Question: Exercise 6: Complete the following example for a bond issued at a price of 106. T-accts below. The same bond from Exercise 4 is

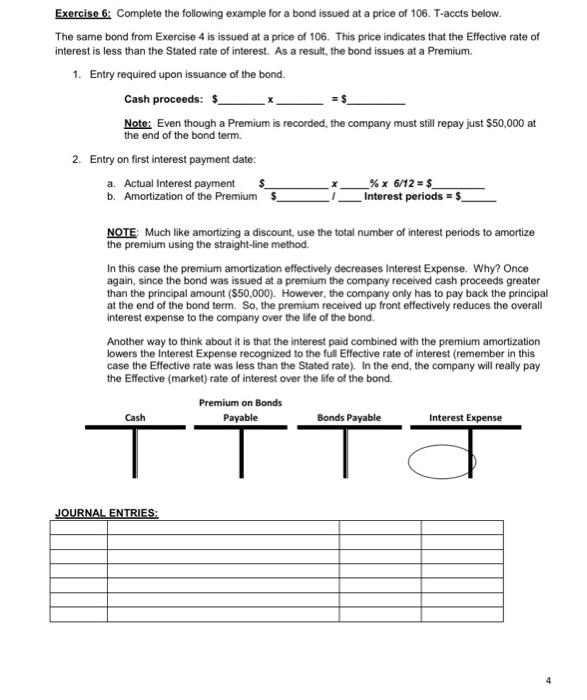

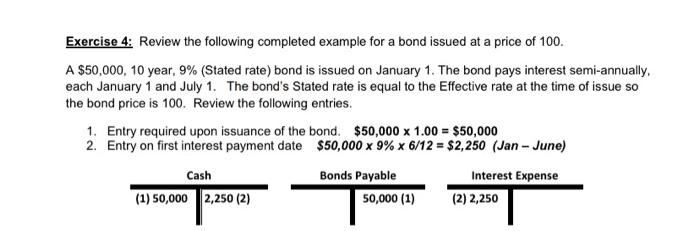

Exercise 6: Complete the following example for a bond issued at a price of 106. T-accts below. The same bond from Exercise 4 is issued at a price of 106. This price indicates that the Effective rate of interest is less than the Stated rate of interest. As a result, the bond issues at a Premium. 1. Entry required upon issuance of the bond. Cash proceeds: $ Note: Even though a Premium is recorded, the company must still repay just $50,000 at the end of the bond term. 2. Entry on first interest payment date: a. Actual Interest payment b. Amortization of the Premium % x 6/12 = $ Interest periods =$_ NOTE: Much like amortizing a discount, use the total number of interest periods to amortize the premium using the straight-line method. In this case the premium amortization effectively decreases Interest Expense. Why? Once again, since the bond was issued at a premium the company received cash proceeds greater than the principal amount ($50,000). However, the company only has to pay back the principal at the end of the bond term. So, the premium received up front effectively reduces the overall interest expense to the company over the life of the bond. Another way to think about it is that the interest paid combined with the premium amortization lowers the Interest Expense recognized to the full Effective rate of interest (remember in this case the Effective rate was less than the Stated rate). In the end, the company will really pay the Effective (market) rate of interest over the life of the bond. Cash Premium on Bonds Payable Bonds Payable Interest Expense TITJ JOURNAL ENTRIES:

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts