Question: EXERCISE IV. A.2. Why do we have the square root of At multiplying the volatility? What will go wrong if we use some other power?

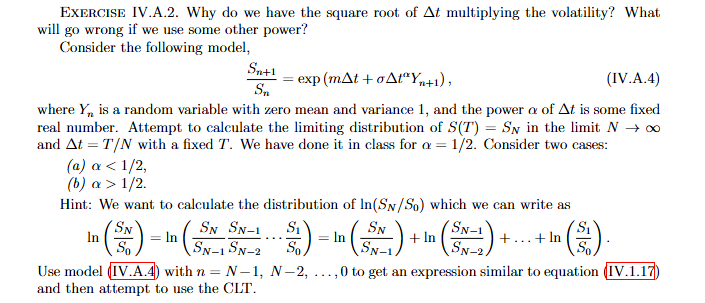

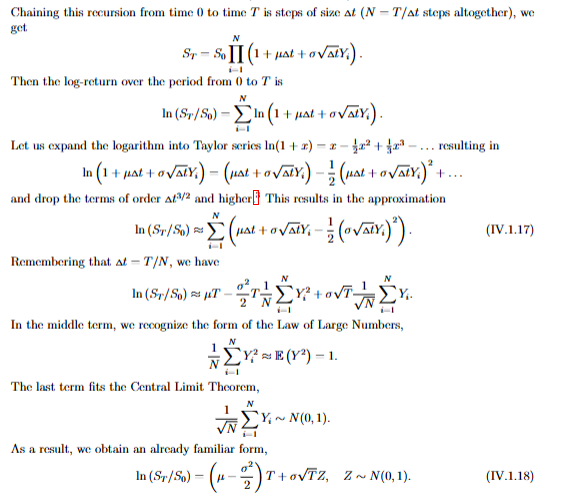

EXERCISE IV. A.2. Why do we have the square root of At multiplying the volatility? What will go wrong if we use some other power? Consider the following model, = exp (mAt+ 0At")+1) , (IV.A.4) Sn where Y,, is a random variable with zero mean and variance 1, and the power a of At is some fixed real number. Attempt to calculate the limiting distribution of S(7) = Sw in the limit N -> co and At =T/N with a fixed 7'. We have done it in class for o = 1/2. Consider two cases: (a) a 1/2. Hint: We want to calculate the distribution of In(Sw/So) which we can write as SN SN SN-1 SN SN-1 In = In = In + In + . .. + In So SN-1SN-2 So SN-1 SN-2. Use model (IV.A.4) with n = N-1, N-2, .. .,0 to get an expression similar to equation (IV.1.17) and then attempt to use the CLT.Chaining this recursion from time 0 to time T is steps of size at (N - T/ at steps altogether), we get N Sr - SoII (1 + pat + OVALY.). Then the log-return over the period from 0 to T is N In (Sr/So) - In (1 + pat + ovaLY.) Let us expand the logarithm into Taylor series In(1 + x) = x - ja' + $23-... resulting in In (1 + pat + ovalY. ) - (ust toVARY.) -" (uAt + OVALY.) +... and drop the terms of order At3/2 and higher This results in the approximation In (Sr/So) = (mat toVAIN -" (ovair.)"). (IV.1.17) Remembering that at - T/N, we have N In (Sr/So) AT 2 In the middle term, we recognize the form of the Law of Large Numbers, 1 N 2 CY? = E(Y?) - 1. The last term fits the Central Limit Theorem, VN SYN(0, 1). As a result, we obtain an already familiar form, In (ST/So) - ( 1 -, ) T + ovTZ, Z ~ N(0, 1 ). (IV.1.18)

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock

Students Have Also Explored These Related Mathematics Questions!