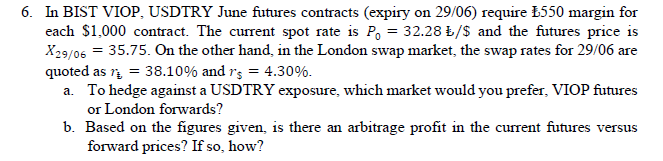

Question: each $ 1 , 0 0 0 contract. The current spot rate is P 0 = 3 2 . 2 8 E $ and the

each $ contract. The current spot rate is and the futures price is On the other hand, in the London swap market, the swap rates for are quoted as and

a To hedge against a USDTRY exposure, which market would you prefer, VIOP futures or London forwards?

b Based on the figures given, is there an arbitrage profit in the current futures versus forward prices? If so how?

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock