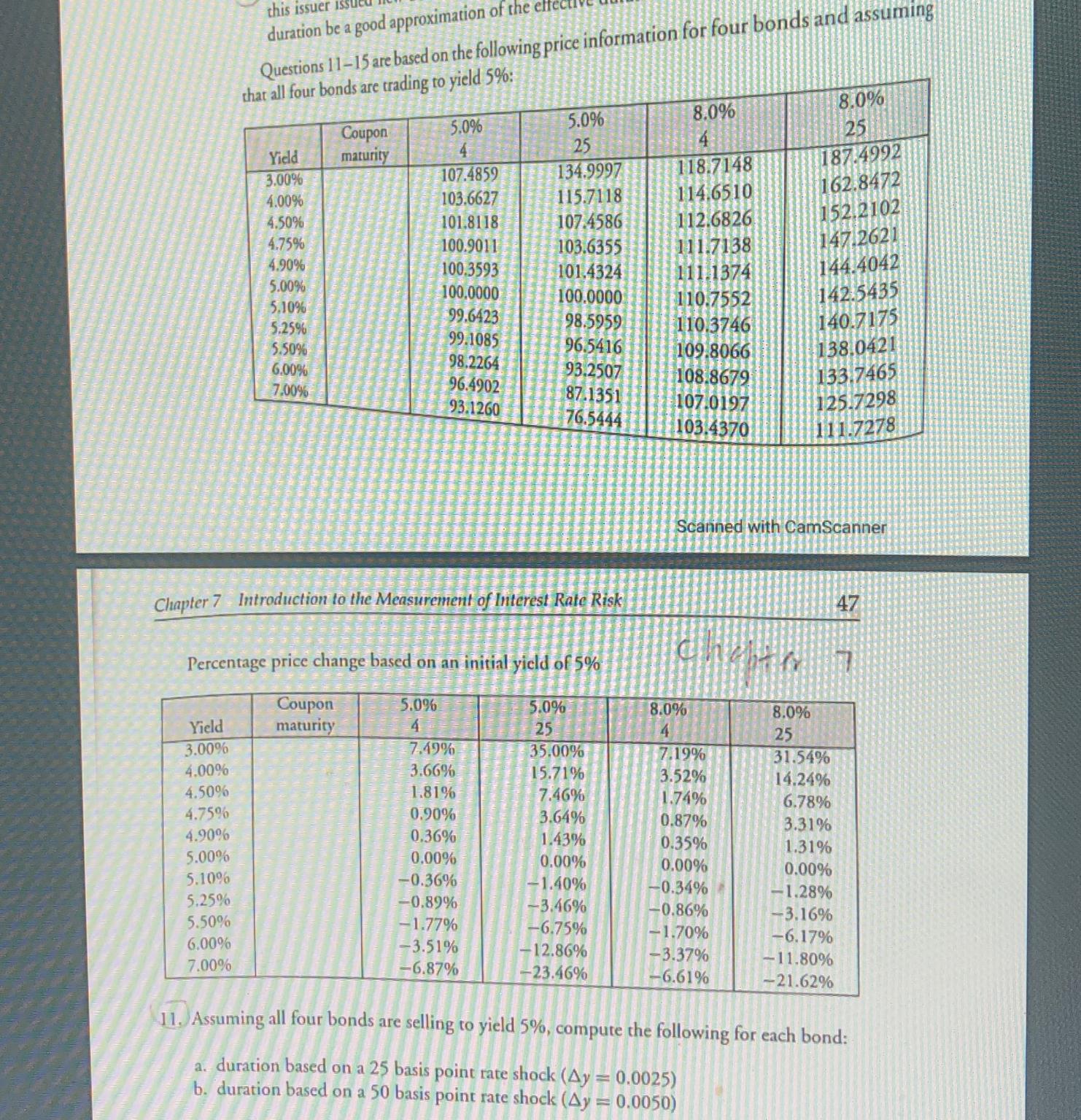

Question: duration be a good approximation of the e Questions 11-15 are based on the following price information for four bonds and assuming that all

duration be a good approximation of the

e\ Questions 11-15 are based on the following price information for four bonds and assuming that all four bonds are trading to yield

5%:\ Scanned with Camscanner\ Chapter 7 Introduction to the Measurement of Interest Rate Risk\ 47\ Percentage price change based on an initial yicld of

5%\ \\\\table[[Yield,\\\\table[[Coupon],[maturity]],\\\\table[[

5.0%

rice information for four bonds and assuming Questions 11-15 are based on the following price in Scanned with CamScanner Chapter 7 Introduction to the Measurement of Interest Rale Risk 47 Percentage price change based on an initial yicld of 5% 11. Assuming all four bonds are selling to yield 5%, compute the following for each bond: a. duration based on a 25 basis point rate shock (y=0.0025) b. duration based on a 50 basis point rate shock (y=0.0050)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts