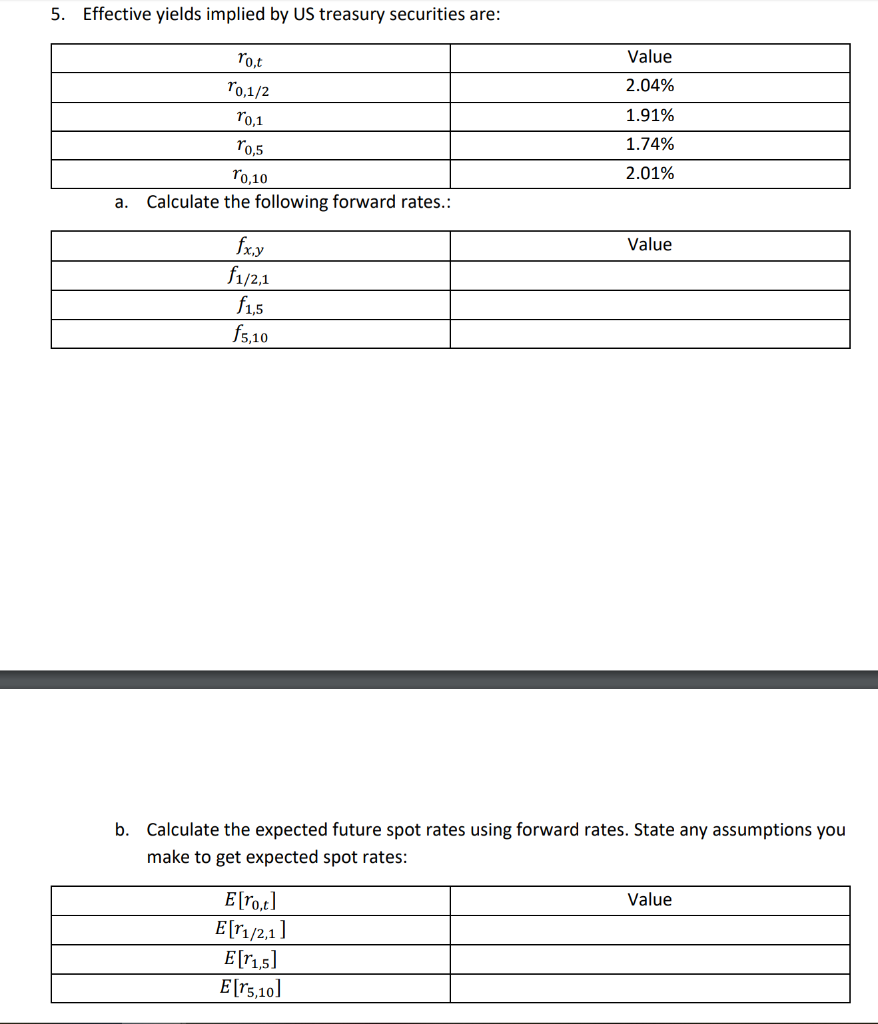

Question: Effective yields implied by US treasury securities are: 5. Value ro,t 2.04% To,1/2 1.91% o,1 1.74% ro,5 2.01% To,10 Calculate the following forward rates.: a.

Effective yields implied by US treasury securities are: 5. Value ro,t 2.04% To,1/2 1.91% o,1 1.74% ro,5 2.01% To,10 Calculate the following forward rates.: a. fx.y f1/21 f1,5 fs,10 Value Calculate the expected future spot rates using forward rates. State any assumptions you make to get expected spot rates: E[rot E[1/2,1] E[r1,5] E[rs,10 Value

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock