Question: explain to me what this means please Chapter 1. Vlewt About financiot Cout. And Manogement Accounting in A business Organtzotton Another view of these three

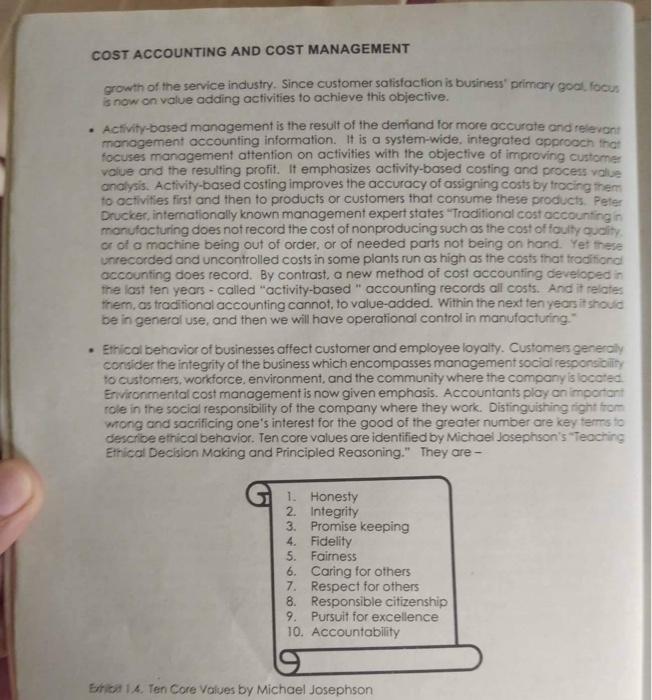

Chapter 1. Vlewt About financiot Cout. And Manogement Accounting in A business Organtzotton Another view of these three atech of occounting thiows that cost occounting encompauses both mandement and financiol occounting as illistrated below: COST ACCOUNTING AND COST MANAGEMENT MANAGEMENT ACCOUNTING FINANCIAL ACCOUNTING Evital 136. Anomer vew on Cort, Manopement, and Fincanciol Accounting Whether the first view of the second view is token. cost accounting hhould not be deemed as pertaining anty to a manufacturing concern. All business enterprises whether service. merchondsing or manufocturing, nowodoys depend on cost accounting for extemaireporting as well as for pianning. controling. and evaluating their operations betore making various important business decisions. Changes in the Business Environment What are the changes faing ploce in the business environment? Recent changes taking place in the business environment have greatly affected the functions and objectives of management accounfing. Some of the more visible changes that have taken place for the recently past decode are as follows: - Advances in technology have helped business in controling of lowering of costs through automatlon. This means that firms gee nolongerlaborintersive but rather machine-intensive. With outomation, costs are reduced and qually is improved which leads to customer safisfoction. Computer-aided manutacturing reters to using of robots, numerically controlled machines and automated assembly systems. These systems reduce the omount and cost of labor, produce large quantify of high quality products and gives management more fime to respond to changes in maket demands. - With the Worid Trade Organization as the driler of global trade, all signatory countries have each a vote in trode disputes, regardless of size. The reduction in trade bamiers gives a consumer the freedom to choose based on the price, quality, access, and design from among domestically or intemationaly produced goods or services. Globalization has created not only marketing opportunities but manufacturing advantages as well. Marnfocturing operations may be situated in ploces where the business has cost and quality odvantages. - Businesses are now emphasizing on performance from the point of view of the customer. which is qualify product or service. Unilke before, where emphasis wos on the number of products manufoctured or ability to meet the budget, with technological advancements. production quality is readily controlled-lead-time is shortened. Deregulation has encouraged more competition. Competition, in tum, has made all businesses more sensitive to customer need and expectations thereby promoting increased performance qualify. Qualify manogement is imperative in all business activities whether the firm is a service. troding or manufacturing entity. Therefore, contemporary management accounting should have as key features quality measurement and reporting. There hos been a continuous 5 COST ACCOUNTING AND COST MANAGEMENT growth of the service industry. Since customer satisfaction is business" primary god. focus is now on value adaing activities to achieve this objective. - Activity-based management is the result of the derfiand for more accurate and relevant management accounting information. It is a system-wide. integrated approcch that focuses management attention on activities with the objective of improving cuttomer volue and the resulting profit. It emphosizes activity-based costing and process value analysis. Activity-based costing improves the accuracy of assigning costs by trocing them to activities first and then to products or customers that consume these products. Peter Drucker, internationally known management expert states "Traditional cost occounting in manufacturing does not record the cost of nonproducing such as the cost of foulty audity. or of a machine being out of order. or of needed parts not being on hand. Yet these Unrecorded and uncontrolled costs in some plants run as high as the costs that tradifiond accounting does record. By contrast, a new method of cost accounting developed in the last ten years - called "activity-based" accounting records all costs. And it reiates thern, as traditional accounting cannot, to value-added. Within the next ten years it shouid be in general use, and then we will have operational control in manufacturing." - Ethical behavior of businesses affect customer and employee loyalty. Customers gereraly consider the integrity of the business which encompasses management sociai responsiciity to Customers, workforce, environment, and the community where the company is loccted. Environmental cost management is now given emphasis. Accountants play an importari role in the social responsibility of the company where they work. Distinguishing light tom wong and sacrificing one's interest for the good of the greater number are key terms to descrioe etrical behavior. Ten core values are identified by Michael Josephson's teaciing Ethical Decision Making and Principled Reasoning." They are - 1. Honesty 2. Integrity 3. Promise keeping 4. Fidelity 5. Fairness 6. Caring for others 7. Respect for others 8. Responsible citizenship 9. Pursuit for excellence 10. Accountability Ethicit 1.4. Ten Core Values by Michael Josephson Chapter 1. Vlewt About financiot Cout. And Manogement Accounting in A business Organtzotton Another view of these three atech of occounting thiows that cost occounting encompauses both mandement and financiol occounting as illistrated below: COST ACCOUNTING AND COST MANAGEMENT MANAGEMENT ACCOUNTING FINANCIAL ACCOUNTING Evital 136. Anomer vew on Cort, Manopement, and Fincanciol Accounting Whether the first view of the second view is token. cost accounting hhould not be deemed as pertaining anty to a manufacturing concern. All business enterprises whether service. merchondsing or manufocturing, nowodoys depend on cost accounting for extemaireporting as well as for pianning. controling. and evaluating their operations betore making various important business decisions. Changes in the Business Environment What are the changes faing ploce in the business environment? Recent changes taking place in the business environment have greatly affected the functions and objectives of management accounfing. Some of the more visible changes that have taken place for the recently past decode are as follows: - Advances in technology have helped business in controling of lowering of costs through automatlon. This means that firms gee nolongerlaborintersive but rather machine-intensive. With outomation, costs are reduced and qually is improved which leads to customer safisfoction. Computer-aided manutacturing reters to using of robots, numerically controlled machines and automated assembly systems. These systems reduce the omount and cost of labor, produce large quantify of high quality products and gives management more fime to respond to changes in maket demands. - With the Worid Trade Organization as the driler of global trade, all signatory countries have each a vote in trode disputes, regardless of size. The reduction in trade bamiers gives a consumer the freedom to choose based on the price, quality, access, and design from among domestically or intemationaly produced goods or services. Globalization has created not only marketing opportunities but manufacturing advantages as well. Marnfocturing operations may be situated in ploces where the business has cost and quality odvantages. - Businesses are now emphasizing on performance from the point of view of the customer. which is qualify product or service. Unilke before, where emphasis wos on the number of products manufoctured or ability to meet the budget, with technological advancements. production quality is readily controlled-lead-time is shortened. Deregulation has encouraged more competition. Competition, in tum, has made all businesses more sensitive to customer need and expectations thereby promoting increased performance qualify. Qualify manogement is imperative in all business activities whether the firm is a service. troding or manufacturing entity. Therefore, contemporary management accounting should have as key features quality measurement and reporting. There hos been a continuous 5 COST ACCOUNTING AND COST MANAGEMENT growth of the service industry. Since customer satisfaction is business" primary god. focus is now on value adaing activities to achieve this objective. - Activity-based management is the result of the derfiand for more accurate and relevant management accounting information. It is a system-wide. integrated approcch that focuses management attention on activities with the objective of improving cuttomer volue and the resulting profit. It emphosizes activity-based costing and process value analysis. Activity-based costing improves the accuracy of assigning costs by trocing them to activities first and then to products or customers that consume these products. Peter Drucker, internationally known management expert states "Traditional cost occounting in manufacturing does not record the cost of nonproducing such as the cost of foulty audity. or of a machine being out of order. or of needed parts not being on hand. Yet these Unrecorded and uncontrolled costs in some plants run as high as the costs that tradifiond accounting does record. By contrast, a new method of cost accounting developed in the last ten years - called "activity-based" accounting records all costs. And it reiates thern, as traditional accounting cannot, to value-added. Within the next ten years it shouid be in general use, and then we will have operational control in manufacturing." - Ethical behavior of businesses affect customer and employee loyalty. Customers gereraly consider the integrity of the business which encompasses management sociai responsiciity to Customers, workforce, environment, and the community where the company is loccted. Environmental cost management is now given emphasis. Accountants play an importari role in the social responsibility of the company where they work. Distinguishing light tom wong and sacrificing one's interest for the good of the greater number are key terms to descrioe etrical behavior. Ten core values are identified by Michael Josephson's teaciing Ethical Decision Making and Principled Reasoning." They are - 1. Honesty 2. Integrity 3. Promise keeping 4. Fidelity 5. Fairness 6. Caring for others 7. Respect for others 8. Responsible citizenship 9. Pursuit for excellence 10. Accountability Ethicit 1.4. Ten Core Values by Michael Josephson

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts