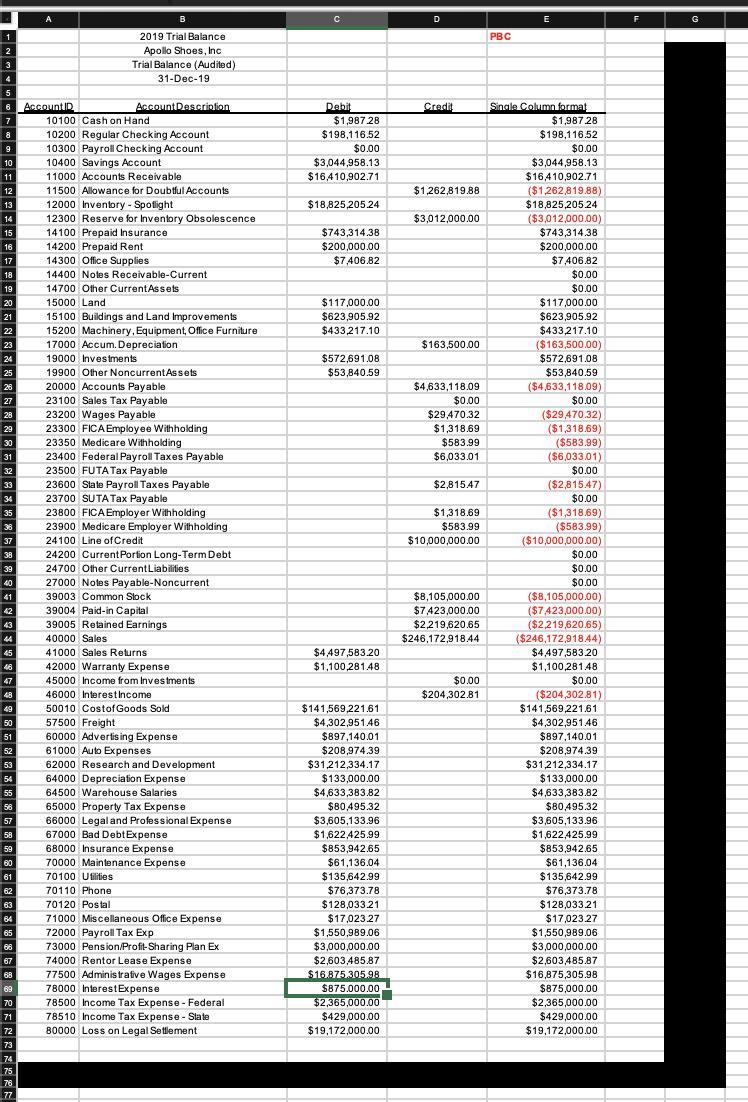

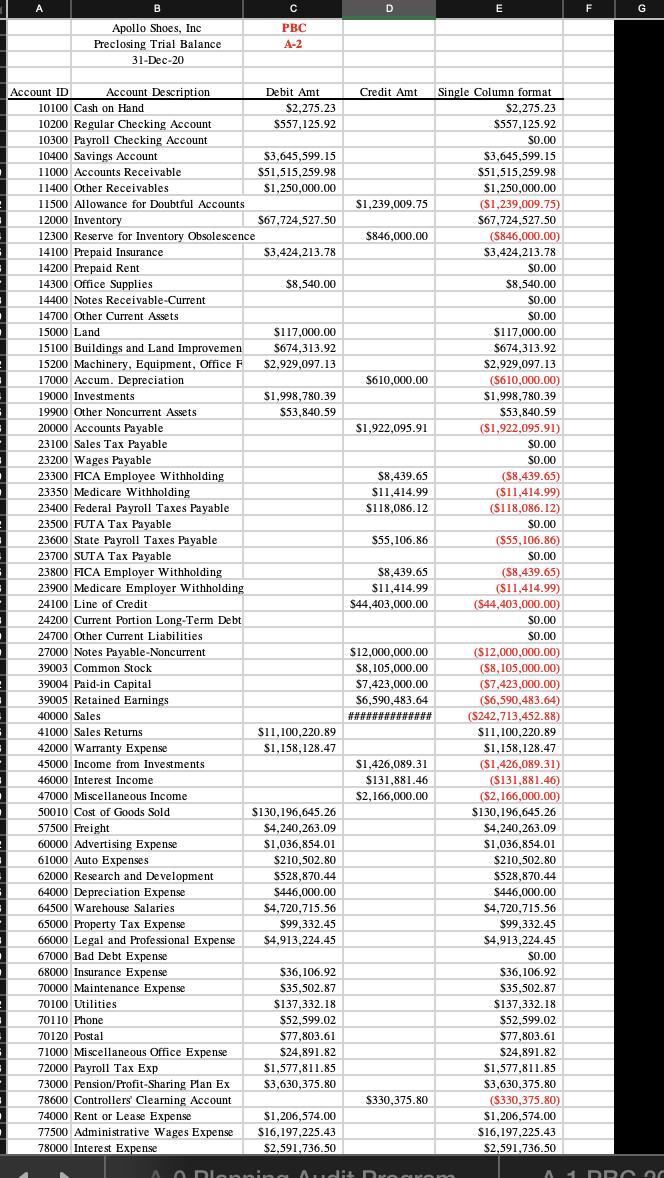

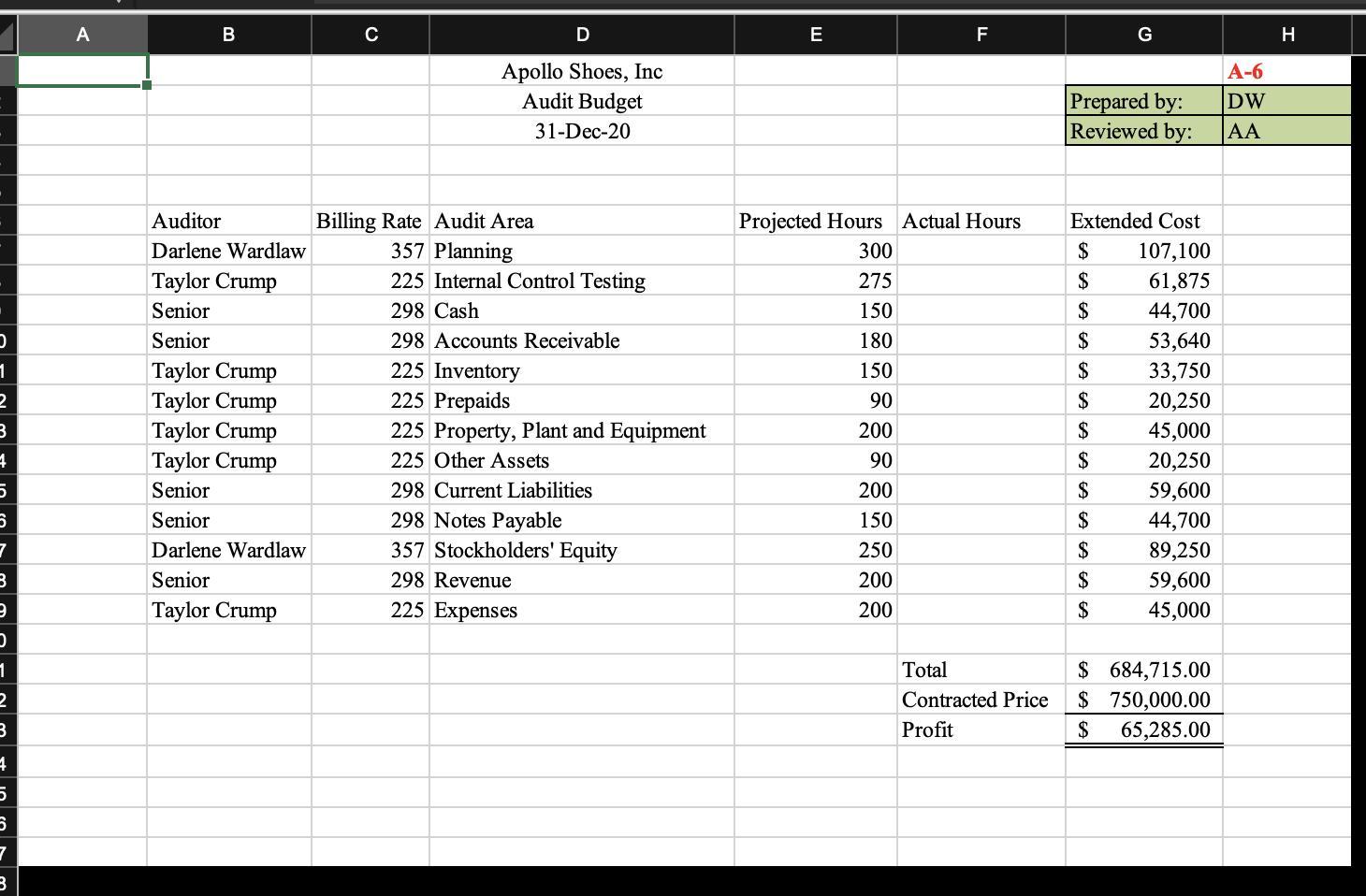

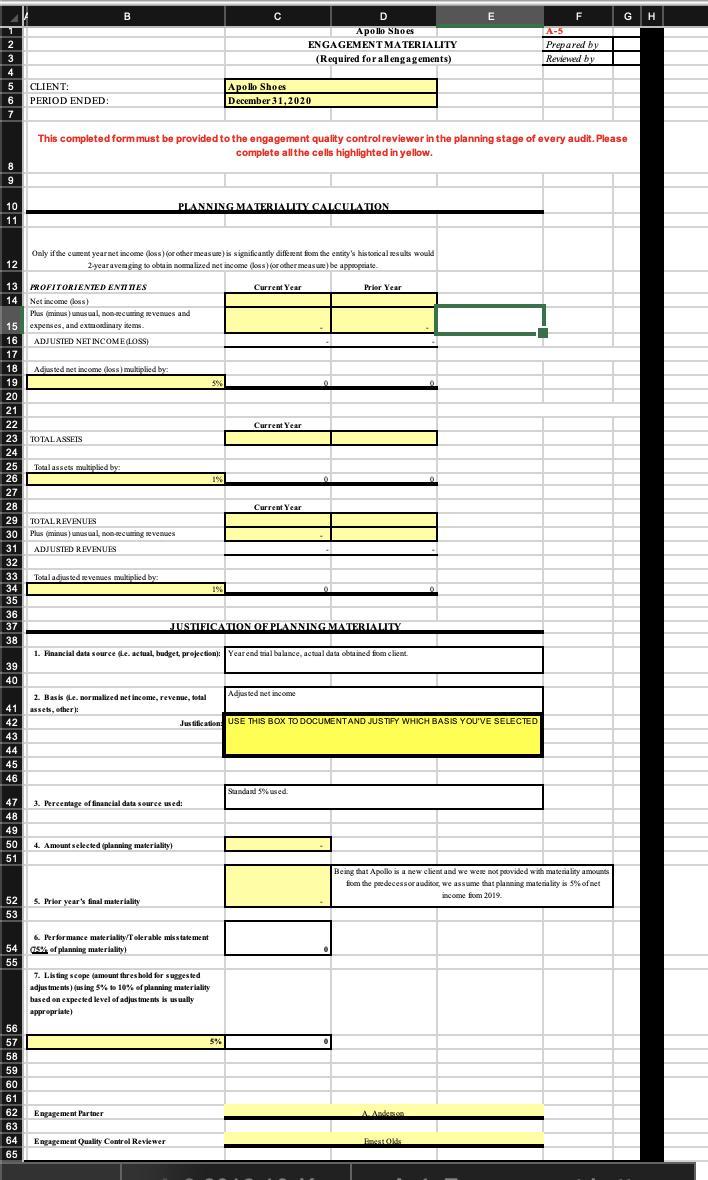

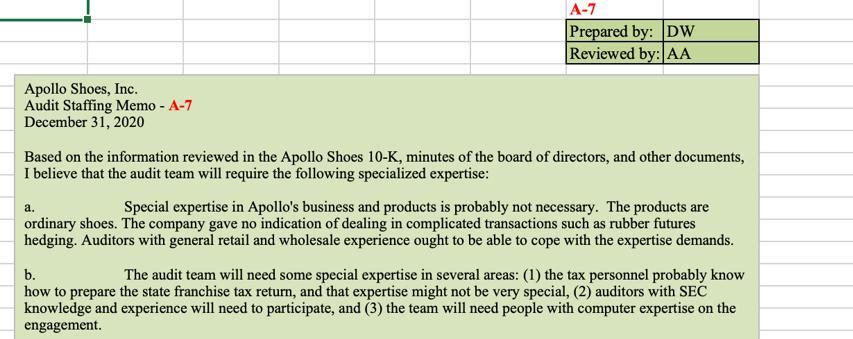

Determine the extent of involvement, if any, of 5 consultants, specialists, or internal auditors. a NA If the work of another is being used in the engagement, determine that it is used in accordance NA with professional standards. DW DW Some reliance on internal audit will be necessary. Apollo Director of Internal Audit - Karina Ramirez will be assisting on the audit, per my (DW) review of her qualifications and the organizational structure of Apollo I have concluded that she is both objective and competent. 1 2 3 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40 41 42 43 44 45 46 47 48 49 50 51 52 53 54 55 56 57 58 59 60 61 62 63 64 65 66 67 68 69 70 71 72 73 74 75 76 77 A Account ID B 2019 Trial Balance Apollo Shoes, Inc. Trial Balance (Audited) 31-Dec-19 Account Description 10100 Cash on Hand 10200 Regular Checking Account 10300 Payroll Checking Account 10400 Savings Account 11000 Accounts Receivable. 11500 Allowance for Doubtful Accounts 12000 Inventory - Spotlight 12300 Reserve for Inventory Obsolescence 14100 Prepaid Insurance 14200 Prepaid Rent 14300 Office Supplies 14400 Notes Receivable-Current 14700 Other Current Assets 15000 Land 15100 Buildings and Land Improvements. 15200 Machinery, Equipment, Office Furniture 17000 Accum. Depreciation 19000 Investments 19900 Other Noncurrent Assets 20000 Accounts Payable 23100 Sales Tax Payable 23200 Wages Payable 23300 FICA Employee Withholding 23350 Medicare Withholding 23400 Federal Payroll Taxes Payable 23500 FUTA Tax Payable 23600 State Payroll Taxes Payable 23700 SUTA Tax Payable 23800 FICA Employer Withholding 23900 Medicare Employer Withholding 24100 Line of Credit 24200 Current Portion Long-Term Debt 24700 Other Current Liabilities 27000 Notes Payable-Noncurrent 39003 Common Stock 39004 Paid-in Capital 39005 Retained Earnings 40000 Sales 41000 Sales Returns 42000 Warranty Expense 45000 Income from Investments 46000 Interest Income 50010 Costof Goods Sold 57500 Freight 60000 Advertising Expense 61000 Auto Expenses 62000 Research and Development 64000 Depreciation Expense 64500 Warehouse Salaries 65000 Property Tax Expense 66000 Legal and Professional Expense 67000 Bad Debt Expense 68000 Insurance Expense 70000 Maintenance Expense 70100 Utilities 70110 Phone 70120 Postal 71000 Miscellaneous Office Expense 72000 Payroll Tax Exp 73000 Pension/Profit-Sharing Plan Ex 74000 Rentor Lease Expense 77500 Administrative Wages Expense 78000 Interest Expense 78500 Income Tax Expense - Federal 78510 Income Tax Expense - State 80000 Loss on Legal Setlement C Debit $1,987.28 $198.116.52 $0.00 $3,044,958.13 $16,410,902.71 $18,825,205.24 $743,314.38 $200,000.00 $7.406.82 $117,000.00 $623,905.92 $433,217.10 $572,691.08 $53,840.59 $4,497,583.20 $1,100,281.48 $141,569,221.61 $4,302,95146 $897,140.01 $208,974.39 $31,212,334.17 $133,000.00 $4,633,383.82 $80,495.32 $3,605,133.96 $1,622,425.99 $853,942.65 $61,136.04 $135.642.99 $76,373.78 $128,033.21 $17,023.27 $1,550,989.06 $3,000,000.00 $2.603,485.87 $16.875.305.98 $875.000.00 $2,365,000.00 $429,000.00 $19,172,000.00 D Credit $1,262,819.88 $3,012,000.00 $163,500.00 $4,633,118.09 $0.00 $29,470.32 $1,318.69 $583.99 $6,033.01 $2,815.47 $1,318.69 $583.99 $10,000,000.00 $8,105,000.00 $7423,000.00 $2,219,620.65 $246,172,918.44 $0.00 $204,302.81 PBC E Single Column format $1,987.28 $198,116.52 $0.00 $3,044,958.13 $16,410,902.71 ($1,262,819.88) $18,825,205.24 ($3,012,000.00) $743,314.38 $200,000.00 $7,406.82 $0.00 $0.00 $117,000.00 $623,905.92 $433,217.10 ($163,500.00) $572,691.08 $53,840.59 ($4,633,118.09) $0.00 ($29,470.32) ($1,318.69) ($583.99) ($6,033.01) $0.00 ($2,815.47) $0.00 ($1,318.69) ($583.99) ($10,000,000.00) $0.00 $0.00 $0.00 ($8,105,000.00) ($7423,000.00) ($2,219,620.65) ($246,172,918.44) $4,497,583.20 $1,100,28148 $0.00 ($204,302.81) $141,569,221.61 $4,302,951.46 $897,140.01 $208,974.39 $31,212,334.17 $133,000.00 $4,633,383.82 $80,495.32 $3,605,133.96 $1,622,425.99 $853,942.65 $61,136.04 $135,642.99 $76,373.78 $128,033.21 $17,023.27 $1,550,989.06 $3,000,000.00 $2,603,485.87 $16,875,305.98 $875,000.00 $2,365,000.00 $429,000.00 $19,172,000.00 F G 1 Account ID B Apollo Shoes, Inc Preclosing Trial Balance: 31-Dec-20 Account Description. 10100 Cash on Hand 10200 Regular Checking Account 10300 Payroll Checking Account 10400 Savings Account 11000 Accounts Receivable 11400 Other Receivables 11500 Allowance for Doubtful Accounts. conomnog 12000 Inventory 12300 Reserve for Inventory Obsolescence 14100 Prepaid Insurance Proproparg 14200 Prepaid Rent. Expan 14300 Office Supplies *** St 14400 Notes Receivable-Current www 14700 Other Current Assets *600* 15000 Land ********** 15100 Buildings and Land Improvemen 15200 Machinery, Equipment, Office F 1000 17000 Accum. Depreciation wwwww 19000 Investments 19900 Other Noncurrent Assets * 20000 Accounts Payable *** mater 23100 Sales Tax Payable 53000 23200 Wages Payable 23300 FICA Employee Withholding 23350 Medicare Withholding 23400 Federal Payroll Taxes Payable 23500 FUTA Tax Payable 23600 State Payroll Taxes Payable 23700 SUTA Tax Payable 23800 FICA Employer Withholding 23900 Medicare Emplover Withholding 24100 Line of Credit 24200 Current Portion Long-Term Debt 24200 Current Portion 24700 Other Current Liabilities 27000 Notes Payable-Noncurrent 39003 Common Stock 39004 Paid-in Capital 39005 35009 Retained Earnings 40000 Sales 40000 Sales 41000 Sales Returns 71000 Sales 42000 Warranty Expense 45000 Income from Investments 46000 Interest Income 10000 47000 Miscellaneous Income 50010 Cost of Goods Sold 30010 COST OF 57500 Freight 60000 Advertising Expense 61000 Auto Expenses 62000 Research and Development www 64000 Depreciation Expense 64500 Warehouse Salaries 65000 Property Tax Expense supe 66000 Legal and Professional Expense Groning and Ad 67000 Bad Debt Expense CORPO 68000 Insurance Expense www. 70000 Maintenance Expense www 70100 Utilities. wwwww conte 70110 Phone 70120 Postal on 16 71000 Miscellaneous Office Expense 72000 Payroll Tax Exp. www 73000 Pension/Profit-Sharing Plan Ex 78600 Controllers' Clearning Account 74000 Rent or Lease Expense 77500 Administrative Wages Expense 78000 Interest Expense с PBC A-2 Debit Amt $2,275.23 $557,125.92 $3,645,599.15 $51,515,259.98 $1,250,000.00 $67,724,527.50 $3,424,213.78 $8,540.00 $117,000.00 $674,313.92 $2,929,097.13 $1,998,780.39 $53,840.59 $11,100,220.89 $1,158,128.47 $130,196,645.26 $4,240,263.09 $1,036,854.01 $210,502.80 $528,870.44 $446,000.00 $4,720,715.56 $99,332.45 $4,913,224.45 $36,106.92 $35,502.87 $137,332.18 $52,599.02 $77,803.61 $24,891.82 $1,577,811.85 $3.630.375.80 $1,206,574.00 $16,197.225.43 $2,591,736.50 D Credit Amt $1,239,009.75 $846,000.00 $610,000.00 $1,922,095.91 $8,439.65 $11,414.99 $118,086.12 $55,106.86 $8,439.65 $11,414.99 $44,403,000.00 $12,000,000.00 $8,105,000.00 $7,423,000.00 $6,590,483.64 ############## $1,426,089.31 $131,881.46 $2,166,000.00 $330,375.80 E Single Column format $2,275.23 $557,125.92 $0.00 O Planning Audit Drogrom $3,645,599.15 $51,515,259.98 $1,250,000.00 ($1,239,009.75) Cooperat $67,724,527.50 www.com ($846,000.00) 2015 20 $3,424,213.78 250.08 non Doku $0.00 www.we $8,540.00 Bronne $0.00 www.ne $0.00 www.www $117,000.00 2015.05 $674,313.92 CA $2,929,097.13 ($610,000.00) $1,998,780.39 400 $53,840.59 Coroa ($1,922,095.91) 20.00 $0.00 $0.00 ($8,439.65) ($11,414.99) ($118,086.12) $0.00 ($55,100.00 $0.00 ($8.439.0 ($11,414.99) ($44,403,000.00) ,000.00) $0.00 $0.00 ($12,000,000.00) 1.000.00 ($8,105.000.00) ($7,423,000.00) ($6,590,483.64) ($242,713,452.88) $11,100,220.89 $1,158,128.47 $1,156,126:47 ($1,426,089.31) ($131,881.46) ($2,166,000.00) $130,150,0.co $4,240,203.09 $1,036,854.01 $210.502.80 $210,502.80 $528,870.44 $446,000.00 $4,720,715.56 $99,332.45 $4,913,224.45 $0.00 826 10 $36,106.92 www. $35,502.87 ******** $137,332.18 AD FOR A $52,599.02 $77,803.61 RASPR $24,891.82 _ $1,577,811.85 $3,630,375.80 ($330,375.80) $1,206,574.00 $16,197,225.43 $2,591,736.50 F G A1 DRC 30 0 1 2 3 4 5 5 7 3 9 0 1 2 3 4 5 6 7 B A B Auditor Darlene Wardlaw Taylor Crump Senior Senior Taylor Crump Taylor Crump Crump Taylor Crump Senior Senior Darlene Wardlaw Senior Taylor Crump D Apollo Shoes, Inc Audit Budget 31-Dec-20 Billing Rate Audit Area 357 Planning 225 Internal Control Testing 298 Cash 298 Accounts Receivable 225 Inventory 225 Prepaids 225 Property, Plant and Equipment 225 Other Assets 298 Current Liabilities 298 Notes Payable 357 Stockholders' Equity 298 Revenue 225 Expenses E F Projected Hours Actual Hours 300 275 150 180 150 90 200 90 200 150 250 200 200 Total Contracted Price Profit Prepared by: Reviewed by: Extended Cost 107,100 61,875 44,700 53,640 33,750 20,250 45,000 20,250 59,600 44,700 89,250 59,600 45,000 $ $ $ $ $ $ $ $ $ $ $ $ $ $ 684,715.00 $ 750,000.00 $ 65,285.00 A-6 DW AA H 1 2 MASON~ ~~~~*~*~*88588388588429494 +9985 3 4 5 6 7 8 9 10 11 12 15 16 17 18 19 20 21 22 13 PROFITORIENTED ENTITIES 14 26 27 30 31 36 37 40 46 47 48 49 50 51 33 Total adjusted revenues multiplied by: 52 53 54 55 CLIENT: 56 57 58 PERIOD ENDED: 59 60 61 62 63 64 65 41 assets, other): B Net income (loss) Plus (minus) unusual, non-curring revenues and expenses, and extacadinary item ADJUSTED NET INCOME (LOSS) Adjusted net income (loss) multiplied by TOTAL ASSEIS Only if the curent year net income (loss) (or other measure) is significantly different from the entity's historical results would 2-year avenging to obtain normalized net income (loss) (or other measure) be appropriate. Total assets multiplied by: This completed form must be provided to the engagement quality control reviewer in the planning stage of every audit. Please complete all the cells highlighted in yellow. TOTAL REVENUES Plus (minus) usual, non-recurring revenues ADJUSTED REVENUES 2. Basis (Le normalized net income, revenue, total 4. Amount selected (planning materiality) 5. Prior year's final materiality PLANNING MATERIALITY CALCULATION 3. Percentage of financial data source used: Engagement Partner 6. Performance materiality/Tolerable misstatement 75% of planning materiality) Engagement Quality Control Reviewer 5% 7. Listing scope (amount threshold for suggested adjustments) (using 5% to 10% of planning materiality based on expected level of adjustments is usually appropriate) C 1% 1% Apollo Shoes December 31, 2020 1. Financial data source (Le. actual, budget, projection): Year end trial balance, actual data obtained from client. Current Year JUSTIFICATION OF PLANNING MATERIALITY 5% D Apollo Shoes ENGAGEMENT MATERIALITY (Required for all engagements) Current Year Current Year Adjusted net income 0 Justification: USE THIS BOX TO DOCUMENT AND JUSTIFY WHICH BASIS YOU'VE SELECTED Standard 5% used Prior Year ● E A Andenon F Emeat Olds A-5 Prepared by Reviewed by Being that Apollo is a new client and we were not provided with materiality amounts from the predecessor auditor, we assume that planning materiality is 5% of net income from 2019. G H Apollo Shoes, Inc. Audit Staffing Memo - A-7 December 31, 2020 A-7 Prepared by: DW Reviewed by: AA Based on the information reviewed in the Apollo Shoes 10-K, minutes of the board of directors, and other documents, I believe that the audit team will require the following specialized expertise: a. Special expertise in Apollo's business and products is probably not necessary. The products are ordinary shoes. The company gave no indication of dealing in complicated transactions such as rubber futures hedging. Auditors with general retail and wholesale experience ought to be able to cope with the expertise demands. b. The audit team will need some special expertise in several areas: (1) the tax personnel probably know how to prepare the state franchise tax return, and that expertise might not be very special, (2) auditors with SEC knowledge and experience will need to participate, and (3) the team will need people with computer expertise on the engagement. Determine the extent of involvement, if any, of 5 consultants, specialists, or internal auditors. a NA If the work of another is being used in the engagement, determine that it is used in accordance NA with professional standards. DW DW Some reliance on internal audit will be necessary. Apollo Director of Internal Audit - Karina Ramirez will be assisting on the audit, per my (DW) review of her qualifications and the organizational structure of Apollo I have concluded that she is both objective and competent. 1 2 3 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40 41 42 43 44 45 46 47 48 49 50 51 52 53 54 55 56 57 58 59 60 61 62 63 64 65 66 67 68 69 70 71 72 73 74 75 76 77 A Account ID B 2019 Trial Balance Apollo Shoes, Inc. Trial Balance (Audited) 31-Dec-19 Account Description 10100 Cash on Hand 10200 Regular Checking Account 10300 Payroll Checking Account 10400 Savings Account 11000 Accounts Receivable. 11500 Allowance for Doubtful Accounts 12000 Inventory - Spotlight 12300 Reserve for Inventory Obsolescence 14100 Prepaid Insurance 14200 Prepaid Rent 14300 Office Supplies 14400 Notes Receivable-Current 14700 Other Current Assets 15000 Land 15100 Buildings and Land Improvements. 15200 Machinery, Equipment, Office Furniture 17000 Accum. Depreciation 19000 Investments 19900 Other Noncurrent Assets 20000 Accounts Payable 23100 Sales Tax Payable 23200 Wages Payable 23300 FICA Employee Withholding 23350 Medicare Withholding 23400 Federal Payroll Taxes Payable 23500 FUTA Tax Payable 23600 State Payroll Taxes Payable 23700 SUTA Tax Payable 23800 FICA Employer Withholding 23900 Medicare Employer Withholding 24100 Line of Credit 24200 Current Portion Long-Term Debt 24700 Other Current Liabilities 27000 Notes Payable-Noncurrent 39003 Common Stock 39004 Paid-in Capital 39005 Retained Earnings 40000 Sales 41000 Sales Returns 42000 Warranty Expense 45000 Income from Investments 46000 Interest Income 50010 Costof Goods Sold 57500 Freight 60000 Advertising Expense 61000 Auto Expenses 62000 Research and Development 64000 Depreciation Expense 64500 Warehouse Salaries 65000 Property Tax Expense 66000 Legal and Professional Expense 67000 Bad Debt Expense 68000 Insurance Expense 70000 Maintenance Expense 70100 Utilities 70110 Phone 70120 Postal 71000 Miscellaneous Office Expense 72000 Payroll Tax Exp 73000 Pension/Profit-Sharing Plan Ex 74000 Rentor Lease Expense 77500 Administrative Wages Expense 78000 Interest Expense 78500 Income Tax Expense - Federal 78510 Income Tax Expense - State 80000 Loss on Legal Setlement C Debit $1,987.28 $198.116.52 $0.00 $3,044,958.13 $16,410,902.71 $18,825,205.24 $743,314.38 $200,000.00 $7.406.82 $117,000.00 $623,905.92 $433,217.10 $572,691.08 $53,840.59 $4,497,583.20 $1,100,281.48 $141,569,221.61 $4,302,95146 $897,140.01 $208,974.39 $31,212,334.17 $133,000.00 $4,633,383.82 $80,495.32 $3,605,133.96 $1,622,425.99 $853,942.65 $61,136.04 $135.642.99 $76,373.78 $128,033.21 $17,023.27 $1,550,989.06 $3,000,000.00 $2.603,485.87 $16.875.305.98 $875.000.00 $2,365,000.00 $429,000.00 $19,172,000.00 D Credit $1,262,819.88 $3,012,000.00 $163,500.00 $4,633,118.09 $0.00 $29,470.32 $1,318.69 $583.99 $6,033.01 $2,815.47 $1,318.69 $583.99 $10,000,000.00 $8,105,000.00 $7423,000.00 $2,219,620.65 $246,172,918.44 $0.00 $204,302.81 PBC E Single Column format $1,987.28 $198,116.52 $0.00 $3,044,958.13 $16,410,902.71 ($1,262,819.88) $18,825,205.24 ($3,012,000.00) $743,314.38 $200,000.00 $7,406.82 $0.00 $0.00 $117,000.00 $623,905.92 $433,217.10 ($163,500.00) $572,691.08 $53,840.59 ($4,633,118.09) $0.00 ($29,470.32) ($1,318.69) ($583.99) ($6,033.01) $0.00 ($2,815.47) $0.00 ($1,318.69) ($583.99) ($10,000,000.00) $0.00 $0.00 $0.00 ($8,105,000.00) ($7423,000.00) ($2,219,620.65) ($246,172,918.44) $4,497,583.20 $1,100,28148 $0.00 ($204,302.81) $141,569,221.61 $4,302,951.46 $897,140.01 $208,974.39 $31,212,334.17 $133,000.00 $4,633,383.82 $80,495.32 $3,605,133.96 $1,622,425.99 $853,942.65 $61,136.04 $135,642.99 $76,373.78 $128,033.21 $17,023.27 $1,550,989.06 $3,000,000.00 $2,603,485.87 $16,875,305.98 $875,000.00 $2,365,000.00 $429,000.00 $19,172,000.00 F G 1 Account ID B Apollo Shoes, Inc Preclosing Trial Balance: 31-Dec-20 Account Description. 10100 Cash on Hand 10200 Regular Checking Account 10300 Payroll Checking Account 10400 Savings Account 11000 Accounts Receivable 11400 Other Receivables 11500 Allowance for Doubtful Accounts. conomnog 12000 Inventory 12300 Reserve for Inventory Obsolescence 14100 Prepaid Insurance Proproparg 14200 Prepaid Rent. Expan 14300 Office Supplies *** St 14400 Notes Receivable-Current www 14700 Other Current Assets *600* 15000 Land ********** 15100 Buildings and Land Improvemen 15200 Machinery, Equipment, Office F 1000 17000 Accum. Depreciation wwwww 19000 Investments 19900 Other Noncurrent Assets * 20000 Accounts Payable *** mater 23100 Sales Tax Payable 53000 23200 Wages Payable 23300 FICA Employee Withholding 23350 Medicare Withholding 23400 Federal Payroll Taxes Payable 23500 FUTA Tax Payable 23600 State Payroll Taxes Payable 23700 SUTA Tax Payable 23800 FICA Employer Withholding 23900 Medicare Emplover Withholding 24100 Line of Credit 24200 Current Portion Long-Term Debt 24200 Current Portion 24700 Other Current Liabilities 27000 Notes Payable-Noncurrent 39003 Common Stock 39004 Paid-in Capital 39005 35009 Retained Earnings 40000 Sales 40000 Sales 41000 Sales Returns 71000 Sales 42000 Warranty Expense 45000 Income from Investments 46000 Interest Income 10000 47000 Miscellaneous Income 50010 Cost of Goods Sold 30010 COST OF 57500 Freight 60000 Advertising Expense 61000 Auto Expenses 62000 Research and Development www 64000 Depreciation Expense 64500 Warehouse Salaries 65000 Property Tax Expense supe 66000 Legal and Professional Expense Groning and Ad 67000 Bad Debt Expense CORPO 68000 Insurance Expense www. 70000 Maintenance Expense www 70100 Utilities. wwwww conte 70110 Phone 70120 Postal on 16 71000 Miscellaneous Office Expense 72000 Payroll Tax Exp. www 73000 Pension/Profit-Sharing Plan Ex 78600 Controllers' Clearning Account 74000 Rent or Lease Expense 77500 Administrative Wages Expense 78000 Interest Expense с PBC A-2 Debit Amt $2,275.23 $557,125.92 $3,645,599.15 $51,515,259.98 $1,250,000.00 $67,724,527.50 $3,424,213.78 $8,540.00 $117,000.00 $674,313.92 $2,929,097.13 $1,998,780.39 $53,840.59 $11,100,220.89 $1,158,128.47 $130,196,645.26 $4,240,263.09 $1,036,854.01 $210,502.80 $528,870.44 $446,000.00 $4,720,715.56 $99,332.45 $4,913,224.45 $36,106.92 $35,502.87 $137,332.18 $52,599.02 $77,803.61 $24,891.82 $1,577,811.85 $3.630.375.80 $1,206,574.00 $16,197.225.43 $2,591,736.50 D Credit Amt $1,239,009.75 $846,000.00 $610,000.00 $1,922,095.91 $8,439.65 $11,414.99 $118,086.12 $55,106.86 $8,439.65 $11,414.99 $44,403,000.00 $12,000,000.00 $8,105,000.00 $7,423,000.00 $6,590,483.64 ############## $1,426,089.31 $131,881.46 $2,166,000.00 $330,375.80 E Single Column format $2,275.23 $557,125.92 $0.00 O Planning Audit Drogrom $3,645,599.15 $51,515,259.98 $1,250,000.00 ($1,239,009.75) Cooperat $67,724,527.50 www.com ($846,000.00) 2015 20 $3,424,213.78 250.08 non Doku $0.00 www.we $8,540.00 Bronne $0.00 www.ne $0.00 www.www $117,000.00 2015.05 $674,313.92 CA $2,929,097.13 ($610,000.00) $1,998,780.39 400 $53,840.59 Coroa ($1,922,095.91) 20.00 $0.00 $0.00 ($8,439.65) ($11,414.99) ($118,086.12) $0.00 ($55,100.00 $0.00 ($8.439.0 ($11,414.99) ($44,403,000.00) ,000.00) $0.00 $0.00 ($12,000,000.00) 1.000.00 ($8,105.000.00) ($7,423,000.00) ($6,590,483.64) ($242,713,452.88) $11,100,220.89 $1,158,128.47 $1,156,126:47 ($1,426,089.31) ($131,881.46) ($2,166,000.00) $130,150,0.co $4,240,203.09 $1,036,854.01 $210.502.80 $210,502.80 $528,870.44 $446,000.00 $4,720,715.56 $99,332.45 $4,913,224.45 $0.00 826 10 $36,106.92 www. $35,502.87 ******** $137,332.18 AD FOR A $52,599.02 $77,803.61 RASPR $24,891.82 _ $1,577,811.85 $3,630,375.80 ($330,375.80) $1,206,574.00 $16,197,225.43 $2,591,736.50 F G A1 DRC 30 0 1 2 3 4 5 5 7 3 9 0 1 2 3 4 5 6 7 B A B Auditor Darlene Wardlaw Taylor Crump Senior Senior Taylor Crump Taylor Crump Crump Taylor Crump Senior Senior Darlene Wardlaw Senior Taylor Crump D Apollo Shoes, Inc Audit Budget 31-Dec-20 Billing Rate Audit Area 357 Planning 225 Internal Control Testing 298 Cash 298 Accounts Receivable 225 Inventory 225 Prepaids 225 Property, Plant and Equipment 225 Other Assets 298 Current Liabilities 298 Notes Payable 357 Stockholders' Equity 298 Revenue 225 Expenses E F Projected Hours Actual Hours 300 275 150 180 150 90 200 90 200 150 250 200 200 Total Contracted Price Profit Prepared by: Reviewed by: Extended Cost 107,100 61,875 44,700 53,640 33,750 20,250 45,000 20,250 59,600 44,700 89,250 59,600 45,000 $ $ $ $ $ $ $ $ $ $ $ $ $ $ 684,715.00 $ 750,000.00 $ 65,285.00 A-6 DW AA H 1 2 MASON~ ~~~~*~*~*88588388588429494 +9985 3 4 5 6 7 8 9 10 11 12 15 16 17 18 19 20 21 22 13 PROFITORIENTED ENTITIES 14 26 27 30 31 36 37 40 46 47 48 49 50 51 33 Total adjusted revenues multiplied by: 52 53 54 55 CLIENT: 56 57 58 PERIOD ENDED: 59 60 61 62 63 64 65 41 assets, other): B Net income (loss) Plus (minus) unusual, non-curring revenues and expenses, and extacadinary item ADJUSTED NET INCOME (LOSS) Adjusted net income (loss) multiplied by TOTAL ASSEIS Only if the curent year net income (loss) (or other measure) is significantly different from the entity's historical results would 2-year avenging to obtain normalized net income (loss) (or other measure) be appropriate. Total assets multiplied by: This completed form must be provided to the engagement quality control reviewer in the planning stage of every audit. Please complete all the cells highlighted in yellow. TOTAL REVENUES Plus (minus) usual, non-recurring revenues ADJUSTED REVENUES 2. Basis (Le normalized net income, revenue, total 4. Amount selected (planning materiality) 5. Prior year's final materiality PLANNING MATERIALITY CALCULATION 3. Percentage of financial data source used: Engagement Partner 6. Performance materiality/Tolerable misstatement 75% of planning materiality) Engagement Quality Control Reviewer 5% 7. Listing scope (amount threshold for suggested adjustments) (using 5% to 10% of planning materiality based on expected level of adjustments is usually appropriate) C 1% 1% Apollo Shoes December 31, 2020 1. Financial data source (Le. actual, budget, projection): Year end trial balance, actual data obtained from client. Current Year JUSTIFICATION OF PLANNING MATERIALITY 5% D Apollo Shoes ENGAGEMENT MATERIALITY (Required for all engagements) Current Year Current Year Adjusted net income 0 Justification: USE THIS BOX TO DOCUMENT AND JUSTIFY WHICH BASIS YOU'VE SELECTED Standard 5% used Prior Year ● E A Andenon F Emeat Olds A-5 Prepared by Reviewed by Being that Apollo is a new client and we were not provided with materiality amounts from the predecessor auditor, we assume that planning materiality is 5% of net income from 2019. G H Apollo Shoes, Inc. Audit Staffing Memo - A-7 December 31, 2020 A-7 Prepared by: DW Reviewed by: AA Based on the information reviewed in the Apollo Shoes 10-K, minutes of the board of directors, and other documents, I believe that the audit team will require the following specialized expertise: a. Special expertise in Apollo's business and products is probably not necessary. The products are ordinary shoes. The company gave no indication of dealing in complicated transactions such as rubber futures hedging. Auditors with general retail and wholesale experience ought to be able to cope with the expertise demands. b. The audit team will need some special expertise in several areas: (1) the tax personnel probably know how to prepare the state franchise tax return, and that expertise might not be very special, (2) auditors with SEC knowledge and experience will need to participate, and (3) the team will need people with computer expertise on the engagement.

Expert Answer:

Answer rating: 100% (QA)

Based on the information provided I would recommend the following extent of involvement for each of the 5 consultants specialists or internal auditors ... View the full answer

Related Book For

Auditing and Assurance Services A Systematic Approach

ISBN: 978-1259162343

9th edition

Authors: William Messier, Steven Glover, Douglas Prawitt

Posted Date:

Students also viewed these accounting questions

-

George Oldman, a Toronto antiquerug dealer, advertises in the January issue of the Rug Dealer's Rag magazine: For sale: 150yearold Sultanabad Persian. 2.5 m x 4 m. Exceptional quality. Phone (416)...

-

Hyten Corporation On June 5, 1998, a meeting was held at Hyten Corporation, between Bill Knapp, Director of Marketing/Sales, and John Rich, director of engineering. The purpose of the meeting was to...

-

In 2014, the International Accounting and Assurance Standards Board asked stakeholders to provide feedback on its proposed changes to the audit reporting model. In its comments on the proposed...

-

According to a study conducted by the Gallup organization, the proportion of Americans who are afraid to y is 0.10. A random sample of 1100 Americans results in 121 indicating that they are afraid to...

-

The cylindrical tank in Fig P2.70 has a 35-cm-high cylindrical insert in the bottom. The pressure at point B is 156 kPa. Find (a) The pressure in the air space; and (b) The force on the top of the...

-

During the year, cost of goods sold was $80,000; income from operations was $76,000; income tax expense was $16,000; interest expense was $12,000; and selling, general, and administrative expenses...

-

Water from a garden hose is sprayed against your car to rinse dirt from it. Estimate the force that the water exerts on the car. List all assumptions and show calculations.

-

Attendance at Orlandos newest Disneylike attrac-tion, Lego World, has been as follows: Compute seasonal indices using all of thedata. GUESTS ON THOUSANDS) GUESTS QUARTER Winter Year 1 Spring Year 1...

-

CASE STUDY: PROFITS AND THE EVOLUTION OF THE COMPUTER INDUSTRY. When profits in a given industry are higher than in other industries, new firms will attempt to enter that industry. CASE STUDY:...

-

1. A building owned by Hopewell Company was recently valued at $850,000 by a real estate expert. The president of the company is questioning the accuracy of the firm's latest balance sheet because it...

-

a) Suppose we have a distillation process where the objective is to separate components of a mixture in the input stream. The relationship between the input variable, temperature, and the output...

-

What kind of organization might want to follow a different political model of IT than the federal model? Describe how a manager provides leadership with respect to infonnation technology in the...

-

A son will receive 3000 pesos at the beginning of each 3 months for 4 years. What is the sum of this annuity at the end of the 4th year if the interest rate is 6% compounded quarterly?

-

All of the following are 'principles of prudence' EXCEPT for: Group of answer choices Trustees have a duty to determine the appropriate levels of risk. Trustees have a duty to avoid high fees. Sound...

-

Identify and post an example of public relations that you come across. Discuss three ways noted in the example that help to articulate a firm's value proposition to its audience.

-

How do emerging technologies, such as artificial intelligence and machine learning, impact stock valuation, and how can investors leverage these tools to improve their analysis?

-

Define forensic psychology, and elaborate on how forensic psychology is different from forensic science. Provide at least one example of how forensic psychologists and forensic science practitioners...

-

When is the indirect pattern appropriate, and what are the benefits of using it?

-

In 2011, your firm issued an unmodified report on Tosi Corporation, a private company. During 2013, Tosi entered its first lease transaction, which you have determined is material but not pervasive...

-

a. Go to the AICPAs website (www. aicpa.org). Find the AICPAs mission statement (currently under the link About the AICPA). Read and briefly summarize the AICPAs mission as described in its mission...

-

Visit the SECs website ( www. sec.gov), and identify a company that has been recently cited for problems related to property, plant, and equipment or lease accounting ( e. g., in years past, many...

-

Consider the situation illustrated in Figure 25. 11. A positively charged particle is lifted against the uniform electric field of a negatively charged plate. Ignoring any gravitational interactions,...

-

A positively charged particle is moved from point A to point B in the electric field of the massive, stationary, positively charged object in Figure 25. 12. (a) Is the electrostatic work done on the...

-

Figure 25. 13 shows both the electric field lines and the equipotentials associated with the given charge distribution. (a) Is the potential at point A higher than, lower than, or the same as the...

Study smarter with the SolutionInn App