Question: Drop-down options include Depreciation (SL Basis) Labor Overhead Raw materials Add: Income Tax Less: Income Tax Add: Noncash Charges Less: Noncash Charges This exercise parallels

Drop-down options include

- Depreciation (SL Basis)

- Labor

- Overhead

- Raw materials

- Add: Income Tax

- Less: Income Tax

- Add: Noncash Charges

- Less: Noncash Charges

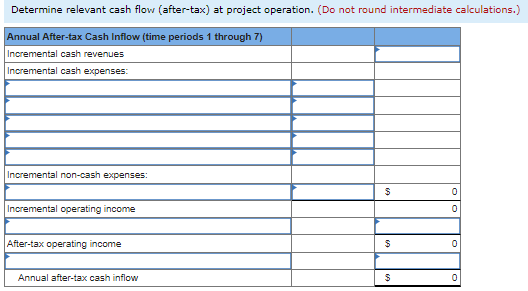

This exercise parallels the machine-purchase decision for the Mendoza Company that is discussed in the body of the chapter. Assume that Mendoza is exploring whether to enter a complementary line of business. The existing business line generates annual cash revenues of approximately $5,000,000 and cash expenses of $3,600,000, one-third of which are labor costs. The current level of investment in this existing division is $12,000,000. (Sales and costs of this division are not affected by the investment decision regarding the complementary line.) Mendoza estimates that incremental (noncash) net working capital of $30,000 will be needed to support the new business line. No additional facilities-level costs would be needed to support the new line-there is currently sufficient excess capacity. However, the new line would require additional cash expenses (overhead costs) of $400,000 per year. Raw materials costs associated with the new line are expected to be $1,200,000 per year, while the total labor cost is expected to double. The CFO of the company estimates that new machinery costing $2,500,000 would need to be purchased. This machinery has a seven-year useful life and an estimated salvage (terminal) value of $400,000. For tax purposes, assume that the Mendoza Company would use the straight-line method (with estimated salvage value considered in the calculation). Assume, further, that the weighted-average cost of capital (WACC) for Mendoza is 14% (after-tax) and that the combined (federal and state) income tax rate is 40%. Finally, assume that the new business line is expected to generate annual cash revenue of $3,600,000. Determine relevant cash flow (after-tax) at project initiation. Determine relevant cash flow (after-tax) at project operation. (Do not round intermediate calculations.) Determine relevant cash flow (after-tax) at project disposal (termination)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts