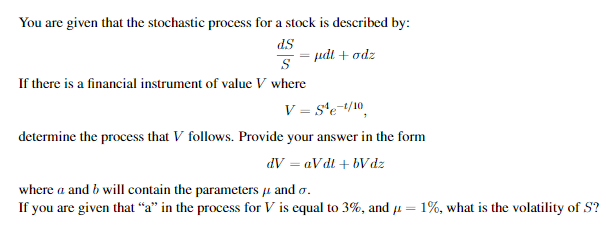

Question: ds You are given that the stochastic process for a stock is described by: S judl+odz If there is a financial instrument of value V

ds You are given that the stochastic process for a stock is described by: S judl+odz If there is a financial instrument of value V where V = Ste-t/10 determine the process that V follows. Provide your answer in the form LV = a V dl + Wdz where a and b will contain the parameters and o. If you are given that a in the process for V is equal to 3%, and = 1%, what is the volatility of S? ds You are given that the stochastic process for a stock is described by: S judl+odz If there is a financial instrument of value V where V = Ste-t/10 determine the process that V follows. Provide your answer in the form LV = a V dl + Wdz where a and b will contain the parameters and o. If you are given that a in the process for V is equal to 3%, and = 1%, what is the volatility of S

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts