Question: Economics question The table below shows the quantity (total product) and different costs for a seller in a perfectly competitive market. If the market price

Economics question

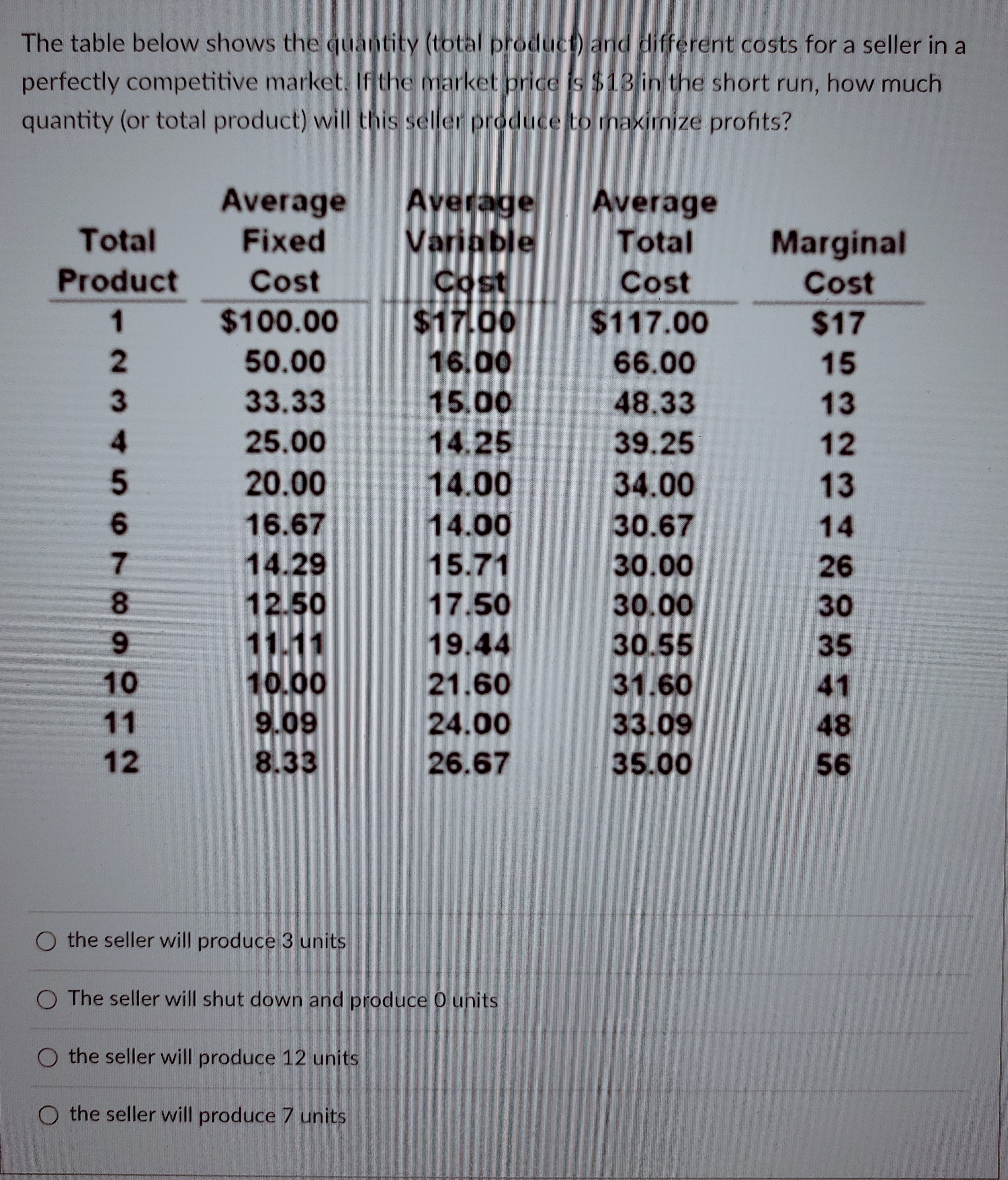

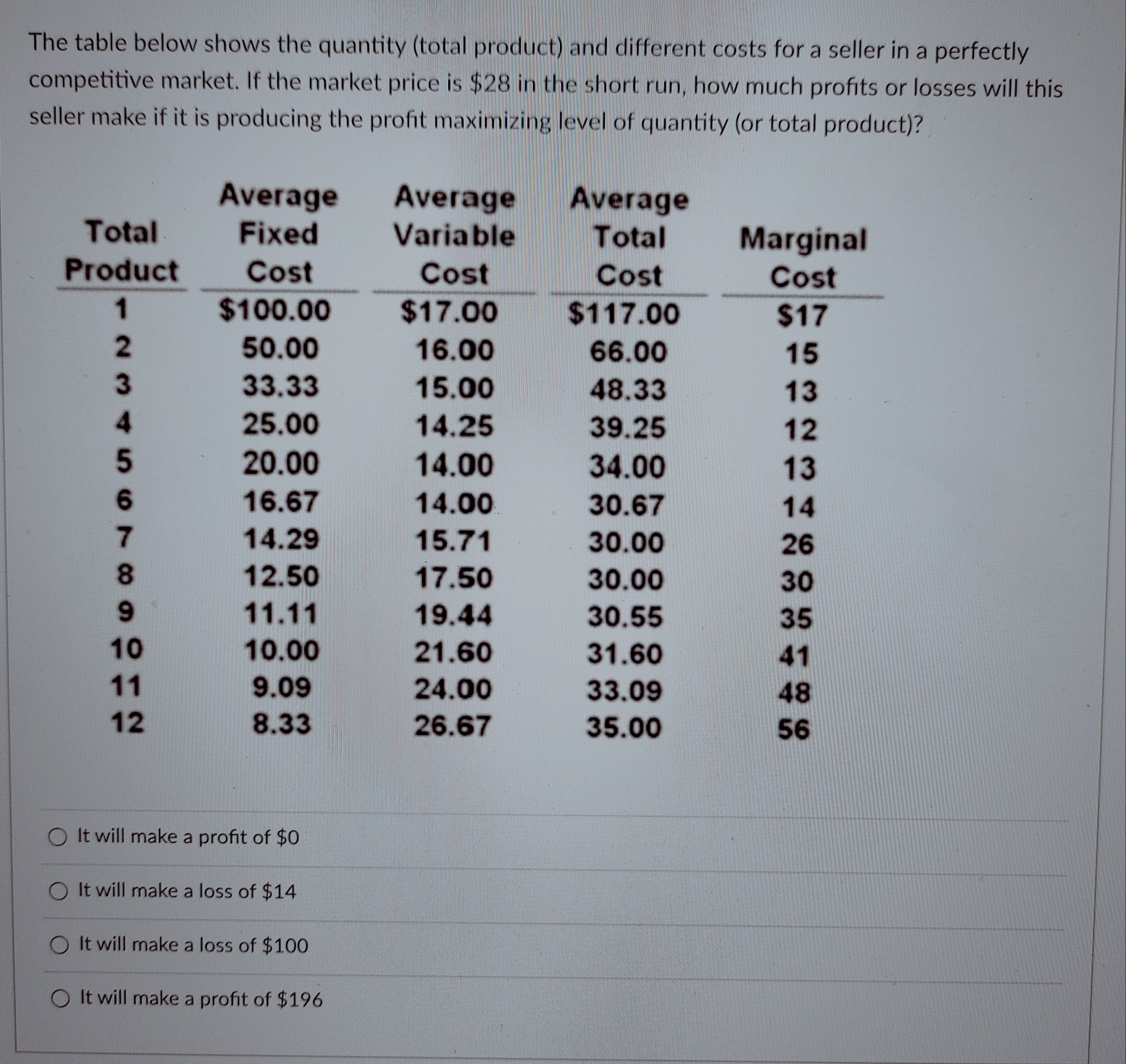

The table below shows the quantity (total product) and different costs for a seller in a perfectly competitive market. If the market price is $13 in the short run, how much quantity (or total product) will this seller produce to maximize profits? Average Average Average Total Fixed Variable Total Marginal Product Cost Cost Cost Cost $100.00 $17.00 $117.00 $17 W N - 50.00 16.00 66.00 15 33.33 15.00 48.33 13 25.00 14.25 39.25 12 20.00 14.00 34.00 13 16.67 14.00 30.67 14 14.29 15.71 30.00 26 54 00 - ) 12.50 17.50 30.00 30 11.11 19.44 30.55 35 10 10.00 21.60 31.60 41 11 9.09 24.00 33.09 48 12 8.33 26.67 35.00 56 the seller will produce 3 units The seller will shut down and produce 0 units the seller will produce 12 units the seller will produce 7 unitsThe table below shows the quantity (total product) and different costs for a seller in a perfectly competitive market. If the market price is $28 in the short run, how much profits or losses will this seller make if it is producing the profit maximizing level of quantity (or total product)? Average Average Average Total Fixed Variable Total Marginal Product Cost Cost Cost Cost $100.00 $17.00 $117.00 $17 50.00 W N - 16.00 66.00 15 33.33 15.00 48.33 13 25.00 14.25 39.25 12 20.00 14.00 34.00 13 16.67 14.00 30.67 14 14.29 15.71 30.00 26 12.50 17.50 30.00 30 11.11 19.44 30.55 35 10 10.00 21.60 31.60 41 11 9.09 24.00 33.09 48 12 8.33 26.67 35.00 56 It will make a profit of $0 It will make a loss of $14 It will make a loss of $100 It will make a profit of $196

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts