Question: Drop-down option one: Front end,back-end Drop down option two: monthly, annual Drop-down option three: before tax, after tax Drop-down option four: Front end,back-end Drop-down option

Drop-down option one: Front end,back-end

Drop down option two: monthly, annual

Drop-down option three: before tax, after tax

Drop-down option four: Front end,back-end

Drop-down option five: annual, monthly

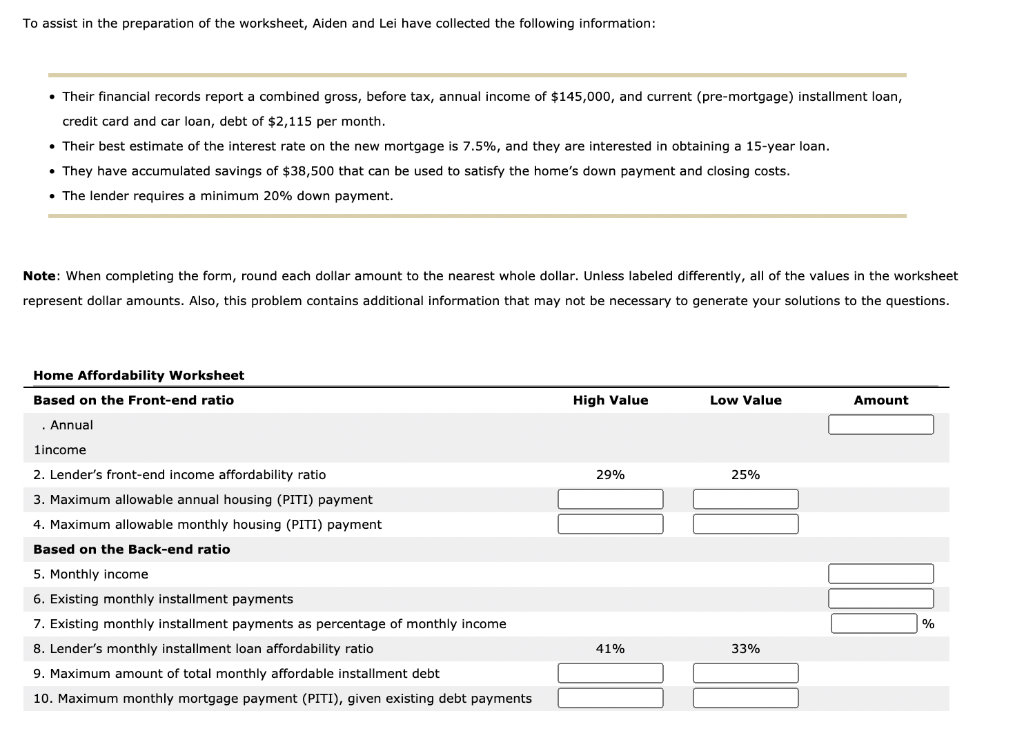

Prior to making a mortgage loan, lenders will require a potential borrower to qualify and demonstrate an acceptable credit record and sufficient income to support the loan's scheduled payments. This credit evaluation relies on two basic criteria to determine maximum payment amount, and, relatedly, the maximum total loan and house amount that the borrower can afford. Generally, the guidelines specify a range for each criterion. This practice provides each lender with the flexibility to adapt its requirements to a particular loan applicant. The two borrowing criteria used by most lending institutions are as follows: The , or maximum allowable housing expense ratio, which maintains that the applicant's total expenditures for housing (as measured by a year's worth of PITI payments), cannot exceed 25%-29% of the borrower's annual gross, or income. The ,or maximum allowable monthly housing expense and long-term debt ratio, which maintains that the total of all debt payments-including the PITI mortgage payments, auto loans, and all other debt payments-cannot exceed 33-41% of applicant's monthly gross income. Next week, your friends Aiden and Lei want to apply to the Fourth Global Bank for a mortgage loan. They are considering the purchase of a home that is expected to cost $155,000. To prevent their possible embarrassment at the bank, and given your knowledge of personal finance, they've asked you to help answer the following questions by completing the home affordability worksheet that follows: What is the minimum and maximum annual housing expense allowable by the bank, given Aiden and Lei's combined annual income? What is the minimum and maximum total monthly debt obligation allowable by the bank, given Aiden and Lei's combined monthly income? Given their existing debt obligations, what is the maximum additional mortgage obligation that Aiden and Lei can reasonably expect the bank to consider next week? To assist in the preparation of the worksheet, Aiden and Lei have collected the following information: Their financial records report a combined gross, before tax, annual income of $145,000, and current (pre-mortgage) installment loan, credit card and car loan, debt of $2,115 per month. Their best estimate of the interest rate on the new mortgage is 7.5%, and they are interested in obtaining a 15-year loan. They have accumulated savings of $38,500 that can be used to satisfy the home's down payment and closing costs. The lender requires a minimum 20% down payment. Note: When completing the form, round each dollar amount to the nearest whole dollar. Unless labeled differently, all of the values in the worksheet represent dollar amounts. Also, this problem contains additional information that may not be necessary to generate your solutions to the questions. Home Affordability Worksheet Based on the Front-end ratio High Value Low Value Amount . Annual 1income 29% 25% 2. Lender's front-end income affordability ratio 3. Maximum allowable annual housing (PITI) payment 4. Maximum allowable monthly housing (PITI) payment Based on the Back-end ratio 5. Monthly income 6. Existing monthly installment payments % 41% 33% 7. Existing monthly installment payments as percentage of monthly income 8. Lender's monthly installment loan affordability ratio 9. Maximum amount of total monthly affordable installment debt 10. Maximum monthly mortgage payment (PITI), given existing debt payments Prior to making a mortgage loan, lenders will require a potential borrower to qualify and demonstrate an acceptable credit record and sufficient income to support the loan's scheduled payments. This credit evaluation relies on two basic criteria to determine maximum payment amount, and, relatedly, the maximum total loan and house amount that the borrower can afford. Generally, the guidelines specify a range for each criterion. This practice provides each lender with the flexibility to adapt its requirements to a particular loan applicant. The two borrowing criteria used by most lending institutions are as follows: The , or maximum allowable housing expense ratio, which maintains that the applicant's total expenditures for housing (as measured by a year's worth of PITI payments), cannot exceed 25%-29% of the borrower's annual gross, or income. The ,or maximum allowable monthly housing expense and long-term debt ratio, which maintains that the total of all debt payments-including the PITI mortgage payments, auto loans, and all other debt payments-cannot exceed 33-41% of applicant's monthly gross income. Next week, your friends Aiden and Lei want to apply to the Fourth Global Bank for a mortgage loan. They are considering the purchase of a home that is expected to cost $155,000. To prevent their possible embarrassment at the bank, and given your knowledge of personal finance, they've asked you to help answer the following questions by completing the home affordability worksheet that follows: What is the minimum and maximum annual housing expense allowable by the bank, given Aiden and Lei's combined annual income? What is the minimum and maximum total monthly debt obligation allowable by the bank, given Aiden and Lei's combined monthly income? Given their existing debt obligations, what is the maximum additional mortgage obligation that Aiden and Lei can reasonably expect the bank to consider next week? To assist in the preparation of the worksheet, Aiden and Lei have collected the following information: Their financial records report a combined gross, before tax, annual income of $145,000, and current (pre-mortgage) installment loan, credit card and car loan, debt of $2,115 per month. Their best estimate of the interest rate on the new mortgage is 7.5%, and they are interested in obtaining a 15-year loan. They have accumulated savings of $38,500 that can be used to satisfy the home's down payment and closing costs. The lender requires a minimum 20% down payment. Note: When completing the form, round each dollar amount to the nearest whole dollar. Unless labeled differently, all of the values in the worksheet represent dollar amounts. Also, this problem contains additional information that may not be necessary to generate your solutions to the questions. Home Affordability Worksheet Based on the Front-end ratio High Value Low Value Amount . Annual 1income 29% 25% 2. Lender's front-end income affordability ratio 3. Maximum allowable annual housing (PITI) payment 4. Maximum allowable monthly housing (PITI) payment Based on the Back-end ratio 5. Monthly income 6. Existing monthly installment payments % 41% 33% 7. Existing monthly installment payments as percentage of monthly income 8. Lender's monthly installment loan affordability ratio 9. Maximum amount of total monthly affordable installment debt 10. Maximum monthly mortgage payment (PITI), given existing debt payments

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts