Question: . Determine the option types that you will consider based on the exchange rate quotes provided by your bank. Remember we will long or short

. Determine the option types that you will consider based on the exchange rate quotes provided by your bank. Remember we will long or short the base currencies (in this case study the currencies that are not $) and the FV of premium cost is based on the borrowing cost of $ for the time period of the option. For example if it is a 3 month option, then the interest rate that should be applied is United States 3 month borrowing rate of 2.687%/4 = 0.67175%). Calculate the total cost of using options as hedging instrument for the import from Australia (Complete Table 4 on the separate answer sheet)

. Determine the option types that you will consider based on the exchange rate quotes provided by your bank. Remember we will long or short the base currencies (in this case study the currencies that are not $) and the FV of premium cost is based on the borrowing cost of $ for the time period of the option. For example if it is a 3 month option, then the interest rate that should be applied is United States 3 month borrowing rate of 2.687%/4 = 0.67175%). Calculate the total cost of using options as hedging instrument for the import from Australia (Complete Table 4 on the separate answer sheet)

Table 4: Australia import cost with option hedge: (8 marks)

| Type of option (Call or put) and on what currency? | Total premium cost for import | Total cost of option in $ (Strike plus premium) | Option hedge breakeven exchange rate | |

| Show your workings and answers in the columns

|

| $ premium x total AUD value of import x (1+i) | (Strike price x total AUD value of import) + total premium | Total cost of option in $/ Total AUD value of transaction |

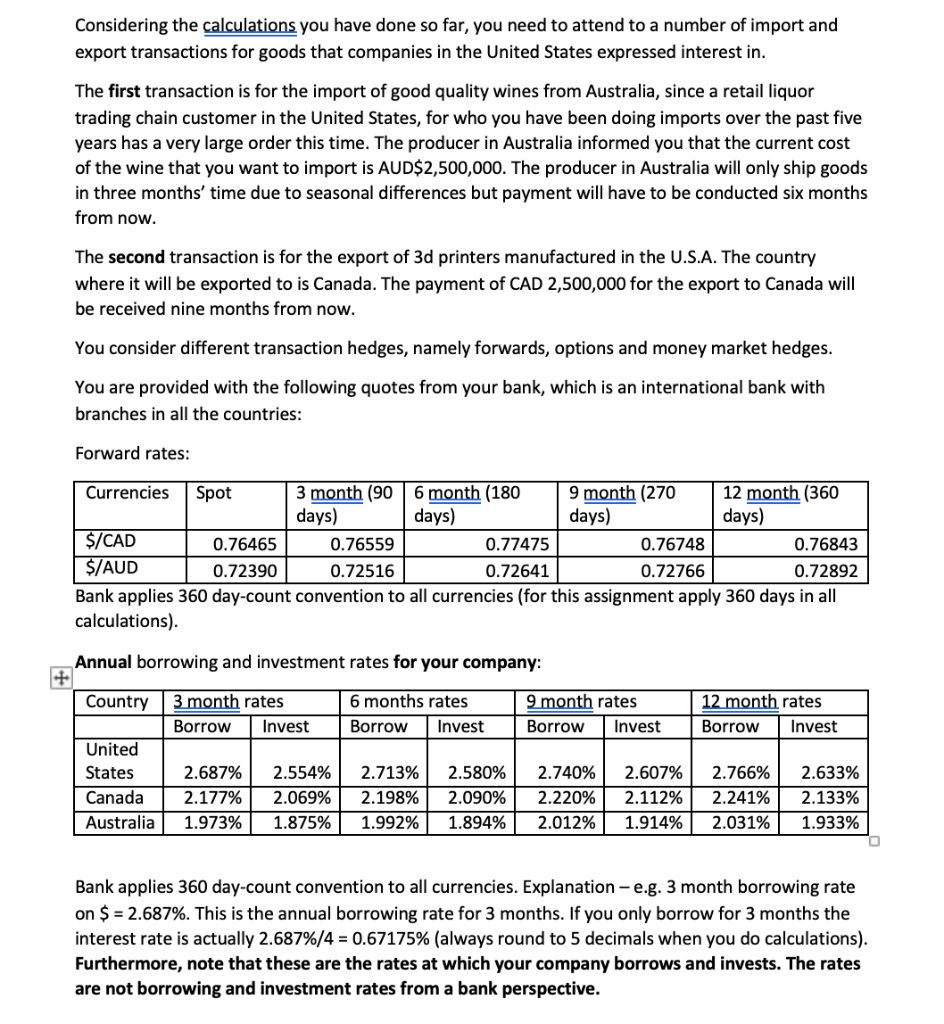

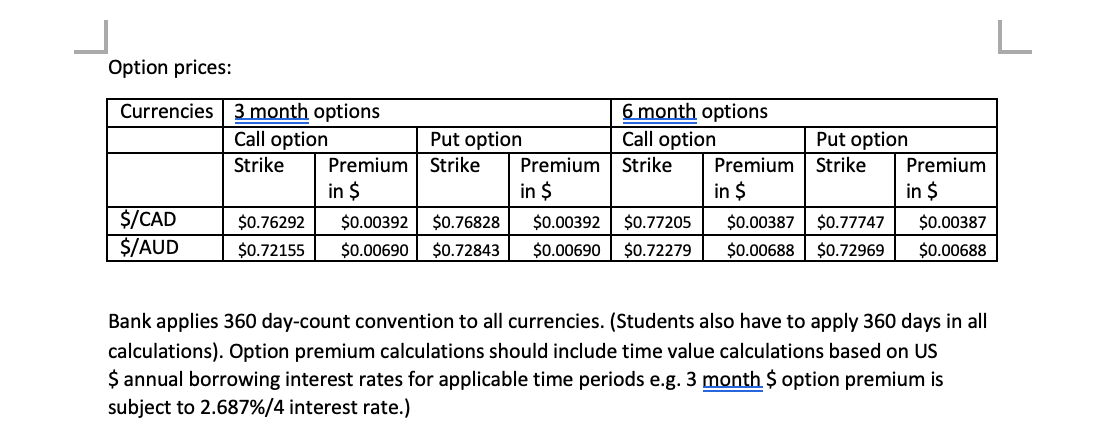

Considering the calculations you have done so far, you need to attend to a number of import and export transactions for goods that companies in the United States expressed interest in. The first transaction is for the import of good quality wines from Australia, since a retail liquor trading chain customer in the United States, for who you have been doing imports over the past five years has a very large order this time. The producer in Australia informed you that the current cost of the wine that you want to import is AUD$2,500,000. The producer in Australia will only ship goods in three months' time due to seasonal differences but payment will have to be conducted six months from now. The second transaction is for the export of 3d printers manufactured in the U.S.A. The country where it will be exported to is Canada. The payment of CAD 2,500,000 for the export to Canada will be received nine months from now. You consider different transaction hedges, namely forwards, options and money market hedges. You are provided with the following quotes from your bank, which is an international bank with branches in all the countries: Forward rates: Currencies Spot 3 month (90 6 month (180 9 month (270 12 month (360 days) days) days) days) $/CAD 0.76465 0.76559 0.77475 0.76748 0.76843 $/AUD 0.72390 0.72516 0.72641 0.72766 0.72892 Bank applies 360 day-count convention to all currencies (for this assignment apply 360 days in all calculations). Annual borrowing and investment rates for your company: Country 3 month rates Borrow Invest 6 months rates Borrow Invest 9 month rates Borrow Invest 12 month rates Borrow Invest United States Canada Australia 2.687% 2.177% 1.973% 2.554% 2.069% 1.875% 2.713% 2.198% 1.992% 2.580% 2.090% 1.894% 2.740% 2.220% 2.012% 2.607% 2.112% 1.914% 2.766% 2.241% 2.031% 2.633% 2.133% 1.933% Bank applies 360 day-count convention to all currencies. Explanation - e.g. 3 month borrowing rate on $ = 2.687%. This is the annual borrowing rate for 3 months. If you only borrow for 3 months the interest rate is actually 2.687%/4 = 0.67175% (always round to 5 decimals when you do calculations). Furthermore, note that these are the rates at which your company borrows and invests. The rates are not borrowing and investment rates from a bank perspective. Option prices: Currencies 3 month options 6 month options Call option Put option Call option Put option Strike Premium Strike Premium Strike Premium Strike Premium in $ in $ in $ in $ $0.76292 $0.00392 $0.76828 $0.00392 $0.77205 $0.00387 $0.77747 $0.00387 $0.72155 $0.00690 $0.72843 $0.00690 $0.72279 $0.00688 $0.72969 $0.00688 $/CAD $/AUD Bank applies 360 day-count convention to all currencies. (Students also have to apply 360 days in all calculations). Option premium calculations should include time value calculations based on US $ annual borrowing interest rates for applicable time periods e.g. 3 month $ option premium is subject to 2.687%/4 interest rate.)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts