Does Broadway benefit from acquiring Landmark? How can Harris justify a $120 million bid for Landmark? If

Fantastic news! We've Found the answer you've been seeking!

Question:

Does Broadway benefit from acquiring Landmark? How can Harris justify a $120 million bid for Landmark?

- If Harris were to proceed with the acquisition, which financing alternative should be chosen, and why? Would Broadway be capable of servicing its debt after the acquisition?

- Does Harris give up shareholder value by opting for the mix of debt & equity financing alternatives? What is the real cost of equity dilution?

- How do the two financing methods affect the value of the acquisition to existing shareholders of Broadway?

Transcribed Image Text:

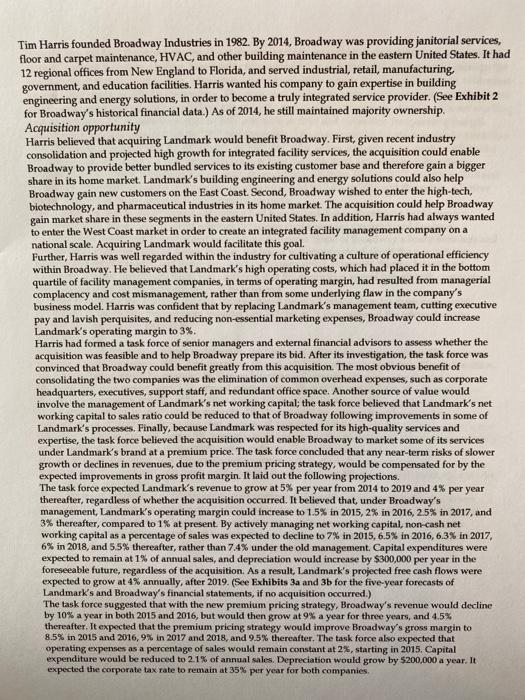

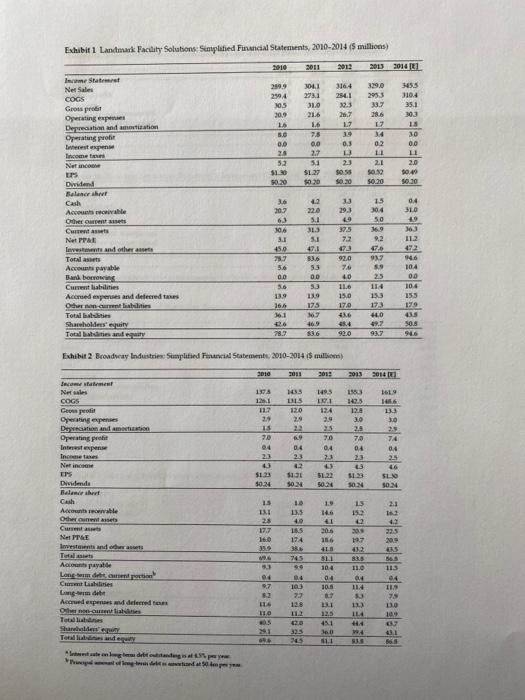

Tim Harris founded Broadway Industries in 1982. By 2014, Broadway was providing janitorial services, floor and carpet maintenance, HVAC, and other building maintenance in the eastern United States. It had 12 regional offices from New England to Florida, and served industrial, retail, manufacturing, government, and education facilities. Harris wanted his company to gain expertise in building engineering and energy solutions, in order to become a truly integrated service provider. (See Exhibit 2 for Broadway's historical financial data.) As of 2014, he still maintained majority ownership. Acquisition opportunity Harris believed that acquiring Landmark would benefit Broadway. First, given recent industry consolidation and projected high growth for integrated facility services, the acquisition could enable Broadway to provide better bundled services to its existing customer base and therefore gain a bigger share in its home market. Landmark's building engineering and energy solutions could also help Broadway gain new customers on the East Coast. Second, Broadway wished to enter the high-tech, biotechnology, and pharmaceutical industries in its home market. The acquisition could help Broadway gain market share in these segments in the eastern United States. In addition, Harris had always wanted to enter the West Coa market in order to create an integrated facility management company on a national scale. Acquiring Landmark would facilitate this goal. Further, Harris was well regarded within the industry for cultivating a culture of operational efficiency within Broadway. He believed that Landmark's high operating costs, which had placed it in the bottom quartile of facility management companies, in terms of operating margin, had resulted from managerial complacency and cost mismanagement, rather than from some underlying flaw in the company's business model. Harris was confident that by replacing Landmark's management team, cutting executive pay and lavish perquisites, and reducing non-essential marketing expenses, Broadway could increase Landmark's operating margin to 3%. Harris had formed a task force of senior managers and external financial advisors to assess whether the acquisition was feasible and to help Broadway prepare its bid. After its investigation, the task force was convinced that Broadway could benefit greatly from this acquisition. The most obvious benefit of consolidating the two companies was the elimination of common overhead expenses, such as corporate headquarters, executives, support staff, and redundant office space. Another source of value would involve the management of Landmark's net working capital; the task force believed that Landmark's net working capital to sales ratio could be reduced to that of Broadway following improvements in some of Landmark's processes. Finally, because Landmark was respected for its high-quality services and expertise, the task force believed the acquisition would enable Broadway to market some of its services under Landmark's brand at a premium price. The task force concluded that any near-term risks of slower growth or declines in revenues, due to the premium pricing strategy, would be compensated for by the expected improvements in gross profit margin. It laid out the following projections. The task force expected Landmark's revenue to grow at 5% per year from 2014 to 2019 and 4% per year thereafter, regardless of whether the acquisition occurred. It believed that, under Broadway's management, Landmark's operating margin could increase to 1.5% in 2015, 2% in 2016, 25% in 2017, and 3% thereafter, compared to 1% at present. By actively managing net working capital, non-cash net working capital as a percentage of sales was expected to decline to 7% in 2015, 6.5% in 2016, 6.3% in 2017, 6% in 2018, and 5.5% thereafter, rather than 7.4% under the old management. Capital expenditures were expected to remain at 1% of annual sales, and depreciation would increase by $300,000 per year in the foreseeable future, regardless of the acquisition. As a result, Landmark's projected free cash flows were expected to grow at 4% annually, after 2019. (See Exhibits 3a and 3b for the five-year forecasts of Landmark's and Broadway's financial statements, if no acquisition occurred.) The task force suggested that with the new premium pricing strategy, Broadway's revenue would decline by 10% a year in both 2015 and 2016, but would then grow at 9% a year for three years, and 4.5% thereafter. It expected that the premium pricing strategy would improve Broadway's gross margin to 8.5% in 2015 and 2016, 9% in 2017 and 2018, and 9.5% thereafter. The task force also expected that operating expenses as a percentage of sales would remain constant at 2%, starting in 2015. Capital expenditure would be reduced to 2.1% of annual sales. Depreciation would grow by $200,000 a year. It expected the corporate tax rate to remain at 35% per year for both companies. Tim Harris founded Broadway Industries in 1982. By 2014, Broadway was providing janitorial services, floor and carpet maintenance, HVAC, and other building maintenance in the eastern United States. It had 12 regional offices from New England to Florida, and served industrial, retail, manufacturing, government, and education facilities. Harris wanted his company to gain expertise in building engineering and energy solutions, in order to become a truly integrated service provider. (See Exhibit 2 for Broadway's historical financial data.) As of 2014, he still maintained majority ownership. Acquisition opportunity Harris believed that acquiring Landmark would benefit Broadway. First, given recent industry consolidation and projected high growth for integrated facility services, the acquisition could enable Broadway to provide better bundled services to its existing customer base and therefore gain a bigger share in its home market. Landmark's building engineering and energy solutions could also help Broadway gain new customers on the East Coast. Second, Broadway wished to enter the high-tech, biotechnology, and pharmaceutical industries in its home market. The acquisition could help Broadway gain market share in these segments in the eastern United States. In addition, Harris had always wanted to enter the West Coa market in order to create an integrated facility management company on a national scale. Acquiring Landmark would facilitate this goal. Further, Harris was well regarded within the industry for cultivating a culture of operational efficiency within Broadway. He believed that Landmark's high operating costs, which had placed it in the bottom quartile of facility management companies, in terms of operating margin, had resulted from managerial complacency and cost mismanagement, rather than from some underlying flaw in the company's business model. Harris was confident that by replacing Landmark's management team, cutting executive pay and lavish perquisites, and reducing non-essential marketing expenses, Broadway could increase Landmark's operating margin to 3%. Harris had formed a task force of senior managers and external financial advisors to assess whether the acquisition was feasible and to help Broadway prepare its bid. After its investigation, the task force was convinced that Broadway could benefit greatly from this acquisition. The most obvious benefit of consolidating the two companies was the elimination of common overhead expenses, such as corporate headquarters, executives, support staff, and redundant office space. Another source of value would involve the management of Landmark's net working capital; the task force believed that Landmark's net working capital to sales ratio could be reduced to that of Broadway following improvements in some of Landmark's processes. Finally, because Landmark was respected for its high-quality services and expertise, the task force believed the acquisition would enable Broadway to market some of its services under Landmark's brand at a premium price. The task force concluded that any near-term risks of slower growth or declines in revenues, due to the premium pricing strategy, would be compensated for by the expected improvements in gross profit margin. It laid out the following projections. The task force expected Landmark's revenue to grow at 5% per year from 2014 to 2019 and 4% per year thereafter, regardless of whether the acquisition occurred. It believed that, under Broadway's management, Landmark's operating margin could increase to 1.5% in 2015, 2% in 2016, 25% in 2017, and 3% thereafter, compared to 1% at present. By actively managing net working capital, non-cash net working capital as a percentage of sales was expected to decline to 7% in 2015, 6.5% in 2016, 6.3% in 2017, 6% in 2018, and 5.5% thereafter, rather than 7.4% under the old management. Capital expenditures were expected to remain at 1% of annual sales, and depreciation would increase by $300,000 per year in the foreseeable future, regardless of the acquisition. As a result, Landmark's projected free cash flows were expected to grow at 4% annually, after 2019. (See Exhibits 3a and 3b for the five-year forecasts of Landmark's and Broadway's financial statements, if no acquisition occurred.) The task force suggested that with the new premium pricing strategy, Broadway's revenue would decline by 10% a year in both 2015 and 2016, but would then grow at 9% a year for three years, and 4.5% thereafter. It expected that the premium pricing strategy would improve Broadway's gross margin to 8.5% in 2015 and 2016, 9% in 2017 and 2018, and 9.5% thereafter. The task force also expected that operating expenses as a percentage of sales would remain constant at 2%, starting in 2015. Capital expenditure would be reduced to 2.1% of annual sales. Depreciation would grow by $200,000 a year. It expected the corporate tax rate to remain at 35% per year for both companies.

Expert Answer:

Answer rating: 100% (QA)

1 Acquiring Landmark is the key to growth for Broadway It is a cheaper and faster way to increase sales and expand the company by opening new branches This will also help Broadway to achieve economies ... View the full answer

Related Book For

Corporate Finance

ISBN: 978-0077861759

10th edition

Authors: Stephen Ross, Randolph Westerfield, Jeffrey Jaffe

Posted Date:

Students also viewed these finance questions

-

Warf Computers has decided to proceed with the manufacture and distribution of the virtual keyboard (VK) the company has developed. To undertake this venture, the company needs to obtain equipment...

-

Warf Computers has decided to proceed with the manufacture and distribution of the virtual keyboard (VK) the company has developed. To undertake this venture, the company needs to obtain equipment...

-

Allison Hill moved to Canada on April 30th, 2019. She was born and raised in Belgium and moved to Canada to start a career in architecture. She earned $45,000 from May to December 2019 from her new...

-

Being employed as a casual barista in a local caf with a flourishing catering business called 'Brown's Caf' , where you are supervised by the caf owner, Jessica Williams. The company employs 20...

-

It is well known that warm air in a cooler environment rises. Now consider a warm mixture of air and gasoline on top of an open gasoline can. Do you think this gas mixture will rise in a cooler...

-

3.19 The following program skeleton asks for an angle in degrees and converts it to radians. The formatting of the final output is left to you. #include #include using namespace std; int main() {...

-

Ajax Savings Bank has certificate of deposit notes with a face value of $\$ 10,000$ with a $10 \%$ interest rate compounded daily. What is the current market price of the $\mathrm{CD}$ if the term of...

-

Toxaway Telephone Company has a $1,000 par value bond outstanding that pays 6 percent annual interest. If the yield to maturity is 8 percent, and remains so over the remaining life of the bond, the...

-

This image consists of 4 different photos together , top section is problem number 4,left middle section is questions, left lower section is problem number 2, right section is problem number 3...

-

The part shown is loaded at point C with 300 N in the positive x direction and at point E with 200 N in the positive y direction. The diameter of the bar ABD is 12 mm. Evaluate the likelihood of...

-

Following the instructions in the textbook on pp. 1-26 through 1-28, download: Amazons Form 10-K from the EDGAR website HTML and XLSX versions Alphabets Form 10-K from the EDGAR website HTML and XLSX...

-

How do religious and spiritual beliefs influence the formation and expression of personal values, and what tensions exist between religious freedoms and secular governance in pluralistic societies?

-

How do values shape public policy and governance structures, and what mechanisms exist for balancing competing values such as liberty and security, equality and meritocracy, or tradition and progress?

-

Anna was hired away from another corporation to became the new CEO of Tandy Corporation, a private, non-publicly-traded, calendar year corporation that uses the cash basis of accounting for tax...

-

Consider a company with net tangible assets valued at $500,000. The company determines the fair rate of return on these assets to be 8%. The company's total normalized earnings are estimated to be...

-

What role does language and discourse play in the construction and negotiation of identity, and how do linguistic practices reflect and reinforce social hierarchies, cultural norms, and power...

-

Shane purchased an appreciation gift for a loyal client. he was able to substantiate all the elements qualifying it as a 274(b) business gift. nevertheless, the deductible dollar amount would be...

-

A certain Christmas tree ornament is a silver sphere having a diameter of 8.50 cm. Determine an object location for which the size of the reflected image is three-fourths the size of the object. Use...

-

What is the present value of an annuity of $ 6,500 per year, with the first cash flow received three years from today and the last one received 25 years from today? Use a discount rate of 7 percent.

-

At 8 percent interest, how long does it take to double your money? To quadruple it?

-

What are the deltas of a call option and a put option with the following characteristics? What does the delta of the option tell you? Stock price = $67 Exercise price = $70 Risk-free rate = 5% per...

-

Using a financial calculator, solve for the unknowns in each of the following situations. a. On June 1, 2024, Holly Golightly purchases lakefront property from her neighbor, George Peppard, and...

-

Ed owns Oak Knoll Apartments. During the year, Fred, a tenant, moved to another state. Fred paid Ed \($1,000\) to cancel the two-year lease he had signed. Ed subsequently began renting the unit to...

-

In 2017, Harry and Mary purchased Series EE bonds, and in 2023 redeemed the bonds, receiving \($500\) of interest and \($1,500\) of principal. Their income from other sources totaled \($30,000.\)...

Study smarter with the SolutionInn App