Question: (e) Given the below information, calculate the covariance matrix V where V = DCD and Dis a diagonal matrix of standard deviations and Cis a

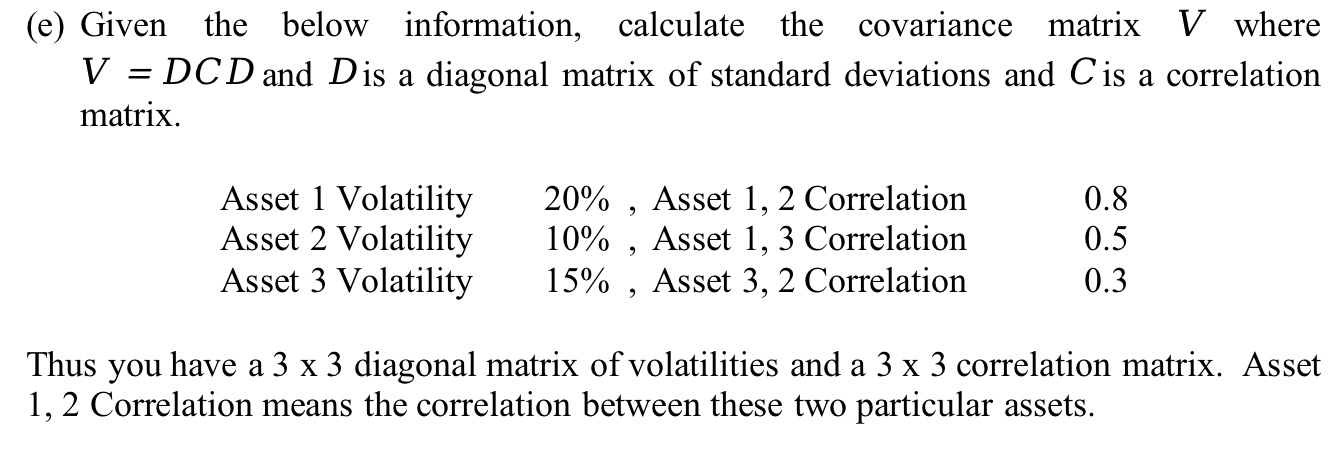

(e) Given the below information, calculate the covariance matrix V where V = DCD and Dis a diagonal matrix of standard deviations and Cis a correlation matrix. Asset 1 Volatility 20% , Asset 1, 2 Correlation 0.8 Asset 2 Volatility 10% , Asset 1, 3 Correlation 0.5 Asset 3 Volatility 15% , Asset 3, 2 Correlation 0.3 Thus you have a 3 x 3 diagonal matrix of volatilities and a 3 x 3 correlation matrix. Asset 1, 2 Correlation means the correlation between these two particular assets

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock