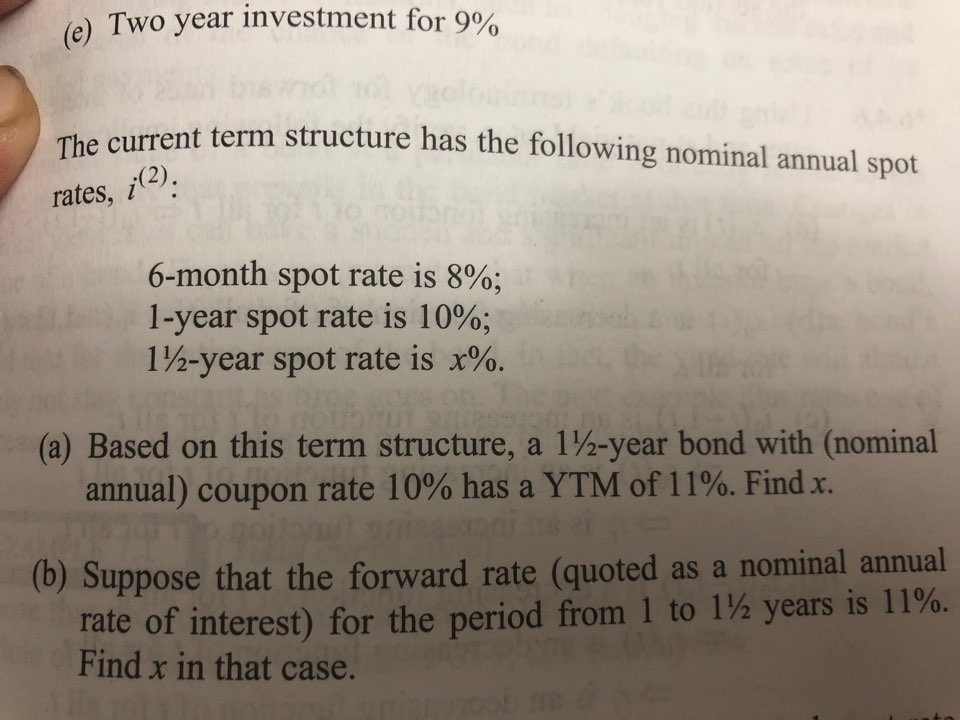

Question: (e) Two year investment for 9% current term structure has the following nominal annual spot rates, : 6-month spot rate is 8%; 1-year spot rate

(e) Two year investment for 9% current term structure has the following nominal annual spot rates, : 6-month spot rate is 8%; 1-year spot rate is 10%; 1 -year spot rate is x%. (a) Based on this term structure, a 1%-year bond with (nominal annual) coupon rate 10% has a YTM of 11%. Find x. b) Suppose that the forward rate (quoted as a nominal annual rate of interest) for the period from 1 to 1 years is 11%. Find x in that case

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock