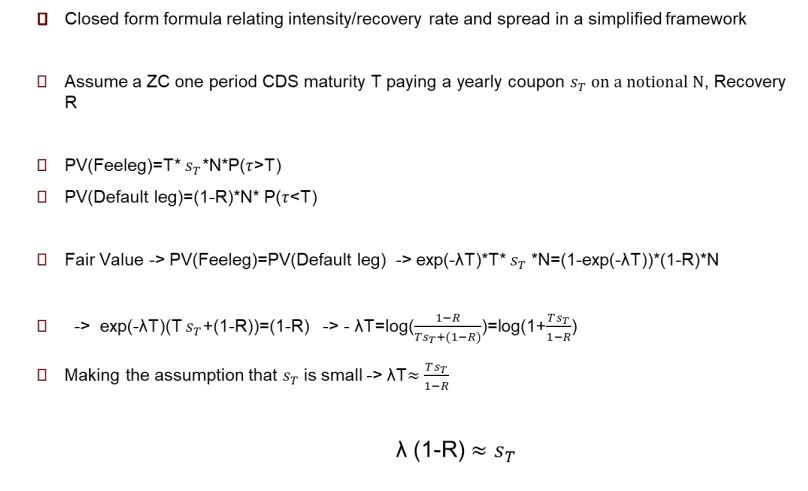

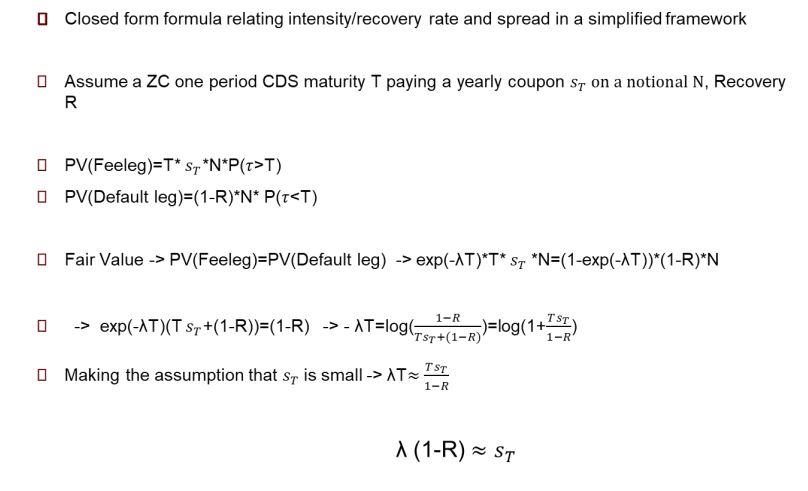

Question: O Closed form formula relating intensity/recovery rate and spread in a simplified framework Assume a ZC one period CDS maturity T paying a yearly

O Closed form formula relating intensity/recovery rate and spread in a simplified framework Assume a ZC one period CDS maturity T paying a yearly coupon ST on a notional N, Recovery PV(Default Fair Value leg) > ST rsr+(1-R) Making the assumption that ST is small -> Tz

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock