Question: estion 2 ( Mandatory ) ( 7 . 5 points ) Assume zero rates and no dividends. TSLA stock price is traded at $ 4

estion Mandatory points

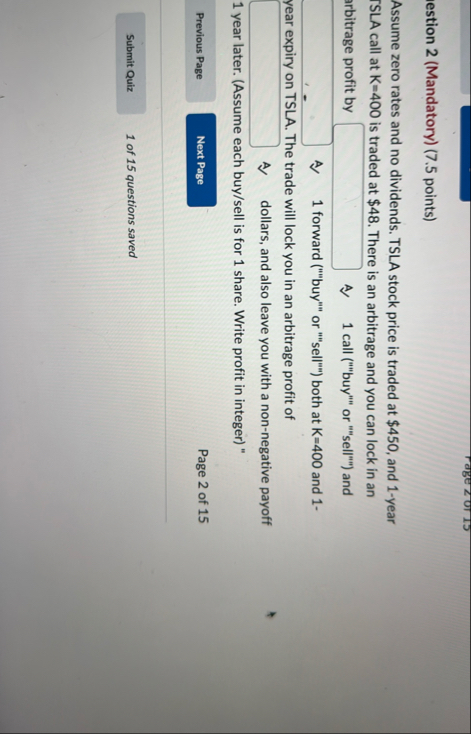

Assume zero rates and no dividends. TSLA stock price is traded at $ and year ISLA call at is traded at $ There is an arbitrage and you can lock in an arbitrage profit by A call buy or sell and A forward buy or sell both at and

year expiry on TSLA. The trade will lock you in an arbitrage profit of A dollars, and also leave you with a nonnegative payoff year later. Assume each buysell is for share. Write profit in integer

Page of

of questions saved

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock