Question: Example: Consider a mutual fund manager that manages a $5 billion S&P500 index fund. Using daily returns on the S&P500 over 2011 (252 trading days),

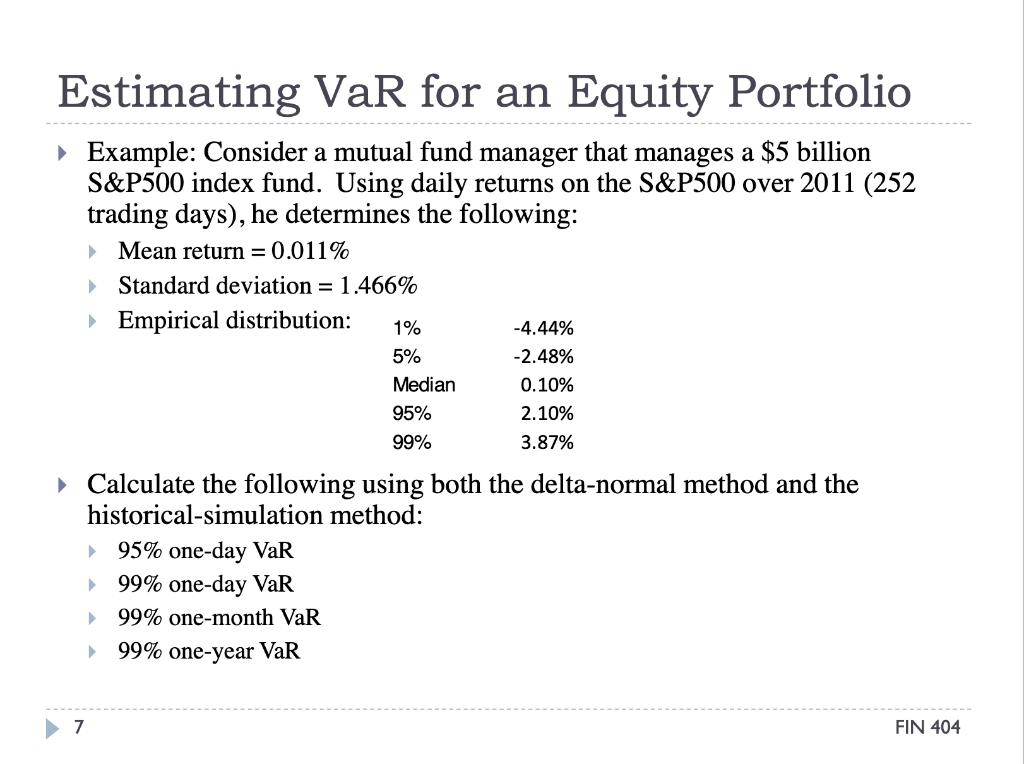

Example: Consider a mutual fund manager that manages a $5 billion S\&P500 index fund. Using daily returns on the S\&P500 over 2011 (252 trading days), he determines the following: b Mean return =0.011% b Standard deviation =1.466% - Empirical distribution: Calculate the following using both the delta-normal method and the historical-simulation method: 95% one-day VaR 99% one-day VaR 99% one-month VaR 99% one-year VaR Example: Consider a mutual fund manager that manages a $5 billion S\&P500 index fund. Using daily returns on the S\&P500 over 2011 (252 trading days), he determines the following: b Mean return =0.011% b Standard deviation =1.466% - Empirical distribution: Calculate the following using both the delta-normal method and the historical-simulation method: 95% one-day VaR 99% one-day VaR 99% one-month VaR 99% one-year VaR

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts