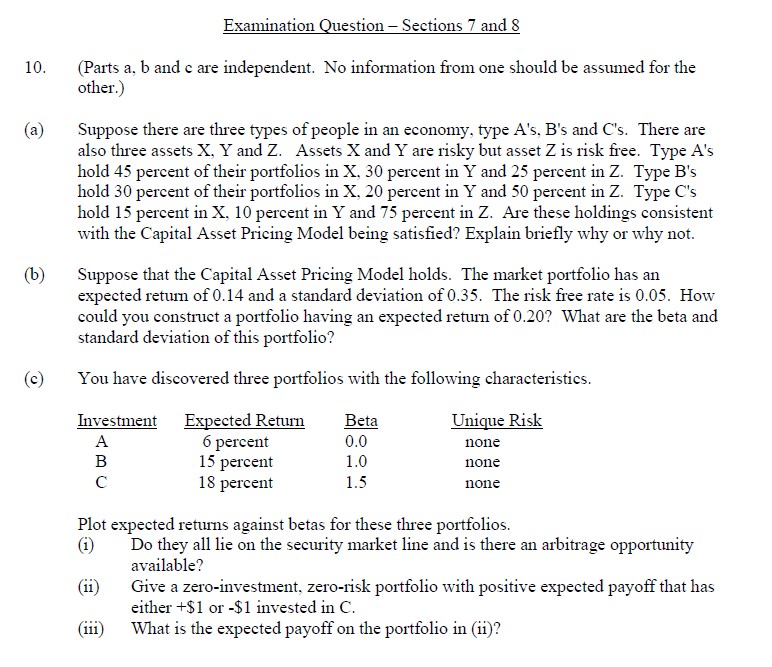

Question: Examination Question - Sections 7 and 8 ( Parts a , b and c are independent. No information from one should be assumed for the

Examination Question Sections and

Parts and are independent. No information from one should be assumed for the

other.

a Suppose there are three types of people in an economy, type As Bs and Cs There are

also three assets and Assets and are risky but asset is risk free. Type As

hold percent of their portfolios in percent in and percent in Type Bs

hold percent of their portfolios in percent in and percent in Type Cs

hold percent in X percent in and percent in Are these holdings consistent

with the Capital Asset Pricing Model being satisfied? Explain briefly why or why not.

b Suppose that the Capital Asset Pricing Model holds. The market portfolio has an

expected return of and a standard deviation of The risk free rate is How

could you construct a portfolio having an expected return of What are the beta and

standard deviation of this portfolio?

c You have discovered three portfolios with the following characteristics.

Plot expected returns against betas for these three portfolios.

i Do they all lie on the security market line and is there an arbitrage opportunity

available?

ii Give a zeroinvestment, zerorisk portfolio with positive expected payoff that has

either $ or $ invested in

iii What is the expected payoff on the portfolio in ii

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock