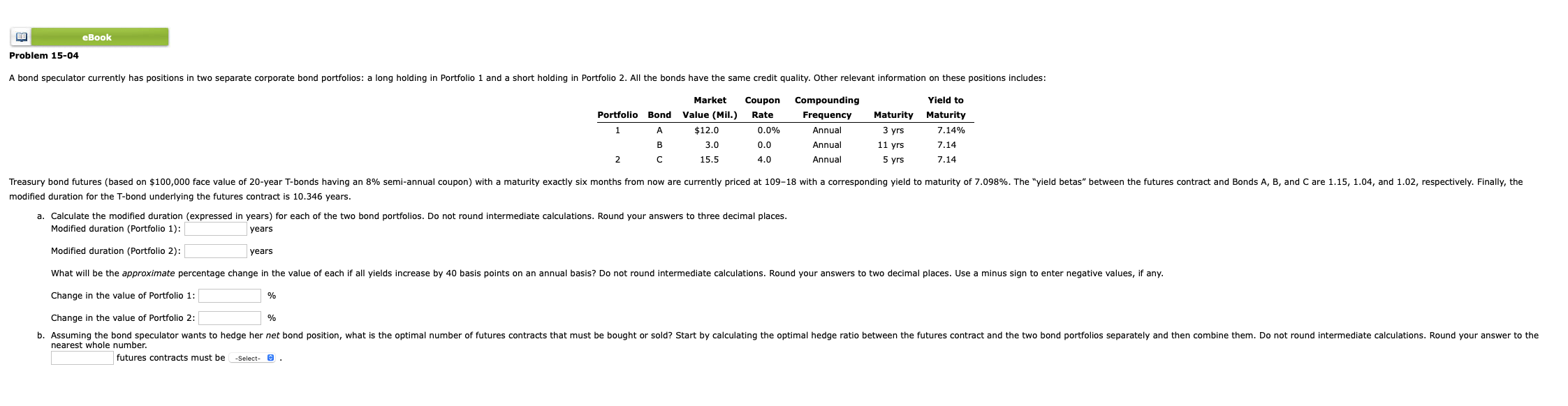

Question: Drop Down : Bought Or Sold odified duration for the T-bond underlying the futures contract is 10.346 years. a. Calculate the modified duration (ovnroccon in

Drop Down : Bought Or Sold

odified duration for the T-bond underlying the futures contract is 10.346 years. a. Calculate the modified duration (ovnroccon in years) for each of the two bond portfolios. Do not round intermediate calculations. Round your answers to three decimal places. Modified duration (Portfolio 1): Modified duration (Portfolio 2): /ears Change in the value of Portfolio 1: Change in the value of Portfolio 2: arest whole number. futures contracts must be - Select- . odified duration for the T-bond underlying the futures contract is 10.346 years. a. Calculate the modified duration (ovnroccon in years) for each of the two bond portfolios. Do not round intermediate calculations. Round your answers to three decimal places. Modified duration (Portfolio 1): Modified duration (Portfolio 2): /ears Change in the value of Portfolio 1: Change in the value of Portfolio 2: arest whole number. futures contracts must be - Select-

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts