Question: - di, eae S3igees CHARTERED 4 5 HERR COMPTABLES = ee PROFESSIONAL =e A PROFESSIONNELS i. or ACCOUNTANTS | AGREES i Finance Integrated Problem 3

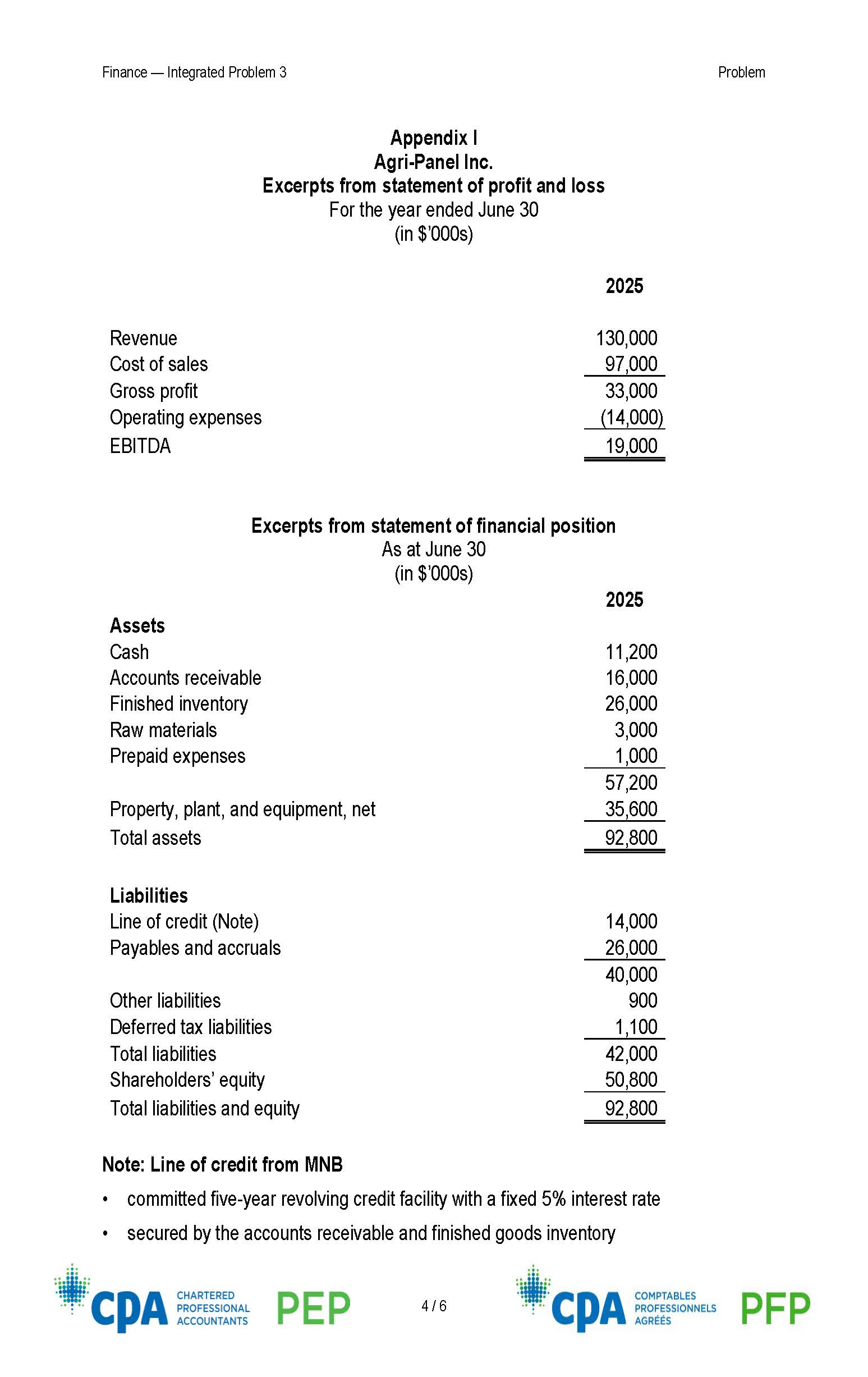

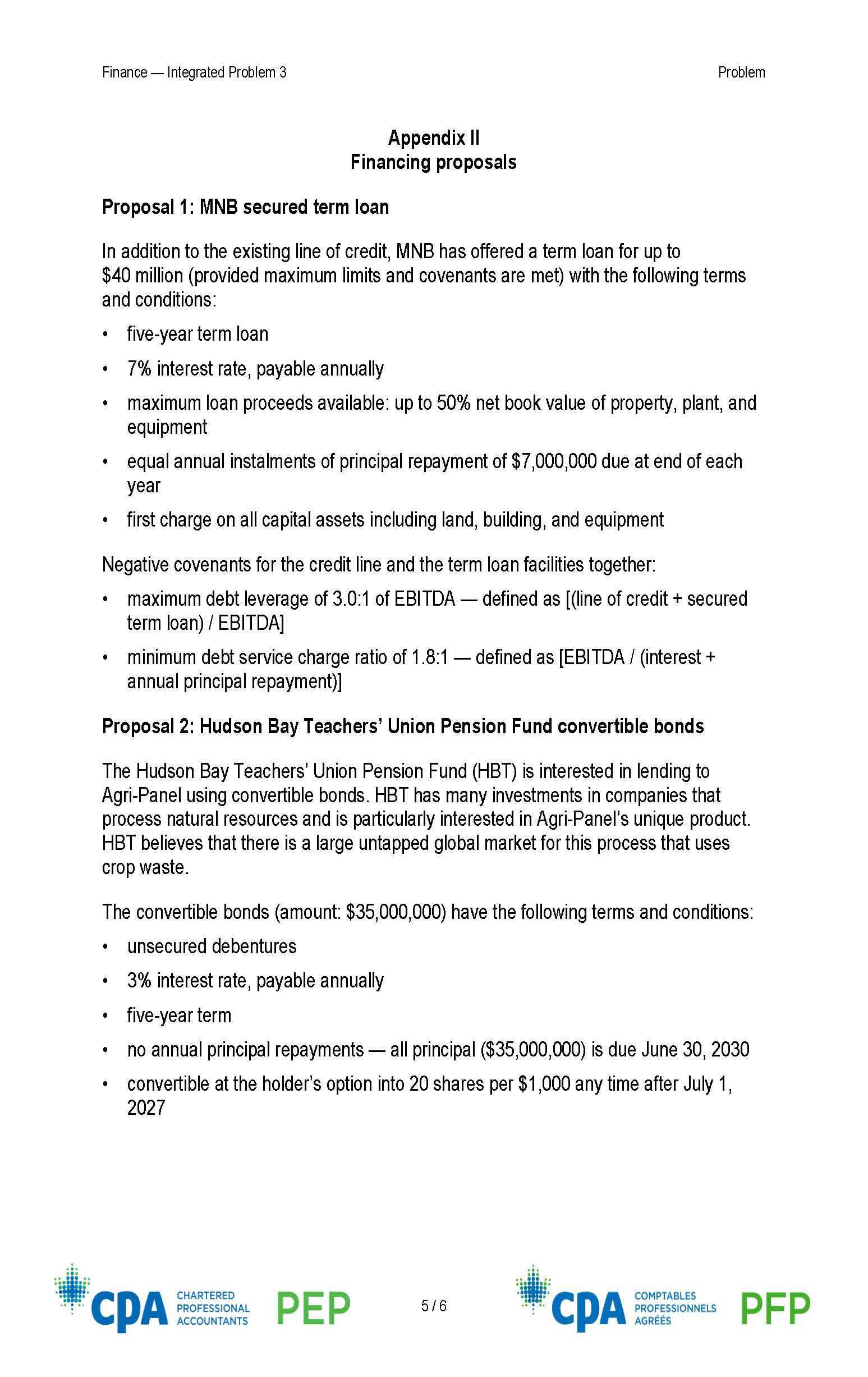

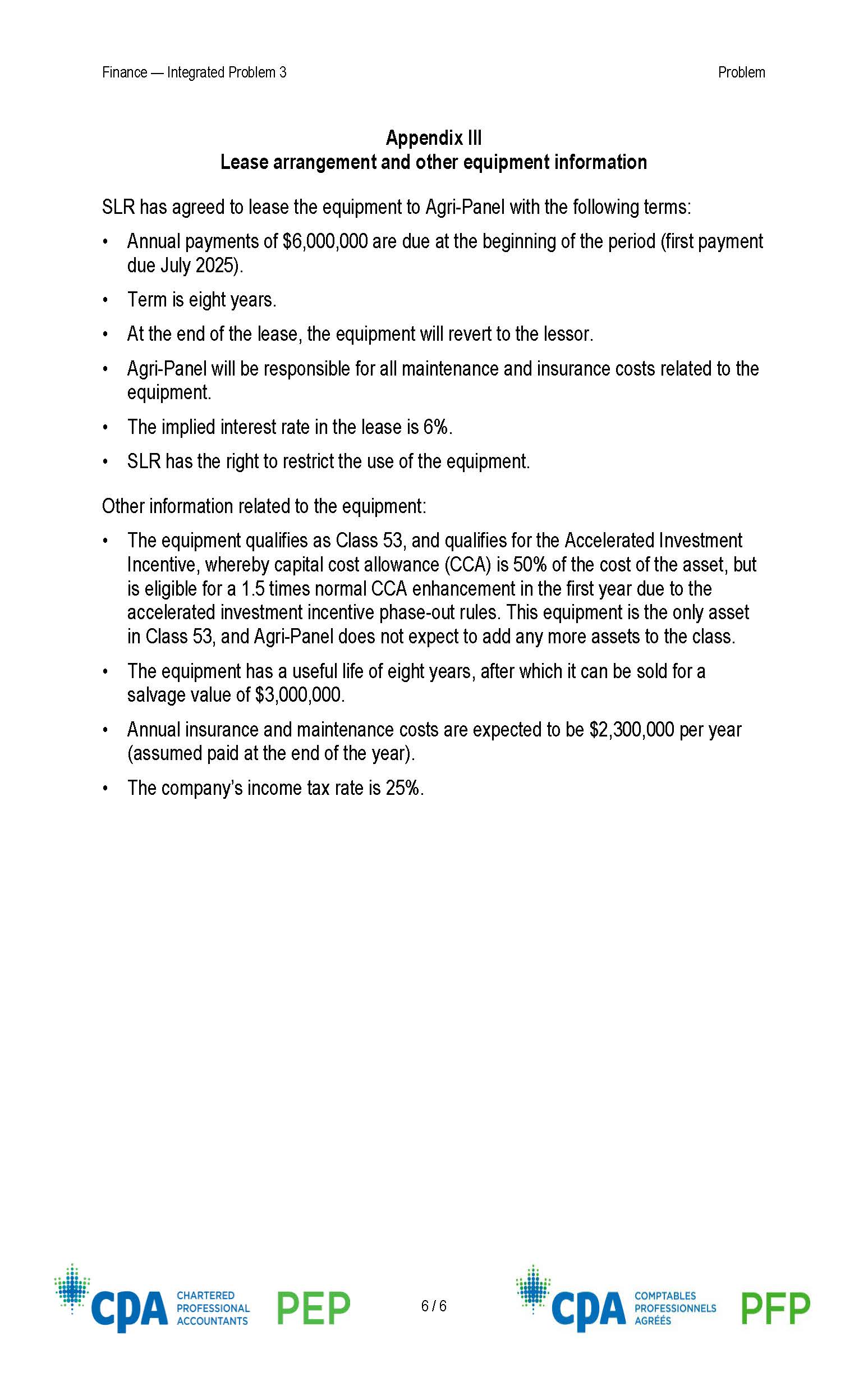

- di, eae \"S3igees CHARTERED 4 5 HERR COMPTABLES = ee PROFESSIONAL =e A PROFESSIONNELS i. or ACCOUNTANTS | AGREES i Finance Integrated Problem 3 Scenario (100 minutes) Agri-Panel Inc. is a manufacturer of high-density fibreboard panels. The company, based in Manitoba, has been in business for nearly 28 years and is owned equally by two brothers, Derek and Alex Maise. Currently, there are 1,000,000 common shares outstanding. The company follows IFRS. Extracts from the financial statements are included in Appendix I. Agri-Panel blends agricultural fibre from crop waste, which is essentially free, with wood chips to form the panels. The product has a very good reputation in the market, so Agri- Panel can charge premium prices and achieve higher than average operating margins. The company is looking to upgrade its equipment, which will cost $40,000,000. The shareholders have agreed to use $5,000,000 of the company's existing cash and finance the remaining balance of $35,000,000. The CFO has narrowed it down to two lenders (Appendix II}. In addition to the lenders, SLR Manufacturing Inc. (SLR), the manufacturer of the equipment, has offered to lease the equipment to Agri-Panel (Appendix III). You, CPA, work as an associate with Campbell and Associates LLP, a financial and business advisory firm. Derek and Alex have engaged your firm to assist them in assessing the financing alternatives. It is July 2, 2025, and you have been asked by your boss, Heather Larimer, to prepare a draft memo to Agri-Panel addressing the items below. Task #1 Calculate the maximum amount of loan proceeds available under the Manitoba National Bank (MNB) secured term loan, given the terms and conditions listed in Appendix II. Qualitatively compare the characteristics of the two sources of financing available to Agri-Panel. Your response should be no longer than six pages, excluding any Excel files. Chartered Professional Accountants of Canada. All rights reserved. No part of this publication may be reproduced or transmitted, in any form or by any means, without the prior written consent of CPA Canada. For information regarding permissions, please contact permissions@cpacanada.ca. 2024-08-14 Finance Integrated Problem 3 Problem Task #2 Prepare a forecast of after-tax cash flows for fiscal 2026, 2027, and 2028 for each of the two financing proposals, assuming the following: * Revenue increases 5% annually. * Earnings before interest taxes depreciation and amortization (EBITDA) margin is 15%. * Annual depreciation is $8,000,000 with equivalent annual capital cost allowance. * The line of credit balance will remain at $14,000 000 for the forecast period. Annual capital expenditures are $3,000,000 for each year. * Net working capital investments are $1,500,000 in fiscal 2026 and then increase 5% annually. Income tax rate is 25%. Assume that financing will be advanced in early July, and one year's worth of interest will be paid in fiscal 2026. Conclude on whether the company can comply with the loans' requirements for each of the years forecasted. Provide a recommendation to Agri-Panel as to which financing alternative is preferable, also considering the qualitative analysis provided in Task #1. Your response should be no longer than one page, excluding any Excel files. Task #3 Given the lease terms listed in Appendix III, discuss how the lease would be recognized in the financial statements. As part of this discussion, determine the impact on the statement of financial position when the lease is initially recognized as well as the impact on the statement of comprehensive income for fiscal 2026. Assume that the first lease payment would be paid in early July 2025. Your response should be no longer than two pages. \"i: ik. oeaRHE- CHARTERED . \"TERRE. COMPTABLES >= ; PROFESSIONAL 2/6 _ A PROFESSIONNELS La fmm fd ACCOUNTANTS AGREES i Finance - Integrated Problem 3 Problem Task #4 Explain the advantages and disadvantages of leasing versus borrowing to buy the equipment. Your response should be no longer than one page. Task #5 Calculate the net advantage of leasing to determine if leasing or buying is the more expensive option. Make a supported recommendation as to which financing, or lease option should be accepted. Your response should be no longer than one page, excluding any Excel files. CPA CHARTERED COMPTABLES PROFESSIONAL PEP 3/6 CPA PROFESSIONNELS ACCOUNTANTS AGREES PFPFinance Integrated Problem 3 Problem Appendix | Agri-Panel Inc. Excerpts from statement of profit and loss For the year ended June 30 (in $'000s) 2025 Revenue 130,000 Cost of sales 97 000 Gross profit 33,000 Operating expenses (14,000) EBITDA 19,000 Excerpts from statement of financial position As at June 30 (in $'000s) 2025 Assets Cash 11,200 Accounts receivable 16,000 Finished inventory 26,000 Raw materials 3,000 Prepaid expenses 1,000 57,200 Property, plant, and equipment, net 35,600 Total assets 92,800 Liabilities Line of credit (Note) 14,000 Payables and accruals 26,000 40,000 Other liabilities 900 Deferred tax liabilities 1,100 Total liabilities 42,000 Shareholders' equity 50,800 Total liabilities and equity 92,800 Note: Line of credit from MNB * committed five-year revolving credit facility with a fixed 5% interest rate * secured by the accounts receivable and finished goods inventory a CHARTERED o : \"ERR COMPTABLES = i PROFESSIONAL 4/6 cones PROFESSIONNELS i. ot 5 ACCOUNTANTS AGREES i Finance Integrated Problem 3 Problem Appendix Il Financing proposals Proposal 1: MNB secured term loan In addition to the existing line of credit, MNB has offered a term loan for up to $40 million (provided maximum limits and covenants are met) with the following terms and conditions: * five-year term loan * 7% interest rate, payable annually * maximum loan proceeds available: up to 50% net book value of property, plant, and equipment * equal annual instalments of principal repayment of $7,000 000 due at end of each year * first charge on all capital assets including land, building, and equipment Negative covenants for the credit line and the term loan facilities together: * maximum debt leverage of 3.0:1 of EBITDA defined as [(line of credit + secured term loan) / EBITDA] * minimum debt service charge ratio of 1.8:1 defined as [EBITDA / (interest + annual principal repayment)] Proposal 2: Hudson Bay Teachers' Union Pension Fund convertible bonds The Hudson Bay Teachers' Union Pension Fund (HBT) is interested in lending to Agri-Panel using convertible bonds. HBT has many investments in companies that process natural resources and is particularly interested in Agri-Panel's unique product. HBT believes that there is a large untapped global market for this process that uses crop waste. The convertible bonds (amount: $35,000,000) have the following terms and conditions: * unsecured debentures * 3% interest rate, payable annually * five-year term * no annual principal repayments all principal ($35,000,000) is due June 30, 2030 * convertible at the holder's option into 20 shares per $1,000 any time after July 1, 2027 \"i: ik. oeaRHE- CHARTERED . \"TERRE. COMPTABLES >= ; PROFESSIONAL 5/6 _ A PROFESSIONNELS La fmm fd ACCOUNTANTS AGREES i Finance Integrated Problem 3 Problem Appendix Ill Lease arrangement and other equipment information SLR has agreed to lease the equipment to Agri-Panel with the following terms: Annual payments of $6,000,000 are due at the beginning of the period (first payment due July 2025). Term is eight years. At the end of the lease, the equipment will revert to the lessor. Agri-Panel will be responsible for all maintenance and insurance costs related to the equipment. The implied interest rate in the lease is 6%. SLR has the right to restrict the use of the equipment. Other information related to the equipment: The equipment qualifies as Class 53, and qualifies for the Accelerated Investment Incentive, whereby capital cost allowance (CCA) is 50% of the cost of the asset, but is eligible for a 1.5 times normal CCA enhancement in the first year due to the accelerated investment incentive phase-out rules. This equipment is the only asset in Class 53, and Agri-Panel does not expect to add any more assets to the class. The equipment has a useful life of eight years, after which it can be sold for a salvage value of $3,000,000. Annual insurance and maintenance costs are expected to be $2,300,000 per year (assumed paid at the end of the year). The company's income tax rate is 25%. 3B: ah. if. s3e8ddez: ooigH- CHARTERED ; 2 \"TEER? COMPTABLES > cm ; PROFESSIONAL 6/6 oats A PROFESSIONNELS fla) fm LD ACCOUNTANTS AGREES a

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock

Students Have Also Explored These Related Finance Questions!