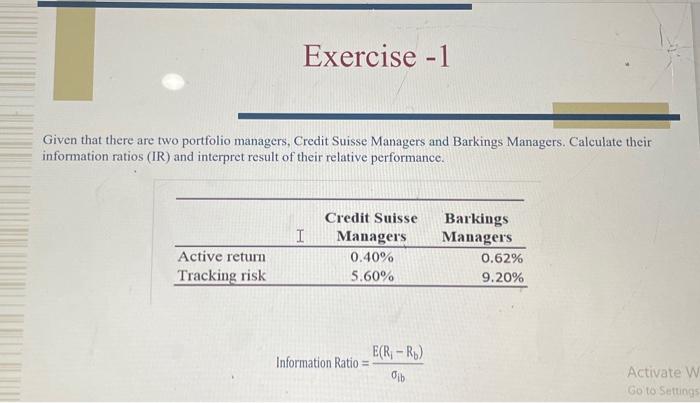

Question: Exercise -1 Given that there are two portfolio managers, Credit Suisse Managers and Barkings Managers. Calculate their information ratios (IR) and interpret result of their

Exercise -1 Given that there are two portfolio managers, Credit Suisse Managers and Barkings Managers. Calculate their information ratios (IR) and interpret result of their relative performance. Credit Suisse Barkings Managers I Managers 0.40% Active return Tracking risk 5.60% Activate W Go to Settings E(R-Rb) dib Information Ratio=- 0.62% 9.20%

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock