Question: EXHIBIT 2 5 - 2 The Exemption Equivalent / Applicable Exclusion Amount table [ [ Year of Transfer,Gift Tax,Estate Tax ] , [ 1

EXHIBIT The Exemption Equivalent Applicable Exclusion Amount

tableYear of Transfer,Gift Tax,Estate Tax$$

The estate tax was optional for decedents dying in In lieu of the estate tax, executors could opt to have the adjusted tax basis of the assets in the gross estate carry over to the heirs of the decedent. The applicable credit and exemption are zero for taxpayers who opt out of the estate tax in Harold and Maude were married and lived in a commonlaw state. Maude died in with a taxable estate of $ million and left it all to Harold. Maude's executor filed a timely estate tax return claiming the marital deduction for the property left to Harold including a valid portability election. Harold died this year, leaving the entire $ million to their three children.Refer to Exhibit and Exhibit

Calculate how much estate tax is due from Harold's estate under the following two alternatives.

Assume that neither Harold nor Maude had made any taxable gifts prior to this year.

Assume that Harold and Maude each made a $ million taxable gift in and offset the gift tax at that time with the applicable credit.

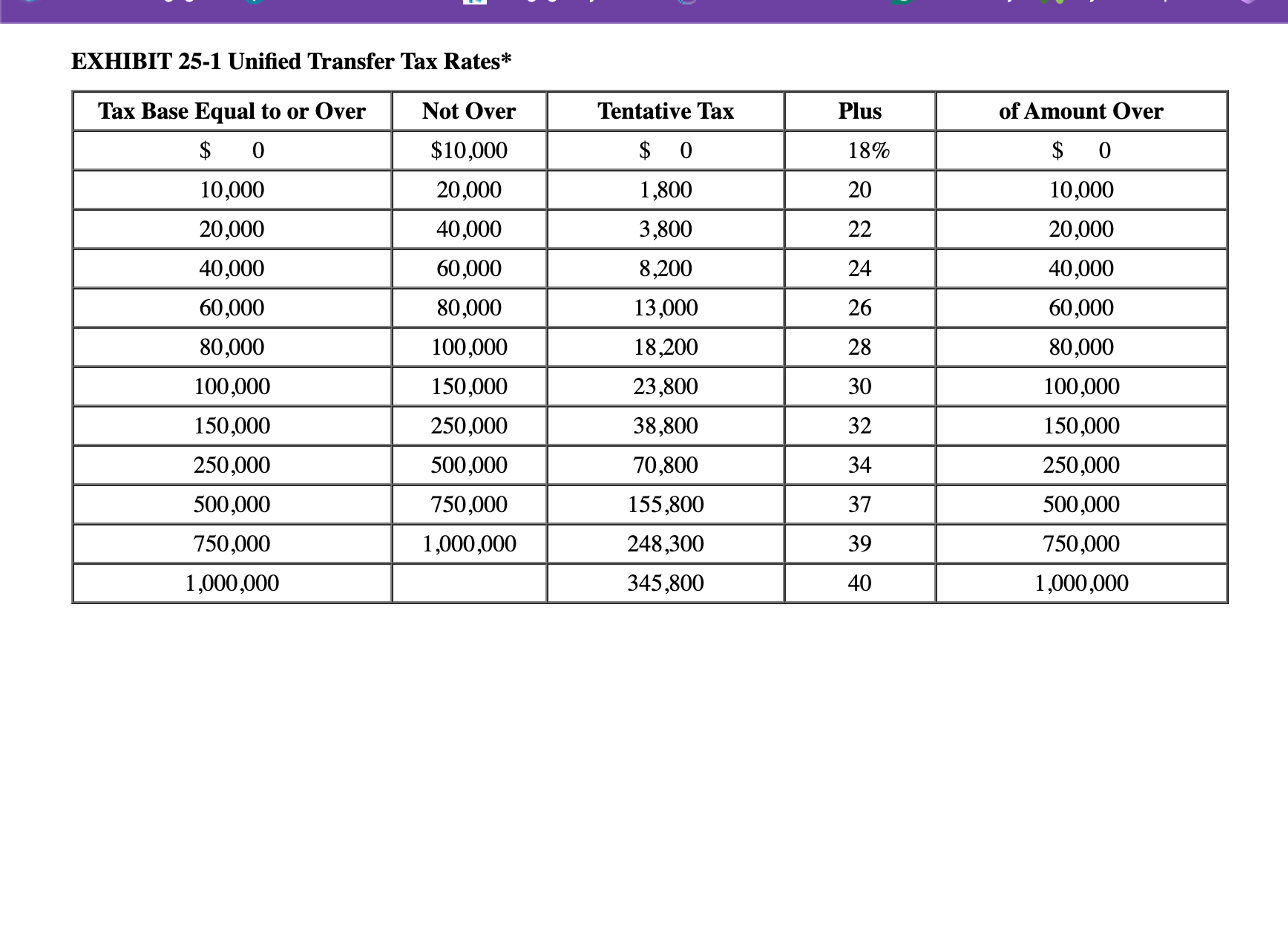

EXHIBIT Unified Transfer Tax Rates

tableTax Base Equal to or Over,Not Over,Tentative Tax,Plus,of Amount Over$$$$

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock