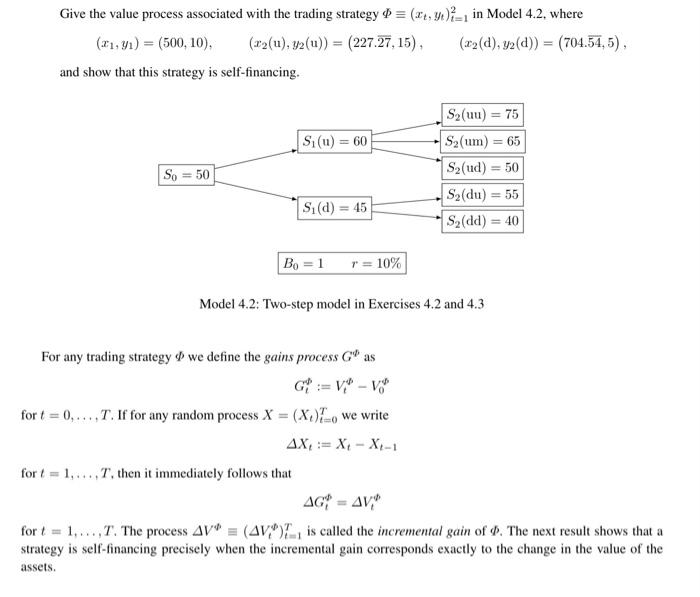

Question: exercise 4.3 Give the value process associated with the trading strategy (xt,yt)t=12 in Model 4.2, where (x1,y1)=(500,10),(x2(u),y2(u))=(227.27,15),(x2(d),y2(d))=(704.54,5), and show that this strategy is self-financing. Model

Give the value process associated with the trading strategy (xt,yt)t=12 in Model 4.2, where (x1,y1)=(500,10),(x2(u),y2(u))=(227.27,15),(x2(d),y2(d))=(704.54,5), and show that this strategy is self-financing. Model 4.2: Two-step model in Exercises 4.2 and 4.3 For any trading strategy we define the gains process G as Gt:=VtV0 for t=0,,T. If for any random process X=(Xt)t=0T we write Xt:=XtXt1 for t=1,,T, then it immediately follows that Gi=Vt for t=1,,T. The process V(Vt)t=1T is called the incremental gain of . The next result shows that a strategy is self-financing precisely when the incremental gain corresponds exactly to the change in the value of the assets. Given the predictable sequence y1=30,y2(u)=40,y2(d)=20 of share holdings and an initial value v=2000, find a predictable sequence (xt)t=12 of bond holdings in Model 4.2 so that the strategy :=(xt,yt)t=12 is self-financing and has initial value v

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts