Question: eBookeBook Problem 13-01 please show me how this was solved using excel. I don't understand the pv as % of price. Calculate the Macaulay duration

| eBookeBook Problem 13-01 please show me how this was solved using excel. I don't understand the pv as % of price. Calculate the Macaulay duration of a 9%, $1,000 par bond that matures in three years if the bond's YTM is 12% and interest is paid semiannually. Calculate this bond's modified duration. Do not round intermediate calculations. Round your answer to two decimal places.

|

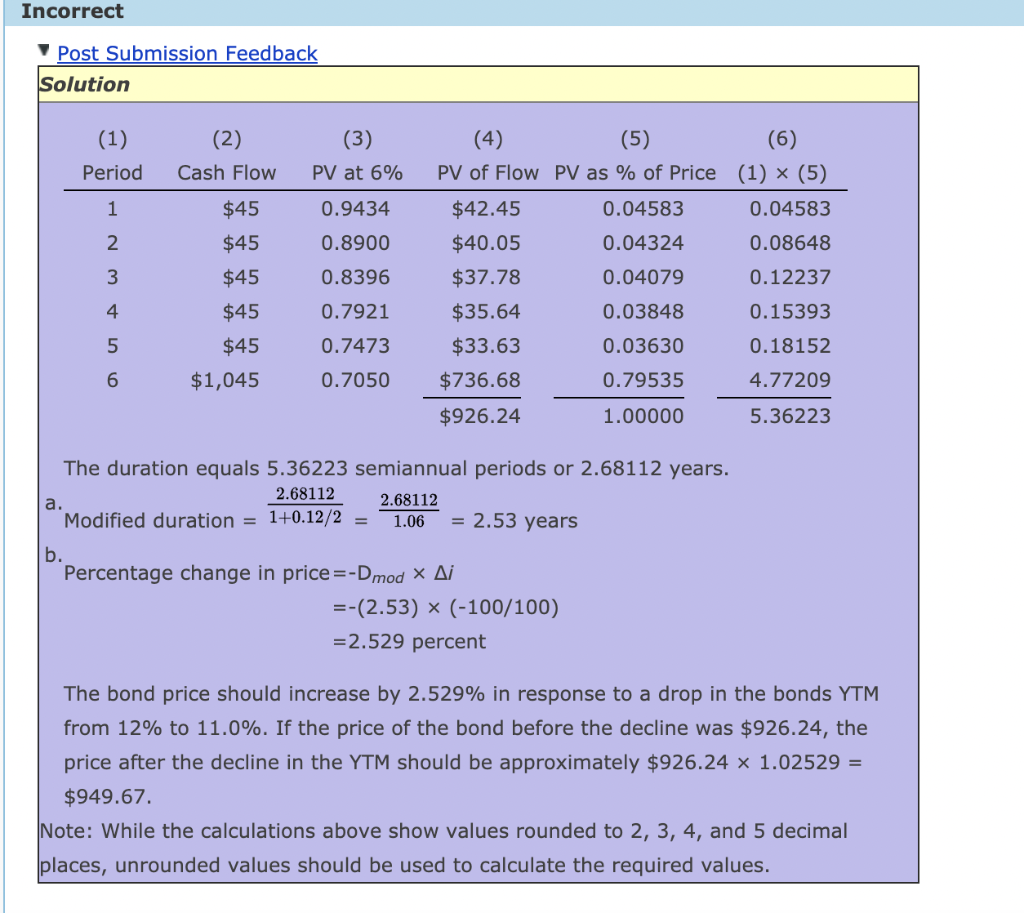

Incorrect Post Submission Feedback Solution (2) (1) Period (3) PV at 6% Cash Flow 1 $45 0.9434 0.8900 2 $45 3 0.8396 (4) (5) (6) PV of Flow PV as % of Price (1) x (5) $42.45 0.04583 0.04583 $40.05 0.04324 0.08648 $37.78 0.04079 0.12237 $35.64 0.03848 0.15393 $33.63 0.03630 0.18152 $736.68 0.79535 4.77209 $926.24 1.00000 5.36223 $45 $45 $45 4 0.7921 5 0.7473 6 $1,045 0.7050 The duration equals 5.36223 semiannual periods or 2.68112 years. 2.68112 2.68112 Modified duration = 1+0.12/2 = 1.06 = 2.53 years a. b. Percentage change in price =-Dmod X Ai =-(2.53) * (-100/100) =2.529 percent The bond price should increase by 2.529% in response to a drop in the bonds YTM from 12% to 11.0%. If the price of the bond before the decline was $926.24, the price after the decline in the YTM should be approximately $926.24 x 1.02529 = $949.67. Note: While the calculations above show values rounded to 2, 3, 4, and 5 decimal places, unrounded values should be used to calculate the required values

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts