Question: do not use excel. i only need answers from part e onwards! part c has expexted return of 25% Question 1 You want to invest

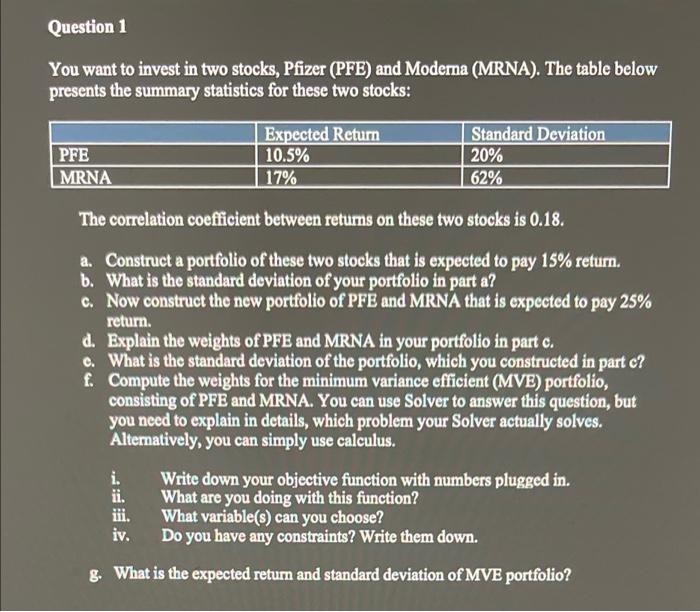

Question 1 You want to invest in two stocks, Pfizer (PFE) and Moderna (MRNA). The table below presents the summary statistics for these two stocks: PFE MRNA Expected Return 10.5% 17% Standard Deviation 20% 62% The correlation coefficient between returns on these two stocks is 0.18. a. Construct a portfolio of these two stocks that is expected to pay 15% return. b. What is the standard deviation of your portfolio in part a? c. Now construct the new portfolio of PFE and MRNA that is expected to pay 25% return. d. Explain the weights of PFE and MRNA in your portfolio in part c. e. What is the standard deviation of the portfolio, which you constructed in part c? f. Compute the weights for the minimum variance efficient (MVE) portfolio, consisting of PFE and MRNA. You can use Solver to answer this question, but you need to explain in details, which problem your Solver actually solves. Alternatively, you can simply use calculus. Write down your objective function with numbers plugged in. ii. What are you doing with this function? ii. What variable(s) can you choose? iv. Do you have any constraints? Write them down. g. What is the expected return and standard deviation of MVE portfolio

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts