Question: do part B please 8. (10 points) The term structure for (annual effective) interest rates is as follows for correspond- ing maturities: 1 year: 5%,

do part B please

do part B please

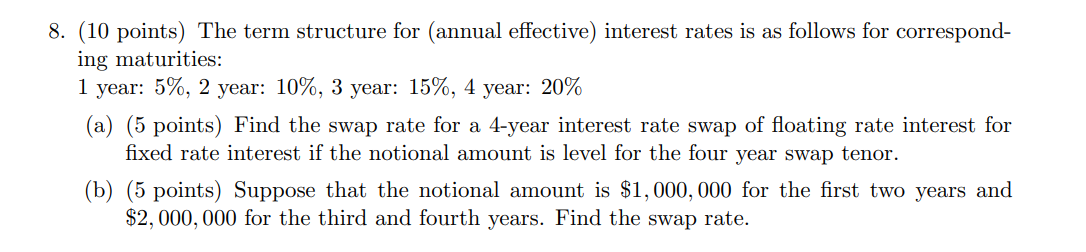

8. (10 points) The term structure for (annual effective) interest rates is as follows for correspond- ing maturities: 1 year: 5%, 2 year: 10%, 3 year: 15%, 4 year: 20% (a) (5 points) Find the swap rate for a 4-year interest rate swap of floating rate interest for fixed rate interest if the notional amount is level for the four year swap tenor. (b) (5 points) Suppose that the notional amount is $1,000,000 for the first two years and $2,000,000 for the third and fourth years. Find the swap rate

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock