Question: Exhibit 9 Beta= Unlevered Beta*(1+(1-T) * (D/E) within Capital Structure Theory: A Current Perspective 2. Utilizing case data from Figure 9 answer the following questions

Exhibit 9

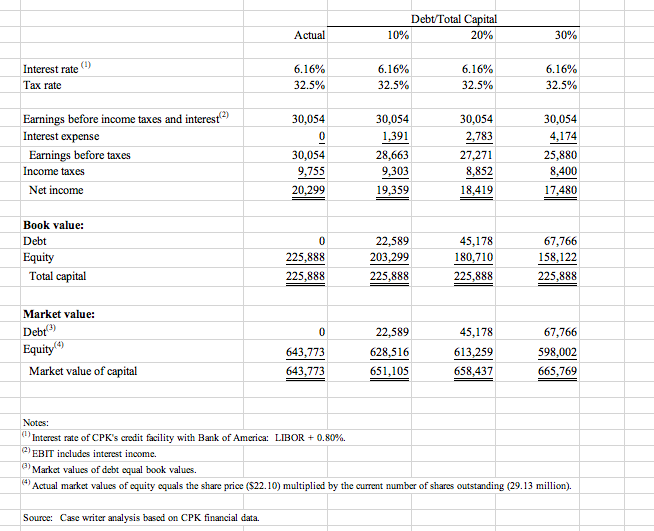

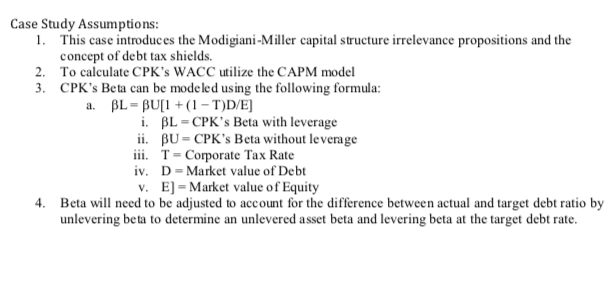

within Capital Structure Theory: A Current Perspective 2. Utilizing case data from Figure 9 answer the following questions a. If CPK's Debt/Total Equity Capital Ratio was 10%; i. What would be CPK's Return on Equity? ii. What would be CPK's WACC? b. If CPK's Debt/Total Equity Capital Ratio was 20%; i. What would be CPK's Retum on Equity? ii. What would be CPK's WACC? If CPK's Debt/Total Equity Capital Ratio was 30%; i. What would be CPK's Retum on Equity? ii. What would be CPK'S WACC? Debt/Total Capital 20% Actual 10% 30% (1) Interest rate Tax rate 6.16% 32.5% 6.16% 32.5% 6.16% 32.5% 6.16% 32.5% Earnings before income taxes and interest(2) Interest expense Earnings before taxes Income taxes Net income 30,054 0 30,054 9,755 20,299 30,054 1,391 28,663 9,303 19,359 30,054 2,783 27,271 8,852 18,419 30,054 4,174 25,880 8,400 17,480 Book value: Debt Equity Total capital 0 225.888 225,888 22,589 203,299 225,888 45,178 180,710 225,888 67,766 158,122 225,888 0 Market value: Debt Equity Market value of capital 643,773 643,773 22,589 628,516 651,105 45,178 613,259 658,437 67,766 598,002 665,769 (2) Notes: Interest rate of CPK's credit facility with Bank of America: LIBOR + 0.80%. EBIT includes interest income. Market values of debt equal book values. Actual market values of equity equals the share price ($22.10) multiplied by the current number of shares outstanding (29.13 million). 3) (4) Source: Case writer analysis based on CPK financial data. Case Study Assumptions: 1. This case introduces the Modigiani-Miller capital structure irrelevance propositions and the concept of debt tax shields. 2. To calculate CPK's WACC utilize the CAPM model 3. CPK's Beta can be modeled using the following formula: a. BL - BU[1 + (1 -T)D/E] i. BL - CPK's Beta with leverage ii. BU = CPK's Beta without leverage iii. T = Corporate Tax Rate iv. D-Market value of Debt v. E] =Market value of Equity 4. Beta will need to be adjusted to account for the difference between actual and target debt ratio by unlevering beta to determine an unlevered asset beta and levering beta at the target debt rate. within Capital Structure Theory: A Current Perspective 2. Utilizing case data from Figure 9 answer the following questions a. If CPK's Debt/Total Equity Capital Ratio was 10%; i. What would be CPK's Return on Equity? ii. What would be CPK's WACC? b. If CPK's Debt/Total Equity Capital Ratio was 20%; i. What would be CPK's Retum on Equity? ii. What would be CPK's WACC? If CPK's Debt/Total Equity Capital Ratio was 30%; i. What would be CPK's Retum on Equity? ii. What would be CPK'S WACC? Debt/Total Capital 20% Actual 10% 30% (1) Interest rate Tax rate 6.16% 32.5% 6.16% 32.5% 6.16% 32.5% 6.16% 32.5% Earnings before income taxes and interest(2) Interest expense Earnings before taxes Income taxes Net income 30,054 0 30,054 9,755 20,299 30,054 1,391 28,663 9,303 19,359 30,054 2,783 27,271 8,852 18,419 30,054 4,174 25,880 8,400 17,480 Book value: Debt Equity Total capital 0 225.888 225,888 22,589 203,299 225,888 45,178 180,710 225,888 67,766 158,122 225,888 0 Market value: Debt Equity Market value of capital 643,773 643,773 22,589 628,516 651,105 45,178 613,259 658,437 67,766 598,002 665,769 (2) Notes: Interest rate of CPK's credit facility with Bank of America: LIBOR + 0.80%. EBIT includes interest income. Market values of debt equal book values. Actual market values of equity equals the share price ($22.10) multiplied by the current number of shares outstanding (29.13 million). 3) (4) Source: Case writer analysis based on CPK financial data. Case Study Assumptions: 1. This case introduces the Modigiani-Miller capital structure irrelevance propositions and the concept of debt tax shields. 2. To calculate CPK's WACC utilize the CAPM model 3. CPK's Beta can be modeled using the following formula: a. BL - BU[1 + (1 -T)D/E] i. BL - CPK's Beta with leverage ii. BU = CPK's Beta without leverage iii. T = Corporate Tax Rate iv. D-Market value of Debt v. E] =Market value of Equity 4. Beta will need to be adjusted to account for the difference between actual and target debt ratio by unlevering beta to determine an unlevered asset beta and levering beta at the target debt rate

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts