Question: E(r) 3) (25%) You have a utility function of U = 0.5Aoand are facing the following investment choices: Investment Expected return, E(r) Standard deviation, o

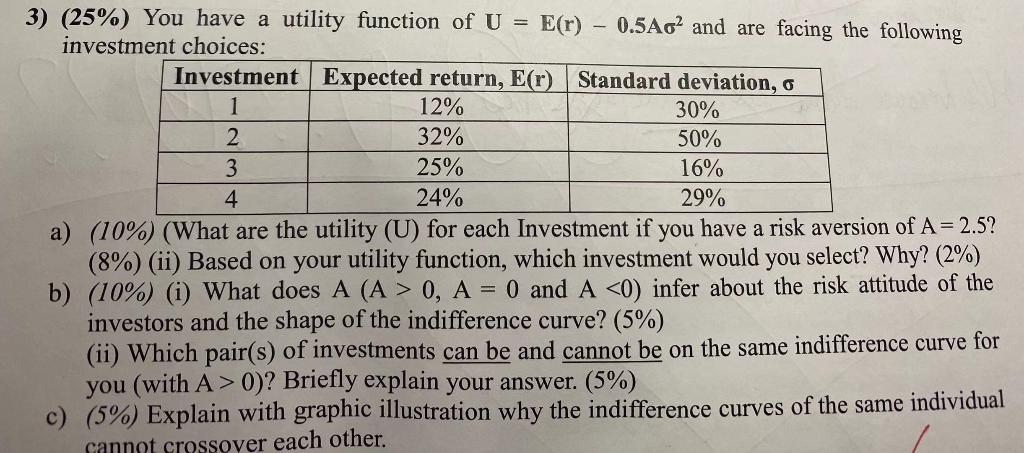

E(r) 3) (25%) You have a utility function of U = 0.5Aoand are facing the following investment choices: Investment Expected return, E(r) Standard deviation, o 1 12% 30% 2 32% 50% 3 25% 16% 4 24% 29% a) (10%) (What are the utility (U) for each Investment if you have a risk aversion of A= 2.5? (8%) (ii) Based on your utility function, which investment would you select? Why? (2%) b) (10%) (i) What does A (A > 0, A = 0 and A 0)? Briefly explain your answer. (5%) c) (5%) Explain with graphic illustration why the indifference curves of the same individual cannot crossover each other

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock