Question: Exercise 3. A. In the table are data on two companies. The T-bill rate is 4% and teh market risk premium is 6%. What would

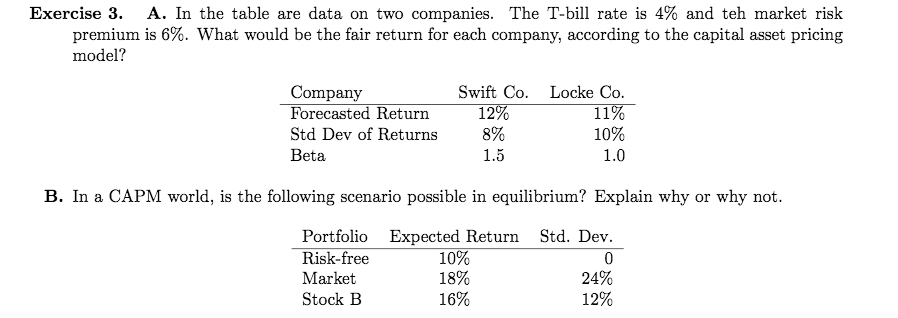

Exercise 3. A. In the table are data on two companies. The T-bill rate is 4% and teh market risk premium is 6%. What would be the fair return for each company, according to the capital asset pricing model? Company Forecasted Return Std Dev of Returns Beta Swift Co. Locke Co. 12% 11% 8% 10% 1.5 1.0 B. In a CAPM world, is the following scenario possible in equilibrium? Explain why or why not. Portfolio Expected Return Std. Dev. Risk-free 10% 0 Market 18% 24% Stock B 16% 12%

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock