Question: Explain step by step please this is mathematical finance class answer all parts please 2. ( 10 points ) ( 459 only ) The value

Explain step by step please this is mathematical finance class answer all parts please

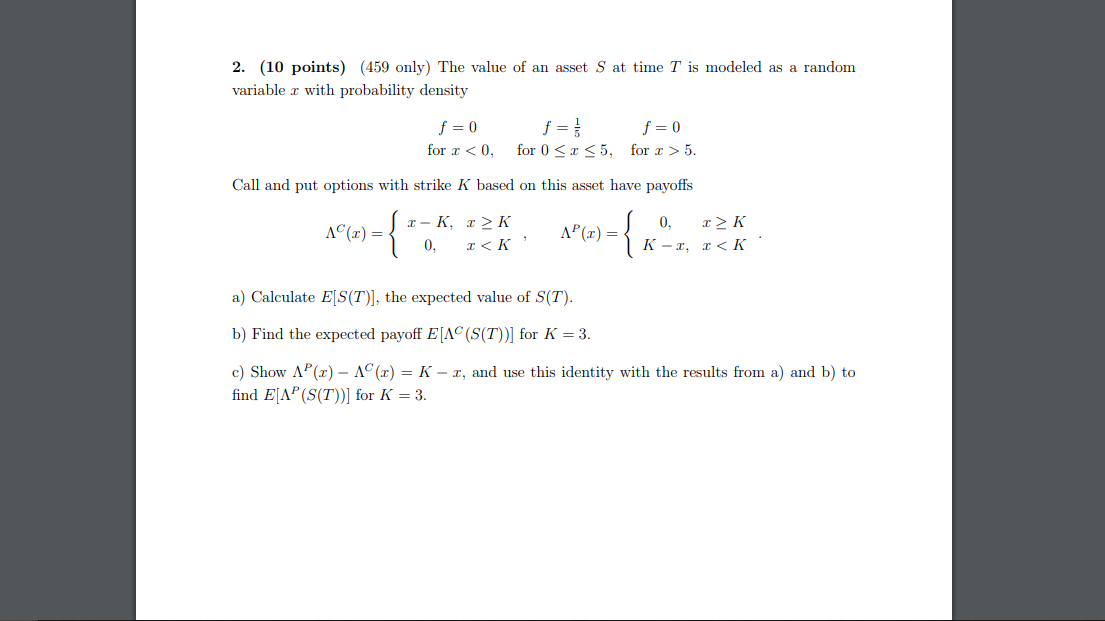

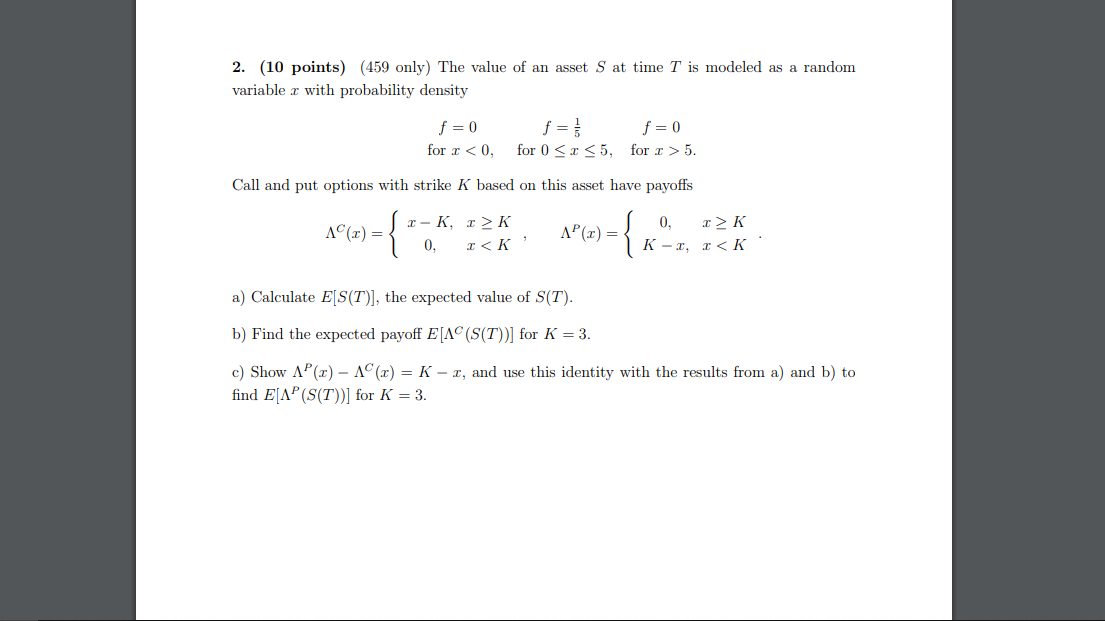

2. ( 10 points ) ( 459 only ) The value of an asset S at time I is modeled as a random variable I with probability density* $ = 0 $ = = f = 0 for * _ O, ford = = = 5, for I _ 5. Call and put options with strike Is based on this asset have payoff's 1 9 ( ` ) = _ ] I - K, I Z K 0 . \I S K " \1 P ( I ) = \ K - * , *

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock