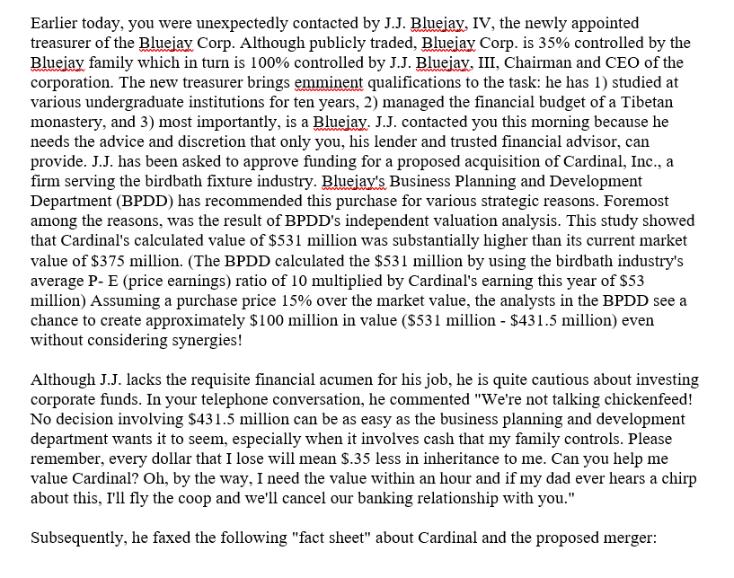

Earlier today, you were unexpectedly contacted by J.J. Bluejay, IV, the newly appointed treasurer of the...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

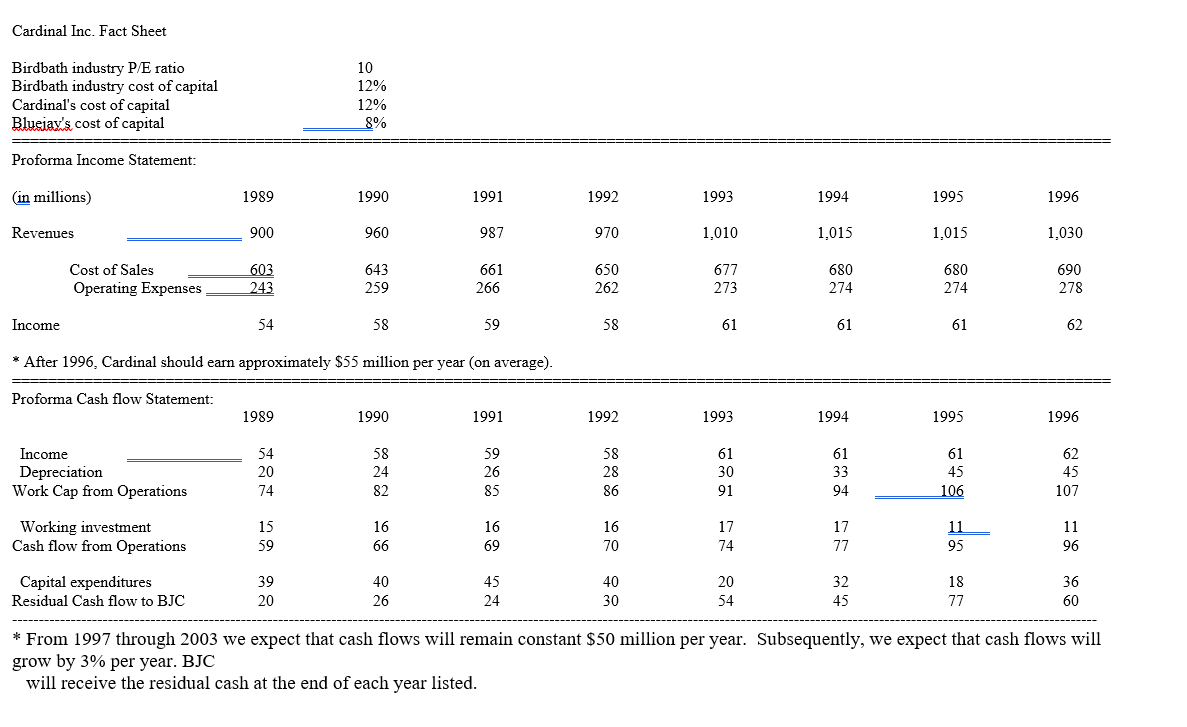

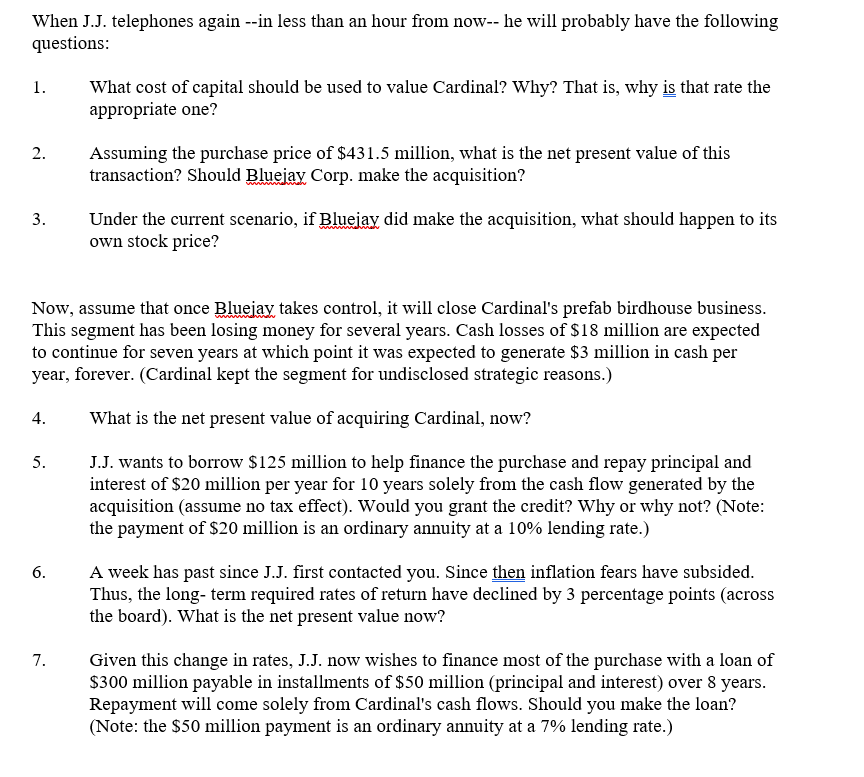

Earlier today, you were unexpectedly contacted by J.J. Bluejay, IV, the newly appointed treasurer of the Bluejay Corp. Although publicly traded, Bluejay Corp. is 35% controlled by the Bluejay family which in turn is 100% controlled by J.J. Bluejay, III, Chairman and CEO of the corporation. The new treasurer brings emminent qualifications to the task: he has 1) studied at various undergraduate institutions for ten years, 2) managed the financial budget of a Tibetan monastery, and 3) most importantly, is a Bluejay. J.J. contacted you this morning because he needs the advice and discretion that only you, his lender and trusted financial advisor, can provide. J.J. has been asked to approve funding for a proposed acquisition of Cardinal, Inc., a firm serving the birdbath fixture industry. Bluejay's Business Planning and Development Department (BPDD) has recommended this purchase for various strategic reasons. Foremost among the reasons, was the result of BPDD's independent valuation analysis. This study showed that Cardinal's calculated value of $531 million was substantially higher than its current market value of $375 million. (The BPDD calculated the $531 million by using the birdbath industry's average P-E (price earnings) ratio of 10 multiplied by Cardinal's earning this year of $53 million) Assuming a purchase price 15% over the market value, the analysts in the BPDD see a chance to create approximately $100 million in value ($531 million - $431.5 million) even without considering synergies! Although J.J. lacks the requisite financial acumen for his job, he is quite cautious about investing corporate funds. In your telephone conversation, he commented "We're not talking chickenfeed! No decision involving $431.5 million can be as easy as the business planning and development department wants it to seem, especially when it involves cash that my family controls. Please remember, every dollar that I lose will mean $.35 less in inheritance to me. Can you help me value Cardinal? Oh, by the way, I need the value within an hour and if my dad ever hears a chirp about this, I'll fly the coop and we'll cancel our banking relationship with you." Subsequently, he faxed the following "fact sheet" about Cardinal and the proposed merger: Cardinal Inc. Fact Sheet Birdbath industry P/E ratio 10 Birdbath industry cost of capital 12% Cardinal's cost of capital 12% 8% Bluejay's cost of capital Proforma Income Statement: (in millions) 1989 1990 1991 1992 1993 1994 1995 1996 Revenues 900 960 987 970 1,010 1,015 1,015 1,030 Cost of Sales 603 643 661 650 677 680 680 Operating Expenses, 243 259 266 262 273 274 274 690 278 Income 54 58 59 58 61 61 61 62 *After 1996, Cardinal should earn approximately $55 million per year (on average). Proforma Cash flow Statement: 1989 1990 1991 1992 1993 1994 Income 54 58 59 58 61 Depreciation Work Cap from Operations Working investment Cash flow from Operations Capital expenditures Residual Cash flow to BJC 228 22 20 24 26 28 74 82 85 86 15 16 16 16 59 66 69 70 39 20 40 26 45 24 40 30 852 28 30 91 17 17 74 77 257 1995 1996 61 62 45 45 106 107 11 11 95 96 20 32 54 45 25 18 36 77 60 * From 1997 through 2003 we expect that cash flows will remain constant $50 million per year. Subsequently, we expect that cash flows will grow by 3% per year. BJC will receive the residual cash at the end of each year listed. When J.J. telephones again --in less than an hour from now-- he will probably have the following questions: 1. What cost of capital should be used to value Cardinal? Why? That is, why is that rate the appropriate one? 2. Assuming the purchase price of $431.5 million, what is the net present value of this transaction? Should Bluejay Corp. make the acquisition? 3. Under the current scenario, if Bluejay did make the acquisition, what should happen to its own stock price? Now, assume that once Bluejay takes control, it will close Cardinal's prefab birdhouse business. This segment has been losing money for several years. Cash losses of $18 million are expected to continue for seven years at which point it was expected to generate $3 million in cash per year, forever. (Cardinal kept the segment for undisclosed strategic reasons.) 4. What is the net present value of acquiring Cardinal, now? 5. 6. 7. J.J. wants to borrow $125 million to help finance the purchase and repay principal and interest of $20 million per year for 10 years solely from the cash flow generated by the acquisition (assume no tax effect). Would you grant the credit? Why or why not? (Note: the payment of $20 million is an ordinary annuity at a 10% lending rate.) A week has past since J.J. first contacted you. Since then inflation fears have subsided. Thus, the long-term required rates of return have declined by 3 percentage points (across the board). What is the net present value now? Given this change in rates, J.J. now wishes to finance most of the purchase with a loan of $300 million payable in installments of $50 million (principal and interest) over 8 years. Repayment will come solely from Cardinal's cash flows. Should you make the loan? (Note: the $50 million payment is an ordinary annuity at a 7% lending rate.) Earlier today, you were unexpectedly contacted by J.J. Bluejay, IV, the newly appointed treasurer of the Bluejay Corp. Although publicly traded, Bluejay Corp. is 35% controlled by the Bluejay family which in turn is 100% controlled by J.J. Bluejay, III, Chairman and CEO of the corporation. The new treasurer brings emminent qualifications to the task: he has 1) studied at various undergraduate institutions for ten years, 2) managed the financial budget of a Tibetan monastery, and 3) most importantly, is a Bluejay. J.J. contacted you this morning because he needs the advice and discretion that only you, his lender and trusted financial advisor, can provide. J.J. has been asked to approve funding for a proposed acquisition of Cardinal, Inc., a firm serving the birdbath fixture industry. Bluejay's Business Planning and Development Department (BPDD) has recommended this purchase for various strategic reasons. Foremost among the reasons, was the result of BPDD's independent valuation analysis. This study showed that Cardinal's calculated value of $531 million was substantially higher than its current market value of $375 million. (The BPDD calculated the $531 million by using the birdbath industry's average P-E (price earnings) ratio of 10 multiplied by Cardinal's earning this year of $53 million) Assuming a purchase price 15% over the market value, the analysts in the BPDD see a chance to create approximately $100 million in value ($531 million - $431.5 million) even without considering synergies! Although J.J. lacks the requisite financial acumen for his job, he is quite cautious about investing corporate funds. In your telephone conversation, he commented "We're not talking chickenfeed! No decision involving $431.5 million can be as easy as the business planning and development department wants it to seem, especially when it involves cash that my family controls. Please remember, every dollar that I lose will mean $.35 less in inheritance to me. Can you help me value Cardinal? Oh, by the way, I need the value within an hour and if my dad ever hears a chirp about this, I'll fly the coop and we'll cancel our banking relationship with you." Subsequently, he faxed the following "fact sheet" about Cardinal and the proposed merger: Cardinal Inc. Fact Sheet Birdbath industry P/E ratio 10 Birdbath industry cost of capital 12% Cardinal's cost of capital 12% 8% Bluejay's cost of capital Proforma Income Statement: (in millions) 1989 1990 1991 1992 1993 1994 1995 1996 Revenues 900 960 987 970 1,010 1,015 1,015 1,030 Cost of Sales 603 643 661 650 677 680 680 Operating Expenses, 243 259 266 262 273 274 274 690 278 Income 54 58 59 58 61 61 61 62 *After 1996, Cardinal should earn approximately $55 million per year (on average). Proforma Cash flow Statement: 1989 1990 1991 1992 1993 1994 Income 54 58 59 58 61 Depreciation Work Cap from Operations Working investment Cash flow from Operations Capital expenditures Residual Cash flow to BJC 228 22 20 24 26 28 74 82 85 86 15 16 16 16 59 66 69 70 39 20 40 26 45 24 40 30 852 28 30 91 17 17 74 77 257 1995 1996 61 62 45 45 106 107 11 11 95 96 20 32 54 45 25 18 36 77 60 * From 1997 through 2003 we expect that cash flows will remain constant $50 million per year. Subsequently, we expect that cash flows will grow by 3% per year. BJC will receive the residual cash at the end of each year listed. When J.J. telephones again --in less than an hour from now-- he will probably have the following questions: 1. What cost of capital should be used to value Cardinal? Why? That is, why is that rate the appropriate one? 2. Assuming the purchase price of $431.5 million, what is the net present value of this transaction? Should Bluejay Corp. make the acquisition? 3. Under the current scenario, if Bluejay did make the acquisition, what should happen to its own stock price? Now, assume that once Bluejay takes control, it will close Cardinal's prefab birdhouse business. This segment has been losing money for several years. Cash losses of $18 million are expected to continue for seven years at which point it was expected to generate $3 million in cash per year, forever. (Cardinal kept the segment for undisclosed strategic reasons.) 4. What is the net present value of acquiring Cardinal, now? 5. 6. 7. J.J. wants to borrow $125 million to help finance the purchase and repay principal and interest of $20 million per year for 10 years solely from the cash flow generated by the acquisition (assume no tax effect). Would you grant the credit? Why or why not? (Note: the payment of $20 million is an ordinary annuity at a 10% lending rate.) A week has past since J.J. first contacted you. Since then inflation fears have subsided. Thus, the long-term required rates of return have declined by 3 percentage points (across the board). What is the net present value now? Given this change in rates, J.J. now wishes to finance most of the purchase with a loan of $300 million payable in installments of $50 million (principal and interest) over 8 years. Repayment will come solely from Cardinal's cash flows. Should you make the loan? (Note: the $50 million payment is an ordinary annuity at a 7% lending rate.)

Expert Answer:

Related Book For

Introduction To Corporate Finance

ISBN: 9781118300763

3rd Edition

Authors: Laurence Booth, Sean Cleary

Posted Date:

Students also viewed these finance questions

-

The Crazy Eddie fraud may appear smaller and gentler than the massive billion-dollar frauds exposed in recent times, such as Bernie Madoffs Ponzi scheme, frauds in the subprime mortgage market, the...

-

Managing Scope Changes Case Study Scope changes on a project can occur regardless of how well the project is planned or executed. Scope changes can be the result of something that was omitted during...

-

Measure each amount given in Problems 1721. a. Container C in ounces b. Container C in milliliters mL 500- 400- 300 200- 100 cups 2 1 -16-ez -14 oz -12 oz -110 oz 8 oz -16 oz -4 oz 2 oz Container C...

-

In each of the following, find the 6 Ã 6 matrix A = [aij] that satisfies the given condition: a. b. c. -10 15) 1 if i j s 1 0 al 10 otherwise

-

Steam steadily enters a nozzle at 180C and 1002.8 kPa with a velocity of 12 m/s and leaves at 300C and 8,000 kPa. For an inlet diameter of 0.5 and an outlet diameter of 0.2, determine the volume flow...

-

Why are grooming and attire so important in selling? How do you know if you are dressed appropriately for a customer?

-

Logan Company received from Furniture.com an invoice dated September 29. Terms were 1/10 EOM. List price on the invoice was $8,000 (freight not included). Logan receives a 8/7 chain discount. Freight...

-

Great Boots Company sells rock climbing equipment. On February 28, Great Boots had the following accounts and balances: Bonds payable $180,000 Discount on bonds payable 19,000 On that day, Great...

-

How does diversification and acquisition create value for a company and how can each destroy value for a company? explain

-

Using real-world examples, evaluate the effectiveness of foreign aid in promoting economic growth and economic development.

-

Using real-world examples, discuss the view that economic growth will always lead to economic development.

-

Using real-world examples, evaluate the arguments against protectionism.

-

Perform the operations by using the polar form and express the result in rectangular form. \(\frac{4+j}{(4+3 j)^{3}}\)

-

Using real-world examples, discuss the extent to which transfer payments can alleviate poverty.

-

Use the Internet to review at least two news articles or publications about current and future trends in the use of relational databases. Be prepared to discuss. "Systems Analysis Please respond to...

-

Estimate a range for the optimal objective value for the following LPs: (a) Minimize z = 5x1 + 2x2 Subject to X1 - x2 3 2x1 + 3x2 5 X1, x2 0 (b) Maximize z = x1 + 5x2 + 3x3 Subject to X1 + 2x2 +...

-

Draw a UML sequence diagram for an interrupt-driven write of a device. The diagram should include the background program, the handler, and the device.

-

Draw a UML sequence diagram of a lower-priority interrupt that happens during a higher-priority interrupt handler. The diagram should include the device, the two handlers, and the background program.

-

Draw a UML sequence diagram for copying characters from an input to an output device using interrupt-driven I/O. The diagram should include the two devices and the two I/O handlers.

Study smarter with the SolutionInn App