Question: EF 4321: Derivatives and Risk Management Problem Set 3 Fall, 2022 Instructions: The problem set should be completed in teams. Please upload an electronic copy

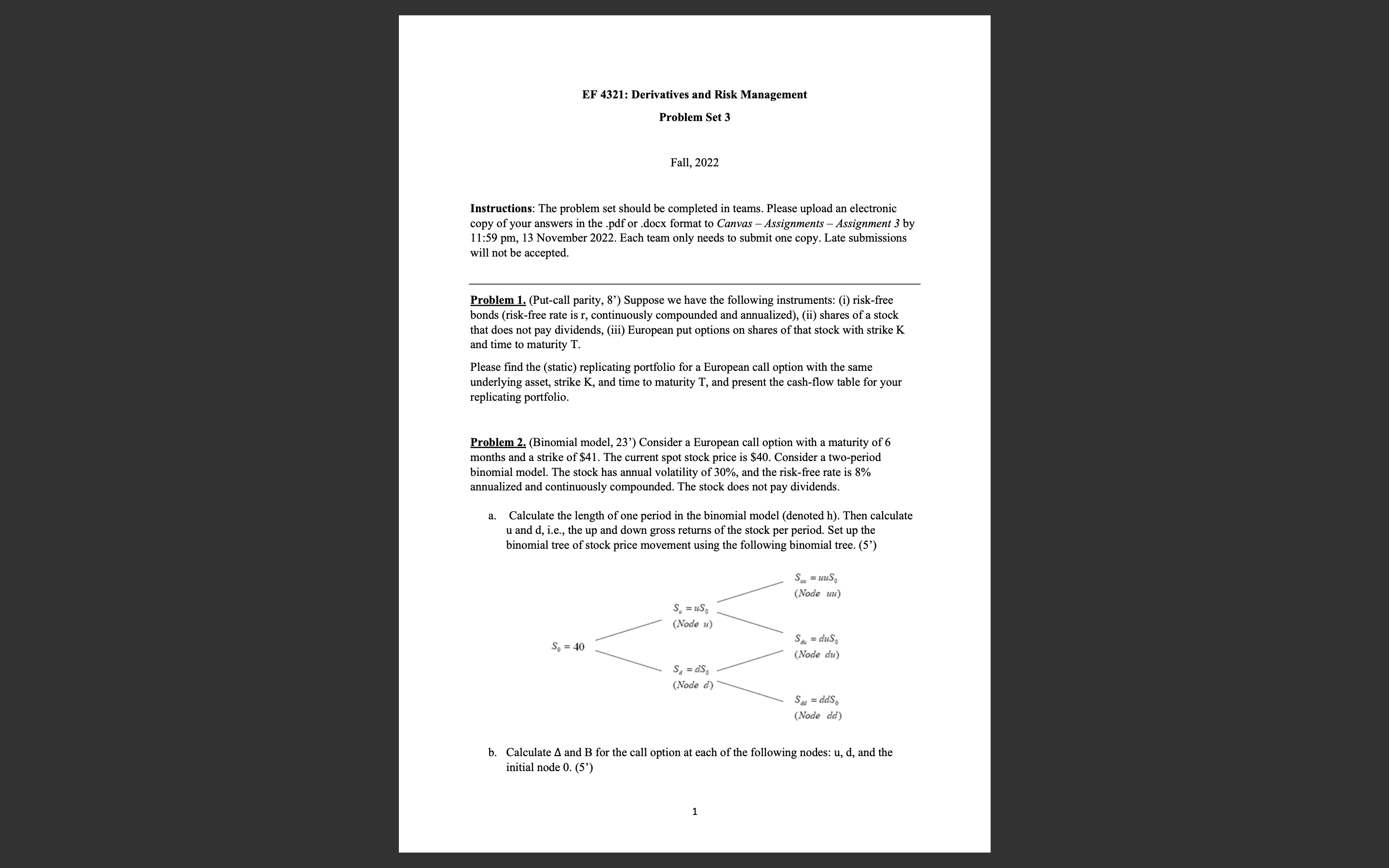

EF 4321: Derivatives and Risk Management Problem Set 3 Fall, 2022 Instructions: The problem set should be completed in teams. Please upload an electronic copy ofyour answers in the .pdf or .docx format to Canvas , Assignments , Assignment 3 by 11:59 pm, 13 November 2022. Each team only needs to submit one copy. Late submissions will not be accepted. Problem 1. (Put-call parity, 8') Suppose we have the following instruments: (i) risk-free bonds (risk-free rate is r, continuously compounded and annualized), (ii) shares of a stock that does not pay dividends, (iii) European put options on shares of that stock with strike K and time to maturity T. Please nd the (static) replicating portfolio for a European Call option with the same underlying asset, strike K, and lime to maturity T, and present the cash-ow able for your replicating portfolio. Problem 2. (Binomial model, 23') Consider a European call option with a maturity 0% months and a strike of $41. The current spot stock price is $40. Consider a two-period binomial model. The stock has annual volatility of 30%, and the risk-free rate is 8% annualized and continuously compounded. The stock does not pay dividends. a. Calculate the length of one period in the binomial model (denoted h). Then calculate u and d, i.e., the up and down gross returns ofthe stock per period. Set up the binomial tree of stock price movement using the following binomial tree. (5') s\" =lmS: (Anna 1111) 5 :ns. (Node u) 31. : r1115; (Node a") s, : 15$: (Node 5') 5,; = all. (Nada (id) b. Calculate A and B for the call option at each of the following nodes: u, d, and the initial node 0. (5') . Calculate the value of the call option at each of the nodes. (Hint: Use the formula: C; = Aisi + 191, where t' denotes node 0, u, or d) (3') . What is a self-nancing strategy? Discuss why your replicating strategy in (b) and (c) is self-fmancing at nodes u and d. (5') r Calculate the risk-neutral probability at each node of u, d, and the initial node 0 Calculate the call option price using the risk-neutral probability method. (5') Problem 3. (Binomial model continued, 15') Consider the same stock as Problem 2. a. In Problem 2, we constructed a recombining binomial tree. For Problem 3, please construct a non-recombining binomial tree. (5') b. An Asian option is an exotic option, and its terminal payoffs are determined by the strike price K and the average stock price throughout the life of the option. Specically, consider the following call option with terminal payoffs max (0,3' 7 K), where is the arithmetic average of the underlying stock prices at time 0, at the end of 3 months, and at the end of 6 months for a price path. Let K = $40. What are the terminal payoffs of that option? Present them in your binomial tree in part (a). (5') Suppose you can only exercise the option at the end of 6 months and cannot exercise early. Price the option with your binomial tree. (5') (Hint: Asian options are pathdependent, so you should use a non-recombining binomial tree to price them. That is because, for path-dependent derivatives, nodes ud and du are different nodes with different paths, although they have the same stock price level)

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock

Students Have Also Explored These Related Finance Questions!