Question: Exhibit 1 is the excel spreadsheet linked belowUsing the information given in Exhibit 1, calculate the historical returns for each company and the share market

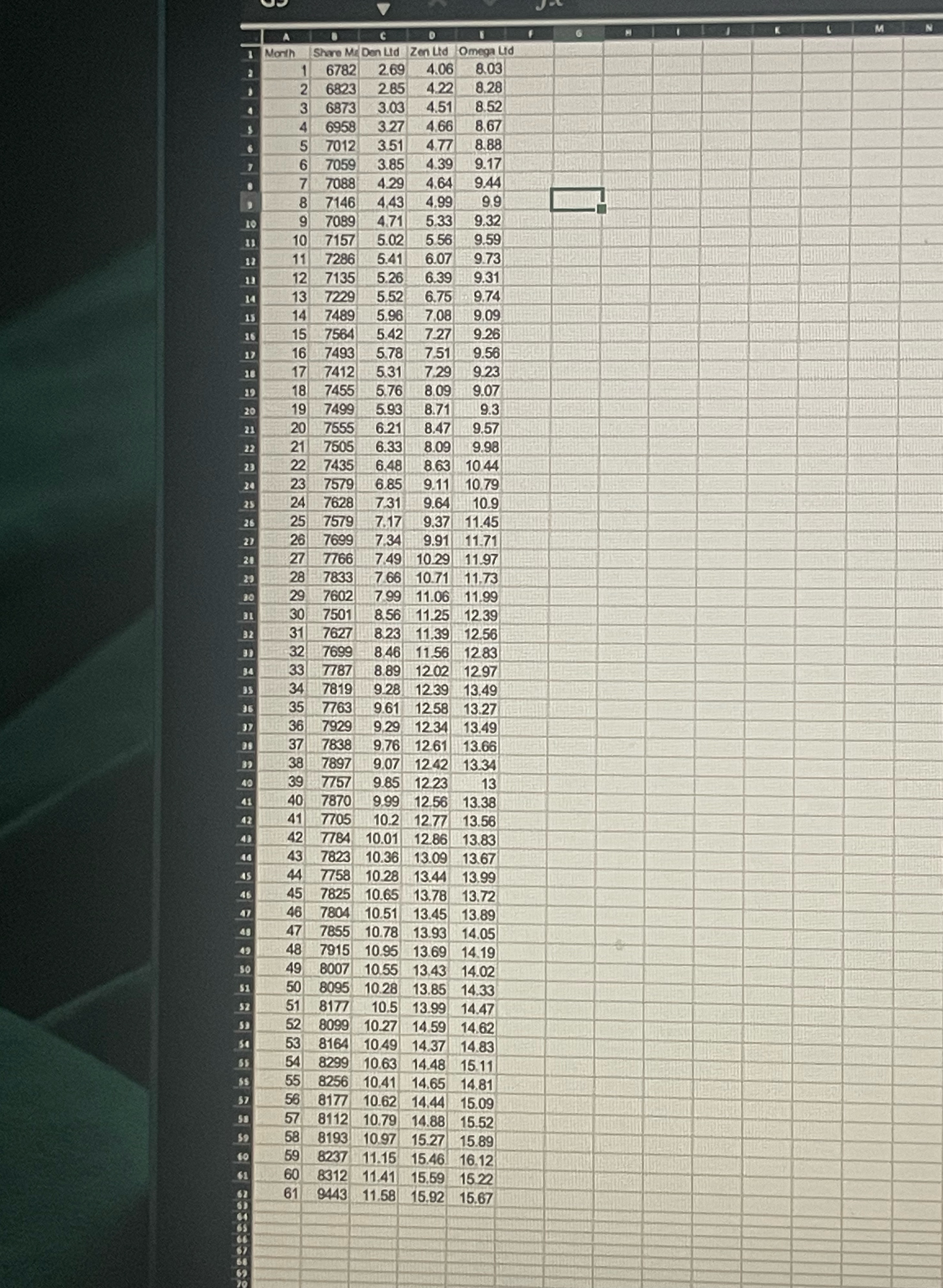

Exhibit 1 is the excel spreadsheet linked belowUsing the information given in Exhibit 1, calculate the historical returns for each company and the share market index. With the use of the excel functions calculate the average monthly return and standard deviation of returns for each company and the market index. Provide a summary of these results in a table format in your report. Are these results consistent with the risk/return relationship as described in finance theory?Using your answers to Question 1, above, and assuming that investors can only invest in one of the three alternative shares in Exhibit 1, use the average return and standard deviation (coefficient of variation) to determine which share would be the most appealing to a risk-averse investor. Provide numerical justification for your selection based on the coefficient of variation. When you answer this question, also address what finance theory assume around investor preferences for risk and return with a focus on risk aversion. What are the annual return prediction intervals for each stock and the market for the next period? What does this measure tells us about the variation of returns for the market and each share? Calculate the correlation coefficient between the 3 stocks. Provide a detailed explanation of your answer and the specific implications for diversification. What combination of 2 shares will produce the highest level of diversification and why?Calculate and the standard deviation of 2-asset portfolios consisting of both Den and Zen; Den and Omega; and Zen and Omega. Assume equal weightings (50%) of each share within the portfolio. Also, calculate the standard deviation a three asset portfolio consisting of all 3 shares (assume equal weightings in the portfolio for each share). Interpret your results and comment and illustrate the impact on risk when combining shares into a portfolio. Use the coefficient of variation to determine which portfolio is the most efficient when it comes to risk and return? What has caused this risk reduction in the portfolio and what specific risk has been eliminated in each case? Determine the systematic risk (Beta) for the three shares. Interpret your answers. The use of excel functions should be used to calculate Beta (slope function in excel). What are the implications around the impact of an asset's price given the beta of each share. Reference some documented limitations of beta when assessing market risk?Calculate the required return and the present value that you would place on each share. Furthermore, assume that Den's dividend has grown from $0.20 to $0.24 in the last 5-years and Zen's dividend has increased from $0.56 to $0.59 over the last 5-years. Omega's dividend has grown from $0.69 to $0.74 in the last 5-years. The last observed 10-year government bond yield was 3.5%. Justify the market risk premium you have used to calculate the required rate of return (Hint: you should be go online and search for market risk premium for the Australian share market). What documented concerns have been raised in regards to dividend valuation models? Please show all your detailed calculations in the report (not excel) when addressing this question.

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts