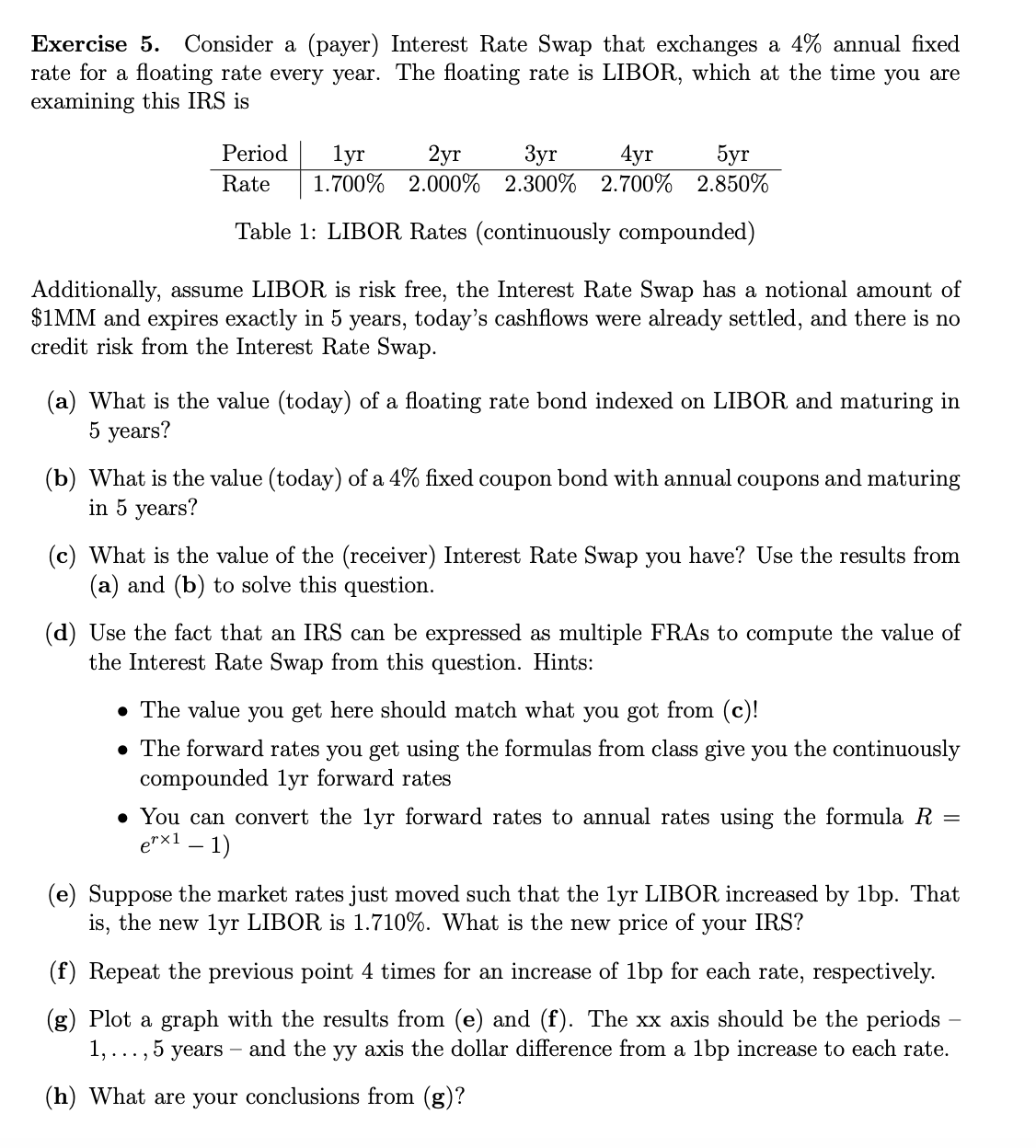

Question: Exercise 5. Consider a (payer) Interest Rate Swap that exchanges a 4% annual fixed rate for a floating rate every year. The floating rate is

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts