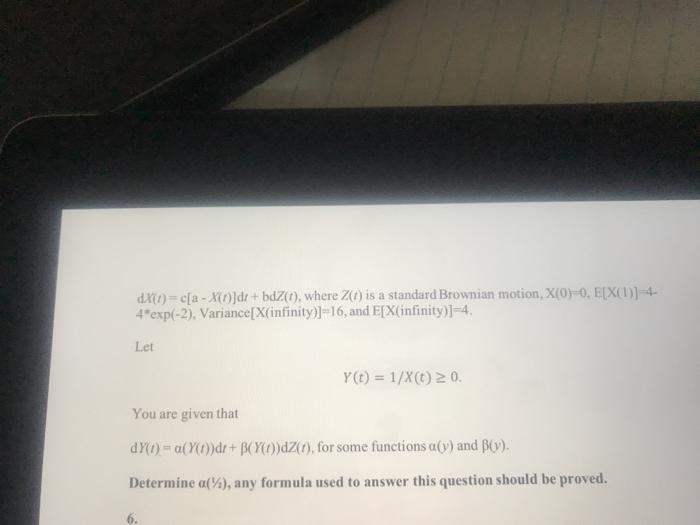

Question: dXD) - C[a - XO}dr + bdzo, where Z() is a standard Brownian motion, X(0)-0. E[X(1)]-4- 4*exp(-2), Variance[X(infinity)]-16, and E[X(infinity)]=4. Let Y(t) = 1/X(t) 20.

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock