Question: Exercise 48 The indifference utility function is given U(E(r),0) = E(r) 0.5Ao?, where A is a risk aversion coefficient (i) How do we determine the

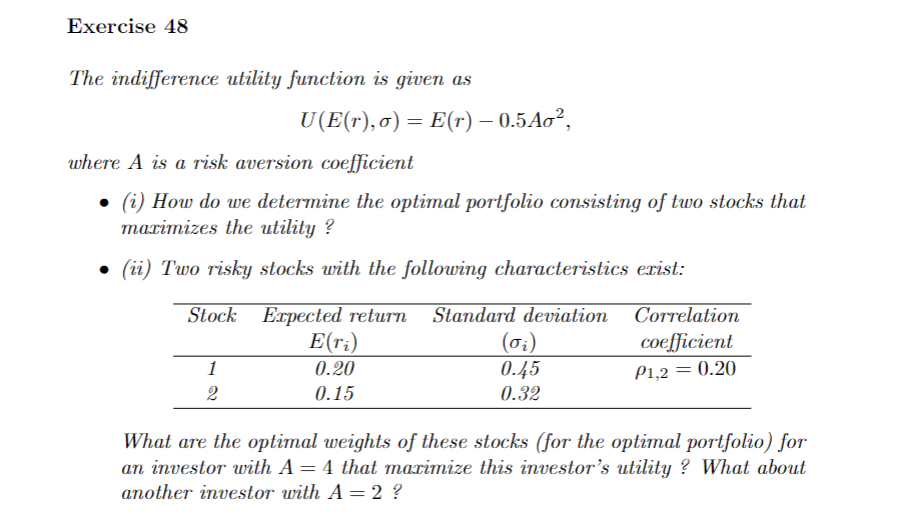

Exercise 48 The indifference utility function is given U(E(r),0) = E(r) 0.5Ao?, where A is a risk aversion coefficient (i) How do we determine the optimal portfolio consisting of two stocks that marimizes the utility ? (ii) Two risky stocks with the following characteristics erist: Stock Expected return Standard deviation Correlation Eri) (Q;) coefficient 1 0.20 0.45 2 0.15 0.32 P1,2 = 0.20 What are the optimal weights of these stocks (for the optimal portfolio) for an investor with A=4 that marimize this investor's utility ? What about another investor with A= 2 ? Exercise 48 The indifference utility function is given U(E(r),0) = E(r) 0.5Ao?, where A is a risk aversion coefficient (i) How do we determine the optimal portfolio consisting of two stocks that marimizes the utility ? (ii) Two risky stocks with the following characteristics erist: Stock Expected return Standard deviation Correlation Eri) (Q;) coefficient 1 0.20 0.45 2 0.15 0.32 P1,2 = 0.20 What are the optimal weights of these stocks (for the optimal portfolio) for an investor with A=4 that marimize this investor's utility ? What about another investor with A= 2

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts