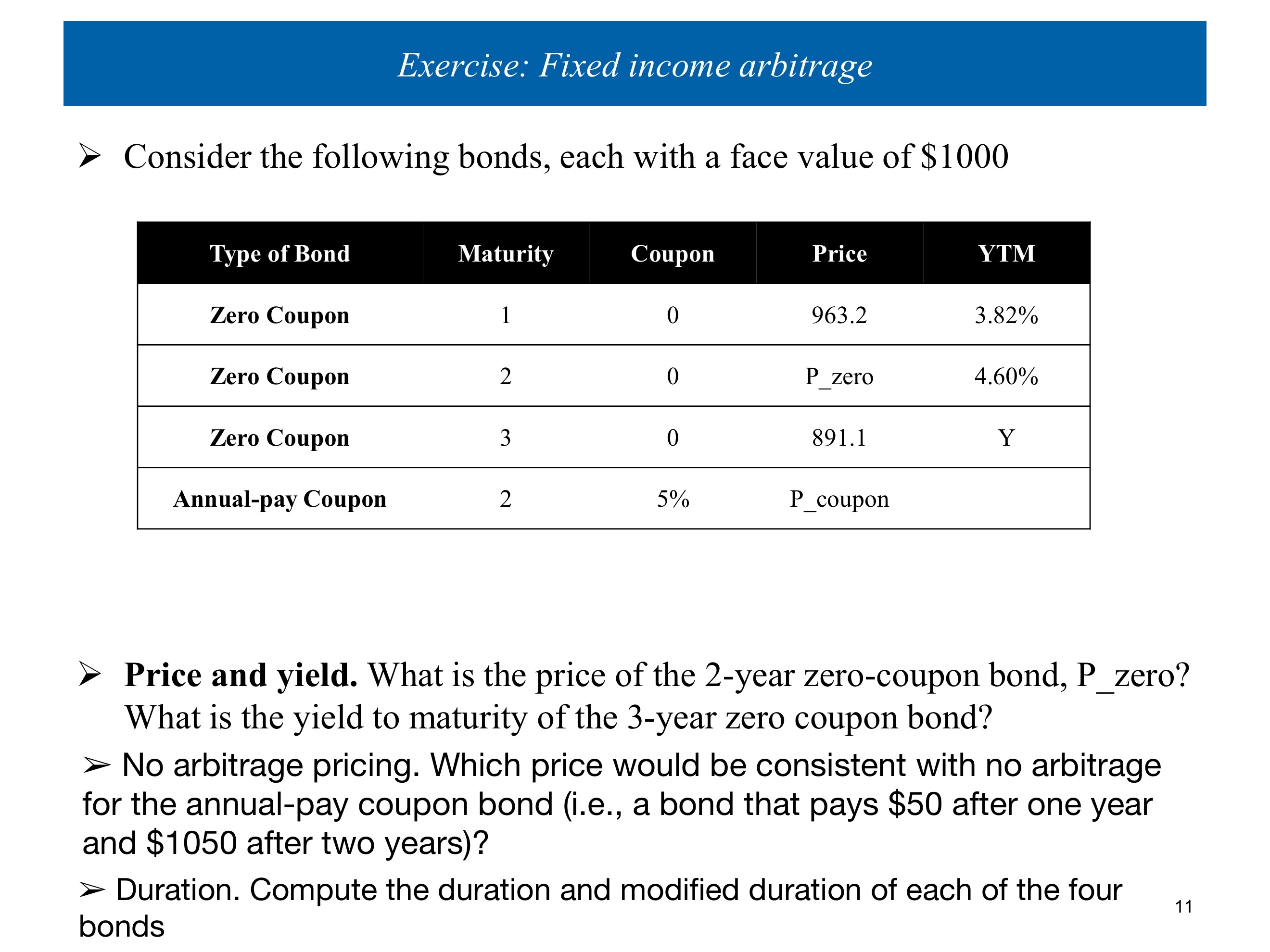

Question: Exercise: Fixed income arbitrage Consider the following bonds, each with a face value of $1000 Type of Bond Maturity Coupon Price YTM Zero Coupon

Exercise: Fixed income arbitrage Consider the following bonds, each with a face value of $1000 Type of Bond Maturity Coupon Price YTM Zero Coupon 1 0 963.2 3.82% Zero Coupon 2 0 P zero 4.60% Zero Coupon 3 0 891.1 Y Annual-pay Coupon 2 5% P_coupon Price and yield. What is the price of the 2-year zero-coupon bond, P_zero? What is the yield to maturity of the 3-year zero coupon bond? No arbitrage pricing. Which price would be consistent with no arbitrage for the annual-pay coupon bond (i.e., a bond that pays $50 after one year and $1050 after two years)? Duration. Compute the duration and modified duration of each of the four bonds 11

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts