Question: eBook Problem 7-03 You are an analyst for a large public pension fund and you have been assigned the task of evaluating two different external

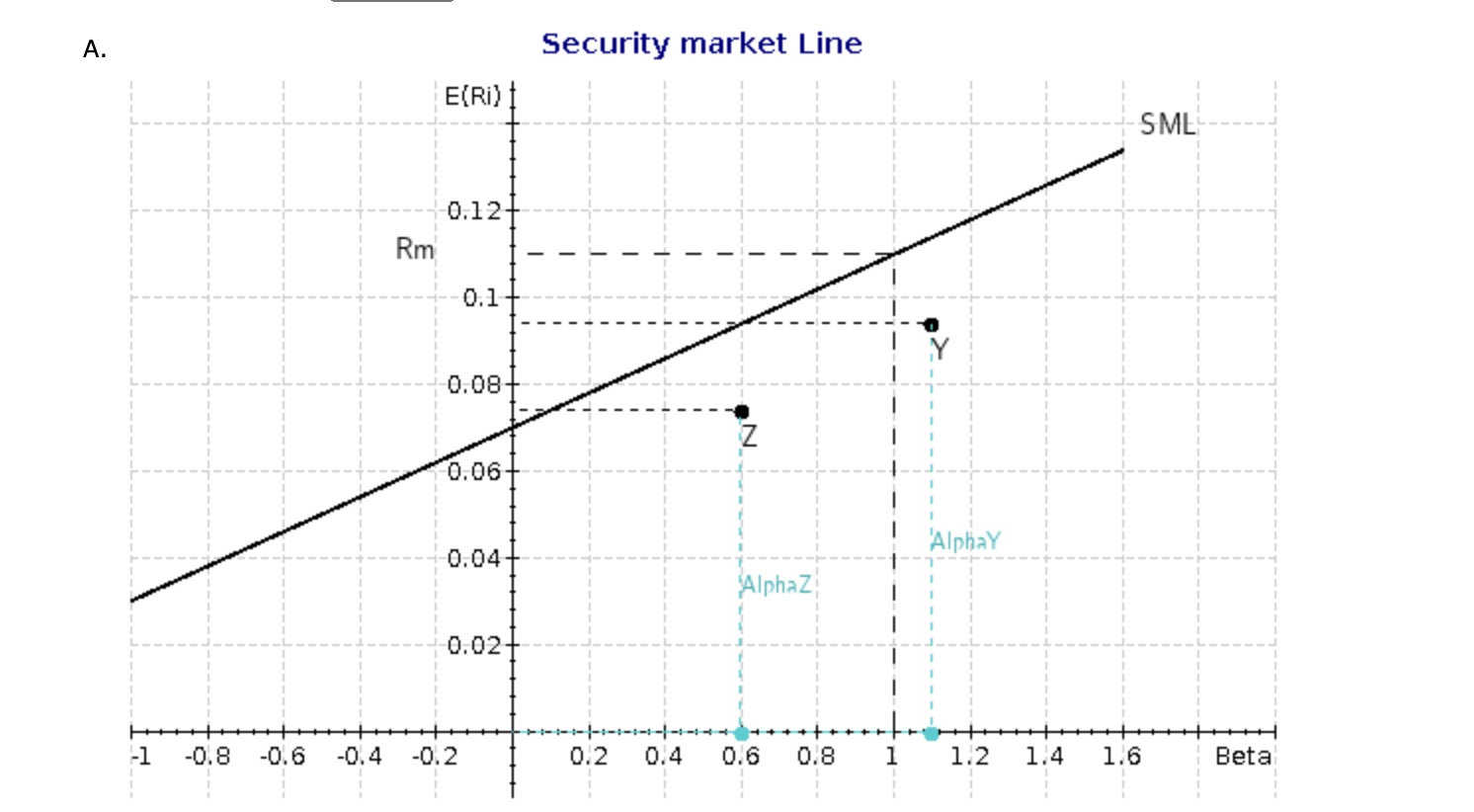

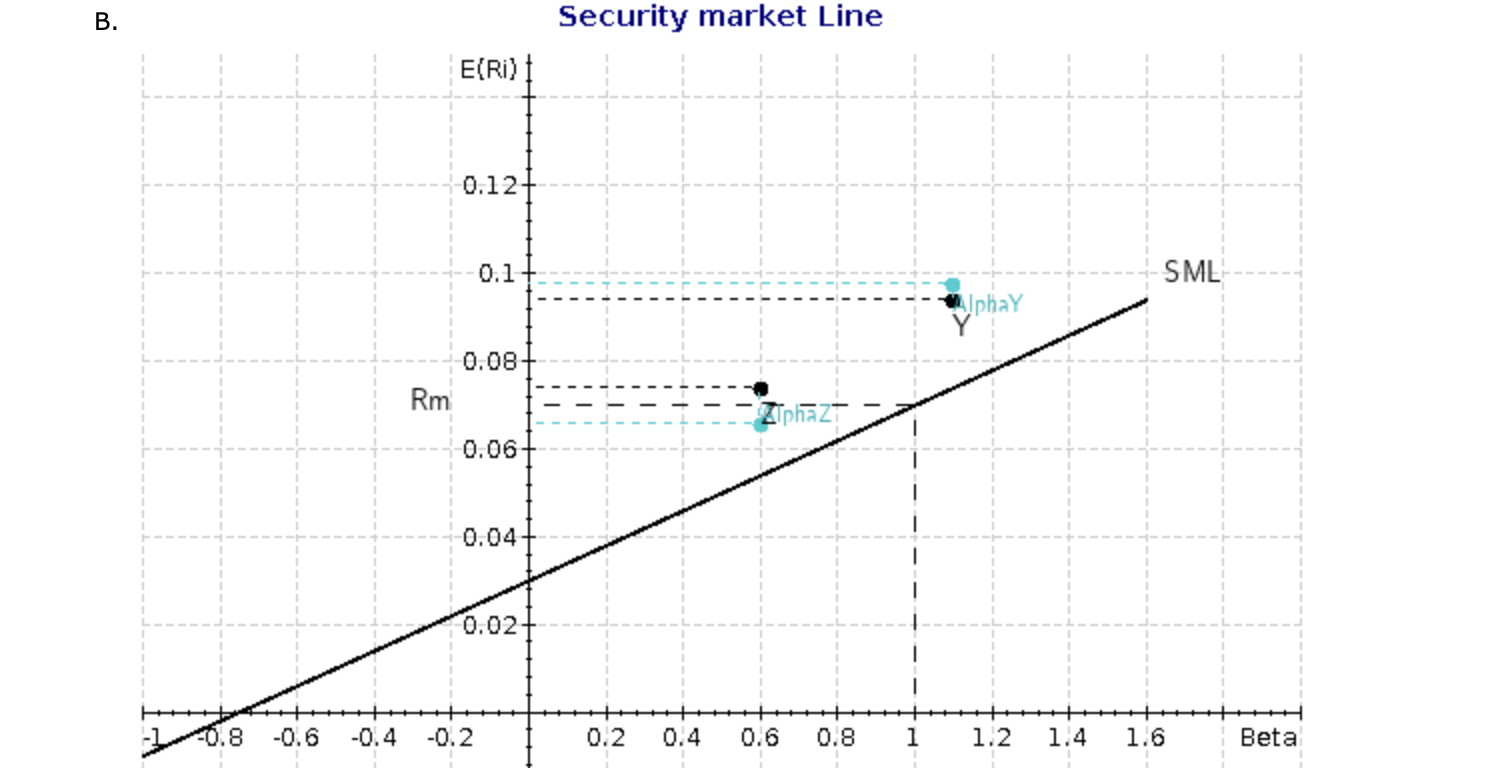

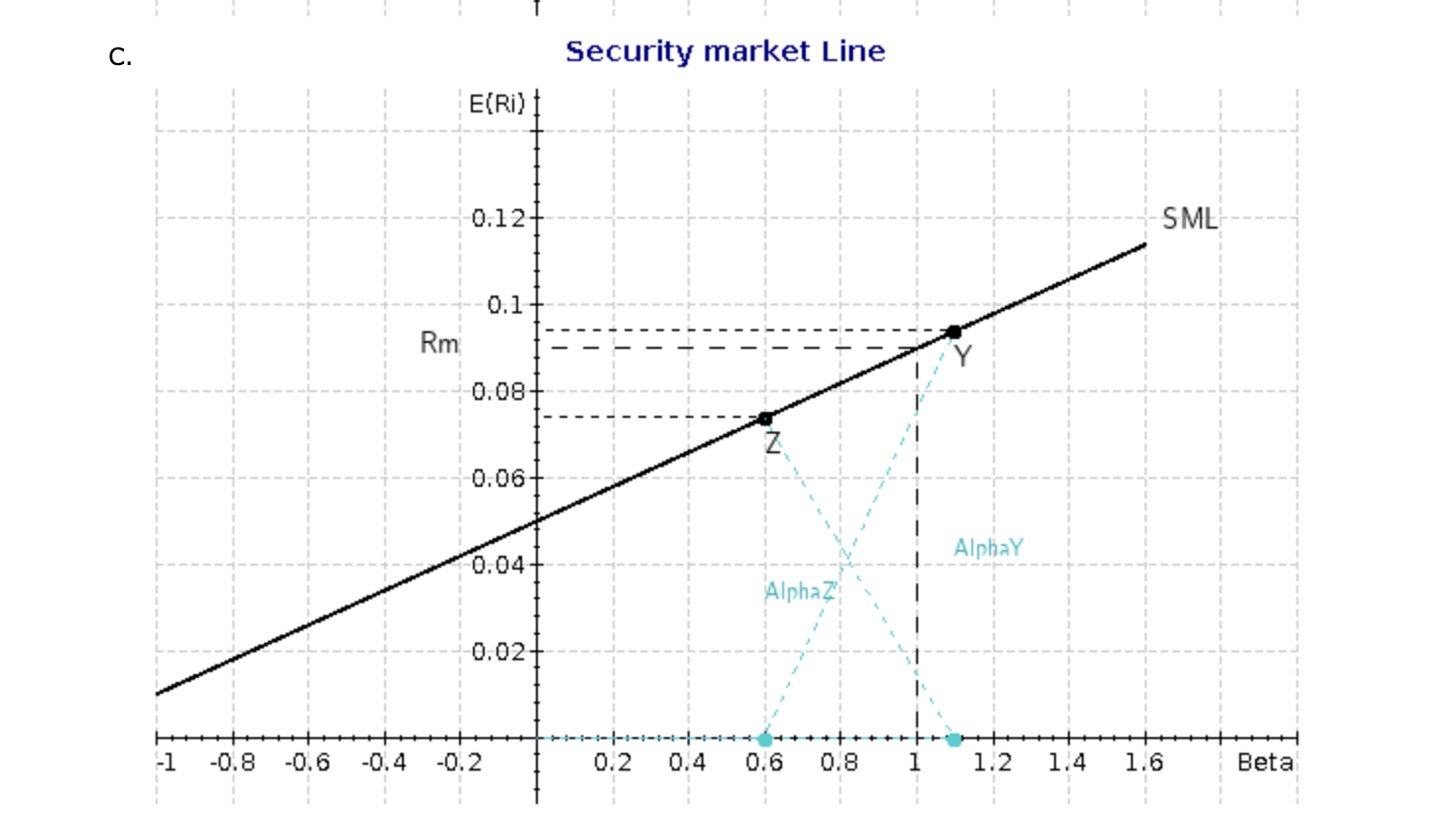

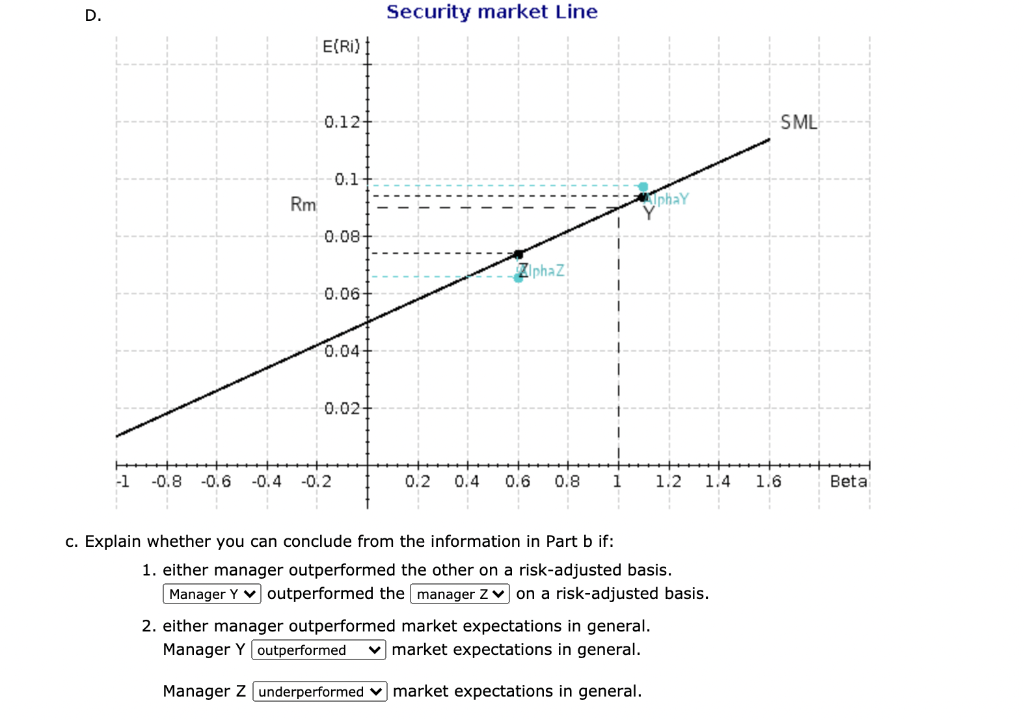

| eBook Problem 7-03 You are an analyst for a large public pension fund and you have been assigned the task of evaluating two different external portfolio managers (Y and Z). You consider the following historical average return, standard deviation, and CAPM beta estimates for these two managers over the past five years:

Additionally, your estimate for the risk premium for the market portfolio is 4.00 percent and the risk-free rate is currently 5.00 percent.

| ||||||||||||||||||

A. Security market Line E(RI) SML 0.12 Rm 0.1 Y 0.08 Z 0.06 Alphay 0.04 Alphaz 0.02 -1 -0.8 -0.6 -0.4 -0.2 0.2 0.4 0.6 0.8 1 1.2 1.4 1.6 Beta B. Security market Line E(Ri) 0.12 0.1 SME Alphay 0.08 Rm !! iphazi 0.06 0.04 0.02 -0.8 -0.6 -0.4 -0.2 0.2 0.4 0.6 0.8 1 1.2 1.4 1.6 Beta c. Security market Line E(Ri) 0.12 SME 0.1 Rm 0.08 Z 0.06 Alphay 0.04 Alpha 0.02 -1 -0.8 -0.6 -0.4 -0.2 0.2 0.4 0.6 0.8 1 1.2 1.4 1.6 Beta D. Security market Line E(R) 0.12 SML 0.1 Rm phay 0.08 Ziphaz 0.06 0.04 0.02 -1 -0.8 -0.6 -0.4 -0.2 0.2 0.4 0.6 0.8 1 1.2 1.4 1.6 Beta c. Explain whether you can conclude from the information in Part b if: 1. either manager outperformed the other on a risk-adjusted basis. Manager Y V outperformed the manager zv on a risk-adjusted basis. 2. either manager outperformed market expectations in general. Manager Y outperformed market expectations in general. Manager z underperformed market expectations in general

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts