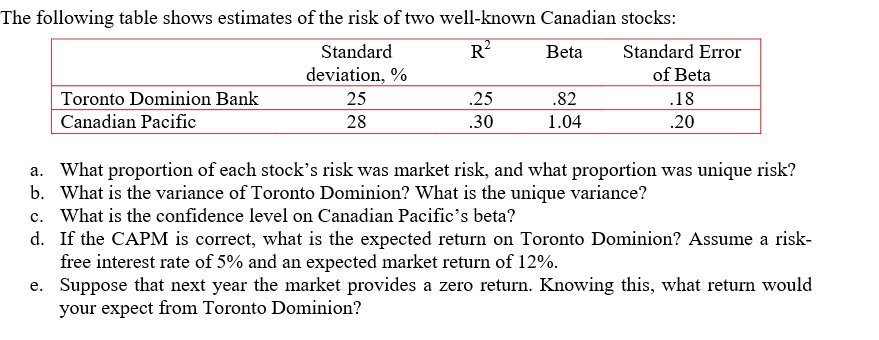

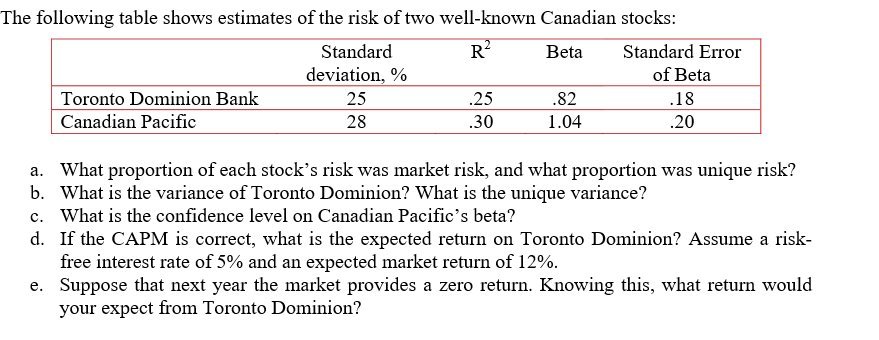

Question: The following table shows estimates of the risk of two well-known Canadian stocks: Toronto Dominion Bank Canadian Pacific Standard deviation, % 25 28 R

The following table shows estimates of the risk of two well-known Canadian stocks: Toronto Dominion Bank Canadian Pacific Standard deviation, % 25 28 R .25 .30 Beta .82 Standard Error of Beta .18 .20 a. b. c. d. e. What proportion of each stock's risk was market risk, and what proportion was unique risk? What is the variance of Toronto Dominion? What is the unique variance? What is the confidence level on Canadian Pacific's beta? If the CAPM is correct, what is the expected return on Toronto Dominion? Assume a risk- free interest rate of 5% and an expected market return of 12% Suppose that next year the market provides a zero return. Knowing this, what return would your expect from Toronto Dominion?

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts